Md Rashel Hasan, Md Khorshed Alam and Mst Nurnaher Begum | January 17, 2026 00:00:00

The financial sector has undergone a profound transformation over the past few decades, mainly driven by rapid technological advancements. The most notable developments are the transition from traditional cash-based transactions to cashless or electronic payment systems. A cashless transaction refers to an economic setting where goods and services are exchanged without physical cash, typically through electronic transfers. The global volume of cashless payments has been expanding rapidly, particularly in emerging market and developing economies (EMDEs).

Recognising these global shifts, central banks worldwide have emphasised the importance of establishing robust electronic payment infrastructure. Such systems offer cost-effectiveness and efficiency while reducing the burdens associated with managing physical cash. Printing, securing, and distributing cash is expensive, and economies remain exposed to risks such as theft, fraud, and other cash-related crimes. Beyond cost savings, cashless payments can also stimulate economic growth.

Despite these benefits, cash continues to dominate retail payments—small-value transactions made by households or individuals for daily necessities and services. This heavy reliance on cash poses a significant barrier to an efficient electronic payment system. Facilitating retail payments through electronic channels could substantially reduce reliance on cash, lower central bank expenditures, and enhance the overall financial ecosystem. For example, in FY24, the cost of printing banknotes in Bangladesh alone totalled Tk 3.4 billion (annual average of Tk 3.2 billion over the last 10 years), excluding additional expenses and risks associated with handling cash. Evidence further suggests that initiatives to integrate and harmonies the retail payment markets foster trade, enhance consumption, and contribute positively to the overall economy.

In line with global developments, Bangladesh Bank (BB) and the Government of Bangladesh have introduced several initiatives to promote electronic payments and reduce reliance on cash. Notable examples include the Bangladesh Automated Cheque Processing System (BACPS), Bangladesh Electronic Funds Transfer Network (BFTN), Real-Time Gross Settlement (RTGS), National Payment Switch Bangladesh (NPSB), QR-based payments, the Bangladesh Automated Clearing House (BACH), Internet Banking Fund Transfer (IBFT), Interoperable Digital Transaction Platform (IDTP) and, most recently, the Bangla Quick Response (QR) system (used widely in universities, hospitals, and digital cattle markets). Along with strong policies and support for banks, the initiatives of Mobile Financial Services (MFS), Payment Service Providers (PSPs), and Payment System Operators (PSOs) are designed to accelerate, lower costs, and make the payment ecosystem more user-friendly.

Among the various initiatives to transition from a cash-based economy to a cashless or digital payment ecosystem, QR-based payments stand out as a significant advancement. By offering a convenient, low-cost, and secure mode of transaction for both consumers and merchants, QR-based payment systems have shown strong potential to enhance financial inclusion and accelerate the adoption of digital financial services. Countries such as Brazil, China, India, Paraguay, Malaysia, and Singapore have achieved remarkable success in reducing their dependence on cash and advancing toward digital economies primarily through the widespread adoption of QR-based payment systems.

In response to this global trend, MFS providers in Bangladesh introduced their own proprietary QR-based payment systems in 2018. However, these early models were merchant-specific, meaning each QR code could only be used for payments within the issuing provider’s network. To address this limitation, BB launched Bangla QR as an interoperable payment platform in 2021, introducing an interoperable QR code payment standard that enables seamless transactions across different banks, MFS providers, and PSPs. This initiative has significantly expanded the acceptance and accessibility of digital payments among both merchants and consumers.

Measuring Cash Use in Payments: Use of Cash as a Payment Option. In recent years, the proliferation of payment options—such as mobile payments, payment cards, and E-Money—has given consumers greater flexibility in choosing whether to use cash or alternative payment methods. However, studies show that cash remains the dominant payment method for small-value transactions, despite the increasing availability of digital alternatives . Although the COVID-19 pandemic accelerated the adoption of card and mobile payments in many countries, several studies find that cash remained widely used in populous and developing economies due to factors such as large informal sectors, limited digital access, and trust issues with electronic systems.

