Default loans trapped under toils of law continue swelling, amounting to Tk 1.78 trillion up till last fiscal end, giving economists to feel a lack effective lending and recovery efforts.

Default loans trapped under toils of law continue swelling, amounting to Tk 1.78 trillion up till last fiscal end, giving economists to feel a lack effective lending and recovery efforts.

Latest situation is deemed much worse with the officially counted dud-money amount till June further ballooning by now to push up piles of non-performing loans (NPL) in Bangladesh's banking system.

The volume of bad loans stuck up with legal cobweb swelled up further by over Tk 213.04 billion in June this year after settlement of some cases.

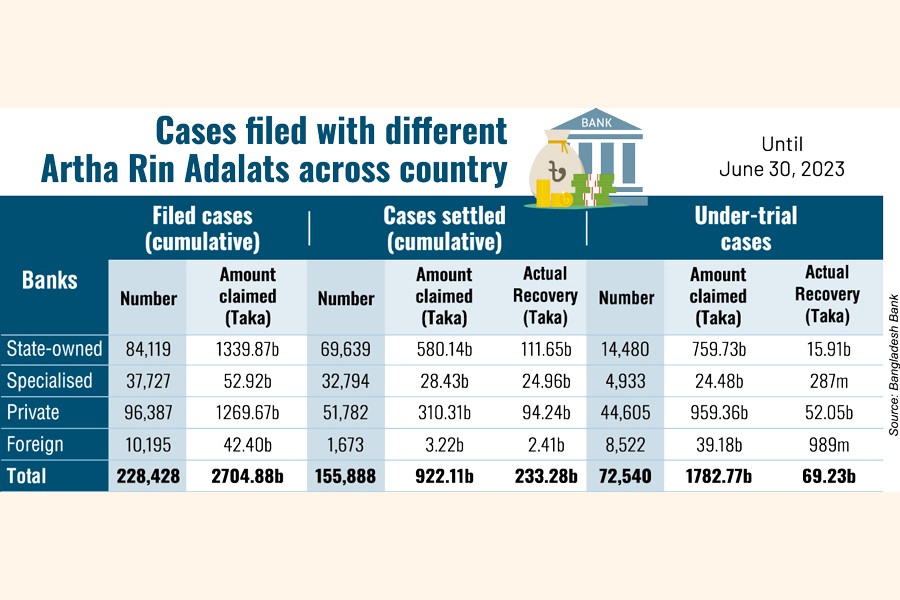

Bangladesh Bank data obtained until June 2023 showed the number of cases pending with the Artha Rin Adalats (money loan courts) as 72,540 by then against huge dues claimed by banks.

Classified or non-performing loans in Bangladesh's banking sector had ballooned over Tk 1.32 trillion until March, according to the BB data.

Economists and analysts say the volume of such money keeps swelling with the passing of time, also for reasons like loan forgeries and lack of due diligence on part of some banks under overall prevailing ambiance.

Mal-governance, poor capacity, insufficient money-loan courts, protracted case proceedings and stay orders are on a long list of drawbacks attributed to this logjam of unsettled cases, according to them.

The loan courts, responsible for handling cases related to defaulted loans, are currently grappling with an overwhelming caseload that has accumulated over time.

The backlog comprises a significant number of loan-default cases, impacting both public and private banks operating within the country.

As of last June, after the formation of the loan court, a total of 228,428 cases were filed with the courts against the cumulative amount of over Tk 2.70 trillion.

However, loan recovery by different courts across the country came to over Tk 69.23 billion only during the period under review, the report states.

People familiar with the process have said the banks often sanction loans "arbitrarily", without keeping in mind that the credits will have to be recovered.

They noted with dissatisfaction that "pressures from bank directors or politicians often force the bankers to lend without merits, and that creates such huge bad loans".

Such loans are approved by the banks against inadequate collateral, according to them.

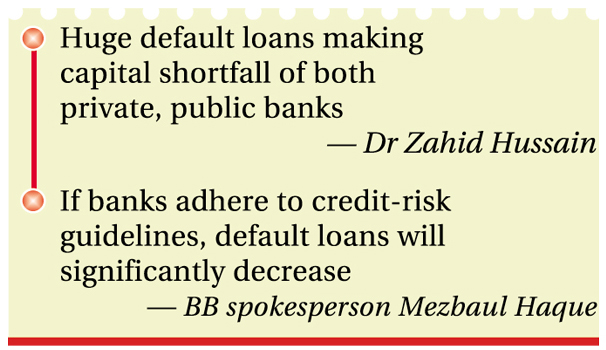

Dr Zahid Hussain, former chief economist at the World Bank's Dhaka office, says such huge default loans are making capital shortfall of both private and public banks, indicating their predicament.

Defaulted loans in the courts are contributing to the rise in non-performing loans due to a contagious effect in the banking sector, which has been triggered by lax regulation, Hussain observes.

"Certain regulations like provision shortfall are encouraging a problematic trend in loan default, which is a cause for concern within the banking sector," says the economist.

"The recent amendment to the Banking Companies Act has not yielded any positive results, as it disregarded the suggestions and opinions of stakeholders aimed at strengthening the banking sector."

Mr Hussain recommends implementing comprehensive legal reforms to bolster the effectiveness of money-loan courts and enhance loan-recovery process.

Md Mezbaul Haque, Executive Director and spokesperson for the Bangladesh Bank, acknowledged that the volume of these default loans is substantial.

However, he also pointed out that the current economic situation and the Ukraine-Russia war have had an impact on the increase in classified loans.

According to Mr Haque, a lawsuit in the loan court typically takes an average of eight to nine years to be resolved. "This prolonged legal process is also contributing to the growing problem of default loans."

The central banker thinks if banks adhere to the credit-risk guidelines, the incidence of default loans would significantly decrease.

Earlier, as of December 31, 2021, the central bank data had shown the number of cases pending with the money loan courts at 68,271 against the dues claimed by banks at Tk 1.43 trillion.

sajibur@gmail.com

© 2026 - All Rights with The Financial Express