Question (Q) Agent banking is now being considered as a cost-effective banking approach particularly in the least developed areas. Could you please explain the journey of agent-based banking service of your bank?

Question (Q) Agent banking is now being considered as a cost-effective banking approach particularly in the least developed areas. Could you please explain the journey of agent-based banking service of your bank?

Answer (A) Midland Bank recognizes the transformative potential of Agent Banking as a cost-effective and inclusive solution for providing financial services to the underserved and under developed areas of the country. Our journey in Agent Banking reflects our commitment to financial inclusion, innovation, and community empowerment. Since 2017, Midland Bank identified Agent Banking as a strategic channel to bridge the gap between traditional banking and underserved populations. The objective was to offer convenient, secure and affordable banking services, particularly in rural and semi-urban regions where banking infrastructure is limited. Our Agent Banking initiative was officially launched in 2017. The program began with a pilot project, focusing on select regions to test operational frameworks, technology infrastructure, and agent capacity. Based on the pilot's success, we expanded the service across the country, ensuring coverage in remote areas. Through our Agent Banking Centres, we provide a wide range of services, including - account opening, deposits, withdrawals, facilitating micro-loans to small businesses and farmers, access to mobile banking, fund transfers and utility bill payments.

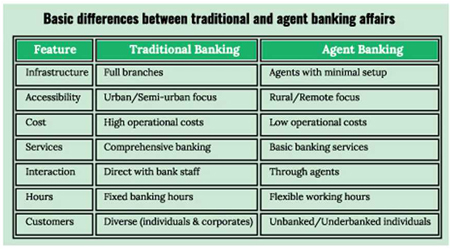

Q: Please share with us the difference between traditional and agent banking affairs?

A: Traditional Banking operates through physical branches with permanent infrastructure, including offices, counters, vaults, and other facilities. Whereas Agent Banking relies on authorized agents or Centres, such as local shops or business centers, equipped with POS systems, biometric devices and basic technology to provide banking services. In terms of service there is no major differences except the nature of customers in Agent Banking are marginal ones.

Q: From when your bank started agent banking services and why?

A: MDB started its operation in 2017 to serve the unbanked people and increase the network coverage of Midland Bank PLC. The decision to introduce Agent Banking was driven by several factors aligned with our mission to enhance financial inclusion and contribute to socio-economic development:

l Financial Inclusion

l Regulatory Encouragement

l Cost Efficiency

l Convenience and Accessibility

l Empowering Local Economies

l Demand for Remittances and Small Savings

Q: How many agent-banking outlets does your bank have so far and their urban-rural ratio?

A: As of 31 December, 2024, MDB has 140 Agent Banking Centres with 115 in rural area and 25 in urban area.

Q: Do you really think agent banking services help expand commercial banks' service network among the unbanked people in a faster and low-cost way? Please answer with an example of your bank?

A: Yes, Agent Banking services significantly help expand commercial banks' service networks among unbanked population in a faster and cost-effective manner. This is particularly true for Midland Bank, where Agent Banking has become a cornerstone of our financial inclusion strategy.

Unlike traditional branches, Agent Banking eliminates the need for large-scale infrastructure and high operational costs. Midland Bank leverages existing local businesses as Agents, enabling us to serve communities with minimal setup costs.

Example-MDB has an Agent Centre in Moshipur, Shahjadpur, Sirajganj where current deposit portfolio is Tk 14.47 Crore, number of A/C-3027 and loan amount Tk 94 Lac.

Q: Many people term agent banking a key deposit-mobilization platform in the banking sector. Could you please share the performance of your bank's agent banking outlets in terms of deposit collection and credit disbursement in recent years?

A: Agent Banking has emerged as a pivotal platform for deposit mobilization within the banking sector, effectively extending financial services to unbanked and underserved populations. Midland Bank has strategically leveraged this model to enhance its deposit collection and credit disbursement capabilities.

As of 31 December, 2024, deposit amount of MDB Agent Banking is Tk. 92.25 Crore and loan amount is Tk 12.07 Crore.

Q: Please tell us the growth of advances of your bank through agent banking along with the account numbers of male users and female users?

A: In 2023, number of loan a/c for male are 77 and female 18 which amount are respectively Tk. 2.03 Crore and Tk 0.76 Crore. In 2024, number of loan a/c for male are 95 and female 29 which amount are respectively Tk 11.11 Crore& Tk. 0.96 Crore.

Q: The growth of deposits with advances in agent banking and their contributions to your bank's entire deposit and lending portfolios?

A: Total loan & advance of MDB is 6,328.50 Crore & total deposit of MDB is 7,520.94 Crore. Agent banking loan and advance is 12.07 Crore & deposit is 92.33 Crore which are respectively 0.19% & 1.22% among the total portfolio of MDB.

Q: What is your bank's plan regarding agent banking in the last two or three years?

A: Agent Outlets will be 250, Deposit amount Tk 175 Crore& Loan amount Tk.25 Crore.

Q: What are the major challenges that need to be overcome for smooth operation and expansion of agent banking across the country?

A: Agent banking has proven to be a transformative model for financial inclusion, but its effective operation and expansion face several challenges that need to be addressed:

l Lack of Awareness and Financial Literacy

Banks should invest in financial literacy campaigns to educate communities about the benefits and security of agent banking

l Limited Infrastructure in Rural Areas

Collaborating with telecom providers to improve internet penetration and deploying solar-powered or offline-capable equipment can address these gaps.

l Agent Management and Training

Comprehensive training programs and periodic performance reviews for agents to ensure they meet service standards.

l Fraud and Security Concerns

Banks should implement robust biometric authentication, end-to-end encryption, and fraud monitoring systems.

l Regulatory Compliance

Streamlined regulatory processes and collaborative frameworks between banks and regulators can ease compliance challenges.

l Liquidity Management

Banks should establish mechanisms for frequent cash replenishment and allow agents to access additional liquidity quickly.

l Customer Trust Issues

Banks should engage with local leaders and community influencers to build trust and provide guarantees for funds.

Moreover, Sub Branches are the major challenges for Agent Banking. Agent Outlets are provided the banking services since the last few years & doing good but Sub Branches are going there rapidly.

Q: Is lending through agent banking too risky as far as NPL (non-performing loan) is concerned?

A: Lending through agent banking can be perceived as riskier compared to traditional lending channels due to several factors, including the challenges of assessing creditworthiness in rural and underserved areas, potential mismanagement at the agent level and the lack of collateral or formal documentation for many borrowers. However, it does not necessarily lead to higher Non-Performing Loan (NPL) rates if properly managed.

Factors Increasing Risks in Lending Through Agent Banking

l Credit Risk in Low-Income Areas

l Limited Agent Oversight

l Lack of Formal Documentation

l Cultural and Financial Literacy Barriers

Mitigating NPL Risks in Agent Banking Lending

l Data-Driven Credit Assessment

l Comprehensive Training for Agents

l Loan Monitoring and Recovery Mechanisms

l Partnerships with Local Leaders or Cooperatives

l Regulatory Safeguards

In some cases, rural people are enjoying the credit facilities from NGO and Cooperative Society who do not report credit facility in Bangladesh Bank CIB. So, potential of NPL risk can be higher.

© 2026 - All Rights with The Financial Express