Both demand-side and supply-side factors are associated with the continued use of cash as a medium of payment. On the supply side, many merchants are reluctant to accept digital payments due to interchange fees and the associated costs of maintaining electronic payment infrastructure. From the demand-side perspective, consumer preferences also play a critical role. Despite these factors, most economies have observed a gradual decline in overall cash use in recent years.

Measuring Cash Use Global Context. Measuring the extent to which cash is used for retail payment purposes, however, is not straightforward. Several proxies have been developed to approximate cash usage in the economy. A simple metric, such as the currency in circulation (CIC) to GDP ratio, provides only a partial picture. While a rising CIC-to-GDP ratio reflects broader monetary activity, most of these payments involve instruments that do not directly compete with cash, thereby failing to accurately capture cash’s role as a means of payment.

A more precise approach is the market share method, which measures cash relative to its substitutes. Khiaonarong & Humphrey (2022) suggest using the following indicator:

![]()

Where CASH denotes the total value of ATM cash withdrawals, and CARDS represents debit and credit card payments. E-money is defined as a stored-value arrangement in which funds are stored on a card or mobile phone (akin to an electronic wallet). This ratio indicates the extent to which cash remains a primary payment instrument in an economy.

Measuring Cash Use in Bangladesh. To estimate the extent of cash reliance in Bangladesh’s retail payment system, we use an equation conceptually similar to that proposed by Khiaonarong and Humphrey (2022), but adapted to reflect Bangladesh’s financial market structure and data availability. The indicator for the Share of Cash Use in Retail Payments is defined as follows:

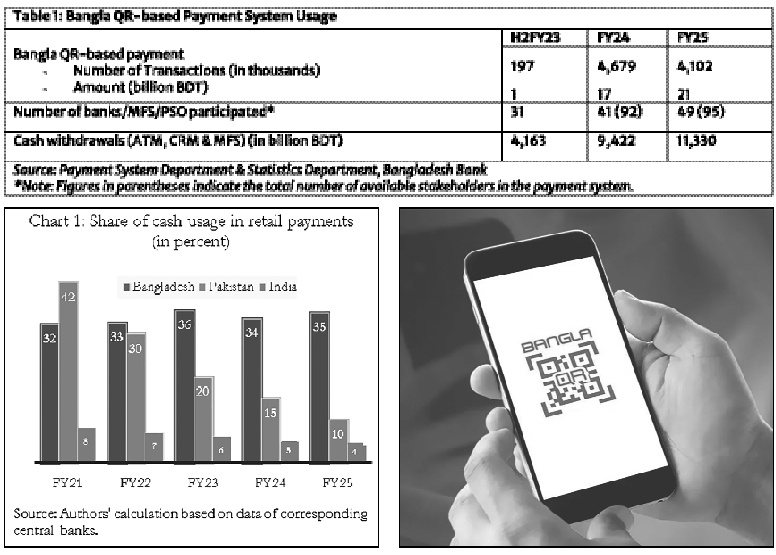

Where Cash-based payments indicate ATM Withdrawals (including CRM) and Cash-out Using MFS. Cashless payments represent E-commerce Payments (Cards), POS Payments, Merchant Payments through MFS, Other Payments through MFS, and Electronic Fund Transfer (EFT). Using the above equation, we estimated the share of cash use relative to its alternative payment substitutes within Bangladesh’s formal payment infrastructure. In FY20, during the COVID-19 pandemic, the share of cash usage stood at 37 per cent. It declined to 32 per cent in FY21 and remained around 33 per cent in FY22, reflecting a behavioural shift toward contactless payments as people sought to avoid physical cash handling to reduce the risk of infection. However, the share rose again to 36 percent in FY23 and has stabilized at approximately 35 per cent in FY25 (Chart 1).

When compared with neighbouring countries such as India and Pakistan, Bangladesh’s reliance on cash remains significantly higher. In 2016, India demonetised approximately 86 per cent of its circulating currency and simultaneously launched major cashless initiatives while investing heavily in digital payment infrastructure. These combined efforts led to remarkable progress in digital payment adoption, which further accelerated during and after the COVID-19 pandemic. The share of cash in total retail payments in India dropped from 8 per cent in 2021 to just 4 per cent in 2025. Similarly, Pakistan has demonstrated substantial improvement in reducing cash dependence, with the cash share in retail payments declining from 42 per cent in 2021 to 10 per cent in 2025. These trends suggest that while Bangladesh has made progress toward digitalisation, its transition to a cashless economy is slower than that of its regional peers.

Retail Payment Methods in Bangladesh: In Bangladesh, individuals have access to several options for making retail payments. Among these, cash remains a prominent means of payment, with its availability stemming from multiple sources. Typically, individuals obtain cash through (Automated Teller Machine) ATM or Cash Recycling Machine (CRM) withdrawals, cash-out transactions using MFS, or directly from the counters of banks and agent banking outlets. At the same time, cashless payment platforms are expanding rapidly, reflecting Bangladesh’s evolving financial landscape, where traditional cash-based transactions coexist with modern digital payment systems.

ATM Withdrawals (including CRM). In Bangladesh, ATM withdrawals remain the dominant method for obtaining cash for retail transactions, thereby reinforcing a nationwide cash-based payment culture.

Cash-out Using MFS. In rural regions of Bangladesh, this is the primary way to access cash for retail payments. Consequently, cash-out through MFS continues to promote a cash-dependent payment environment, especially in rural areas.

E-commerce Payments (Cards). Card-based payments for e-commerce transactions are increasingly promoting cashless retail transactions in Bangladesh. Moreover, e-commerce payments can also be made through internet banking platforms, where available, and via MFS, offering consumers multiple convenient and secure digital payment options.

POS Payments. This system serves as an essential cashless transaction platform across retail outlets, restaurants, and service centers.

Electronic Fund Transfer (EFT). It is one of the key cashless retail payment methods, regulated and operated by the BB, which supports the country’s move toward a more efficient and transparent cashless retail payment ecosystem.

Merchant Payments through MFS. Merchant payments through MFS refer to digital payments made by customers to merchants for purchasing goods and services using mobile financial services accounts, such as bKash, Nagad, or Rocket, rather than cash. It has become one of the fastest-growing forms of cashless retail transactions in Bangladesh. In addition to MFS platforms, many merchants offer multiple payment options, including bank cards and QR-based payments. While QR-based payments are primarily facilitated through MFS providers, an increasing number of banks are also adopting QR payment systems at merchant outlets, expanding the country’s digital payment ecosystem.

Other Payments through MFS. Other payments through MFS include person-to-person transfers, government-to-person payments, employee salary disbursements, payments for mobile talk time and internet purchases, and utility bill payments. These are also considered cashless payment methods in Bangladesh.

There are several other payment methods, including over-the-counter withdrawals, manual or BACH cheque payments, intra- and inter-bank fund transfers, IBFT, and RTGS. However, time series data for most of these modes are not available.

QR code and QR code-based payment: A QR code, or Quick Response code, is a two-dimensional barcode that can store a wide range of information, including website links, product details, and payment instructions. It consists of black squares arranged on a white background, which a smartphone camera or a QR code reader can easily scan. Unlike traditional barcodes, which hold limited information and can only be read in a fixed orientation, QR codes can store much more data and can be read in any orientation. They can be scanned from any angle, making them faster and more versatile. Initially developed for the automotive industry, QR codes gradually found applications across sectors and eventually became a popular contactless payment method worldwide. Their adoption has been particularly transformative in the retail and service industries, where they provide a low-cost alternative to traditional point-of-sale (POS) devices. Instead of relying on expensive infrastructure, merchants of all sizes—including small and micro businesses—can now be integrated into the digital payment ecosystem using QR technology.

In practice, QR code-based payment systems work by enabling customers to transfer money digitally through a simple scan. A merchant displays a QR code, either printed or on a digital screen, and the customer scans it using a mobile payment application. The code contains the merchant’s account details. The customer may either manually input the transaction amount or have it automatically filled in. After confirmation, the payment is instantly transferred from the customer’s account to the merchant’s account.

The growing popularity of QR code-based payments lies in their simplicity, convenience, and security. Customers no longer need to carry cash or cards, while merchants avoid the expense of purchasing POS terminals. This cost has traditionally hindered the adoption of digital payments in many developing economies. As a result, QR codes have played a vital role in broadening financial inclusion by empowering even small vendors and individual service providers to accept digital payments with minimal investment. In both developed and emerging markets, this technology is contributing to more accessible, efficient, and inclusive financial ecosystems, reshaping the way everyday transactions are conducted.

Developments in QR-based Payments in Bangladesh. The introduction of QR-based payments has been one of the most significant developments in Bangladesh’s efforts to promote a digital financial system. Initially, leading Mobile Financial Service (MFS) providers such as bKash, Nagad, and Rocket introduced their own proprietary QR payment systems in 2018. These early models allowed users to scan merchant-specific QR codes within their respective apps to make payments. However, the lack of interoperability—where a customer from one platform could not pay a merchant using another—limited the scalability and overall impact of these systems.

Recognising this fragmentation, BB launched the Bangla QR initiative in January 2021 to standardise and unify QR code–based transactions across banks, Mobile Financial Service (MFS) providers, and Payment Service Providers (PSPs) (Bangladesh Bank, 2021). Bangla QR introduced a single interoperable format that allows all licensed institutions to issue and accept QR-based payments, enabling seamless transactions across platforms.

This development marked a significant advancement in payment interoperability, enabling small and medium-sized enterprises (SMEs) and micro-merchants to accept digital payments without costly point-of-sale (POS) terminals. The system operates under the National Payment Switch Bangladesh (NPSB) framework. As of FY25, the initiative encompasses 42 banks, 7 MFS providers, 3 payment service providers (PSPs)—reflecting the broad institutional participation that underpins Bangladesh’s growing interoperable payment ecosystem.

Performance of Bangla QR-based Payment System. After the Bangla QR-based payment system was launched in 2021, participants started using this platform in the latter half of FY23. However, the system became more active during FY24, as shown in Table 1. The number of transactions rose sharply to 4,679 thousand in FY24, up from 197 thousand in FY23. Despite this, the growth momentum was not as strong in FY25. The total number of transactions declined by 12.3 percent, although the overall transaction value increased slightly to BDT 21 billion from BDT 17 billion in FY24.

Another notable observation concerns the number of participants in the Bangla QR ecosystem. According to Table 1, the expansion of stakeholders to operationalise Bangla QR has been relatively slow—only 49 payment system stakeholders participated by the end of FY25, compared to 41 a year earlier, despite nearly double that number being eligible to join. This suggests that many stakeholders are not yet technically ready or are facing operational or strategic barriers to participation, which warrants further investigation and policy attention.

As discussed earlier, ATM/CRM withdrawals and MFS cash-outs are primarily used to purchase daily necessities, suggesting they could serve as a substitute for retail payments. Although transaction value from these channels has declined in recent years, the total amount—BDT 11,330 billion—remains substantial and reflects continued reliance on cash withdrawals.

Most ATM withdrawals are mainly used for cash-based retail transactions, indicating that these users represent a significant potential customer base for QR-based payments. Overall, Bangla QR-based retail payments show strong growth potential toward a cashless economy.

From a regulatory perspective, BB has taken several initiatives to expand the usage of Bangla QR-based payments. All relevant institutions were instructed to make their mobile applications compatible with the Bangla QR system and to replace proprietary QR codes with the standardized Bangla QR code. Additionally, BB directed stakeholders to undertake awareness campaigns among both customers and merchants to promote adoption.

Despite these regulatory efforts, the participation rate remains modest—only about half of the 95 available payment stakeholders are currently active—indicating a slow rate of adoption. Similarly, the relatively low transaction numbers and values suggest that consumers are not yet fully aware of the convenience and benefits associated with QR-based payments.

Another factor that may contribute to this slow adoption is the Merchant Discount Rate (MDR). Initially, BB set the upper cap for the MDR at 0.70 per cent for individual merchant payments and 1.60 per cent for other payment types. In January 2024, the MDR cap for micro-merchants was revised to 0.50 per cent for payments via bank accounts, debit cards, and prepaid cards, and 0.80 percent for payments through credit cards, Mobile Financial Services (MFS), and Payment Service Providers (PSPs). For regular merchants, the MDR was set at 1.0 per cent (for bank accounts, debit cards, and prepaid cards) and 1.20 per cent (for credit cards, MFS, and PSPs), along with an additional 0.15 percent NPSB charge. Recently, in February 2025, BB revised the MDR structure to a flat 1.15 percent for all merchants and withdrew the NPSB platform fee.

While this uniform MDR aims to simplify the fee structure, it may still discourage micro and small merchants—who typically operate with thin profit margins—from adopting the Bangla QR system. Further consideration of tiered or subsidized MDR rates could encourage broader participation and accelerate the shift toward digital retail payments.

In addition to introducing the interoperable QR-based payment solution under the NPSB network, BB has also taken further initiatives to enhance interoperability in fund transfers. On November 1, 2025, BB introduced an interoperable money transfer system among banks, PSPs, and MFS providers. The system allows instant transfer from mobile wallets, bank accounts, non-bank accounts, or institutional accounts directly into any other account. Furthermore, to support merchants and accelerate the adoption of interoperable Bangla QR, BB mandated that payments made through Bangla QR must be credited instantly to the merchant’s bank or MFS account, effective from 15th December 2025. These initiatives aim to enhance efficiency, reduce transaction frictions, and advance the development of a fully integrated digital payment ecosystem in Bangladesh.

Furthermore, BB has initiated the development of an inclusive Instant Payment System (IIPS) to strengthen interoperability further and meet the growing demand for cashless payments. The initiative is being implemented in collaboration with domestic and international stakeholders, marking another significant step toward building a seamless, inclusive digital payment infrastructure.

Security Concerns in QR-Based Payment Systems. The Bangla QR code has been developed in accordance with the EMVCo standard, which provides globally recognized specifications for secure QR-based payment transactions. Accordingly, acquirers and issuers are required to adopt the security features prescribed by EMVCo for the related security. Furthermore, they must comply with the BB’s “ICT Security for Banks and Non-Bank Financial Institutions” guidelines, which outline controls for secure system design, authentication, and data protection. These regulatory measures aim to strengthen the overall resilience of the Bangla QR payment ecosystem and safeguard users against emerging cyber threats.

Although QR-based payment adoption in Bangladesh is not yet as extensive as in many other countries, it is essential to recognise and address the evolving risks associated with its use. Since QR-based payments rely on smartphones and internet connectivity, users may face threats arising from weak anti-phishing protections and greater exposure to social engineering attacks, leading to significant cybersecurity vulnerabilities. Moreover, because QR codes are machine-readable rather than human-readable, attackers can easily embed malicious URLs (Uniform Resource Locator), phishing links, or malware without offering any visible cues to alert users.

QR codes can also facilitate advanced cyberattacks such as cross-site scripting (XSS), SQL (Structured Query Language) injection, or reader application exploitation, enabling attackers to steal user credentials, execute unauthorised commands, or access sensitive data. Payment-related QR codes are particularly at risk, as malicious actors may replace or overlay legitimate codes with fraudulent ones to divert funds. The ease of generating QR codes, coupled with limited authentication mechanisms, further amplifies these threats.

To mitigate these challenges, researchers recommend a multi-layered defence strategy that combines digital signatures and other cryptographic validation methods with machine-learning–based malicious-link detection, two-factor authentication, and user-awareness programs. Ensuring the security of QR code–based payment transactions, therefore, requires both robust technical safeguards and informed user behaviour.

[Last part will appear tomorrow]

The article is an abridged version of the BB Working Paper No 2501. Md Rashel Hasan, Additional Director;

Md Khorshed Alam, Joint Director; and Mst Nurnaher Begum, Director; Chief Economist’s Unit, Bangladesh Bank. The views expressed in the paper are solely those of the authors. rashel.hasan@bb.org.bd. The full paper is available at: https://www.bb.org.bd/en/index.php/publication/

workingpaperlist

© 2026 - All Rights with The Financial Express