Coming as a technology-driven hybridization of traditional banks, agent banking has accelerated financial-inclusion initiatives across Bangladesh through bringing more unbanked and underbanked people into the banking network. This way, this banking derivative is contributing to the national effort for achieving the UN-designated sustainable development goals (SDGs).

It is an innovative banking model embedded within traditional banks with the leveraging of technology to deliver tailored products and services to millions of people, particularly from rural areas of Bangladesh.

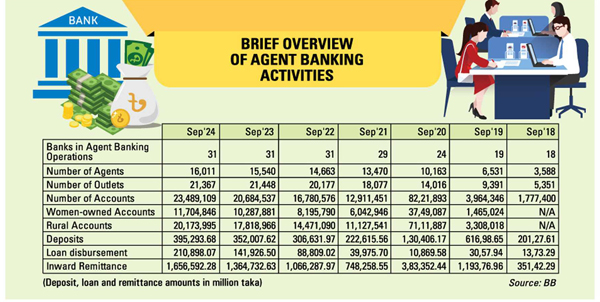

More than 23 million accounts have been opened through 21,367 outlets operated by 16011 agents of 31 scheduled banks since the inception of this banking derivative in 2014.

Agent banking continues to thrive across the country with the scheduled banks currently offering these services. Two state-owned commercial banks, 21 private commercial banks, and eight Islamic banks are running such banking through agents needing no branch setups with hired manpower.

The account-opening numbers indicate a significant potential to integrate rural unbanked population into the formal banking system and thus promote the achievement of SDGs by the 2030 deadline.

The SDGs include 17 goals and 169 targets that set out quantitative and qualitative objectives aimed at eliminating poverty, protecting the planet and ensuring that all people enjoy peace and prosperity.

By providing access to financial services in remote areas, the new model banking helps reduce poverty and inequalities by way of offering savings, credit, and insurance options to the unbanked people.

It is a proven cost-effective model for banks to expand their reach without the need for setting up physical branches. This model reduces operational costs and allows banks to serve remote areas with minimum investment.

Besides, facilitating access to finance particularly for small businesses and entrepreneurs in rural areas stimulates economic activity and job creations, contributing to sustained economic growth.

Furthermore, agent banking is promoting partnerships between financial institutions and technology providers, and the government for creating a cohesive approach to achieving the SDGs.

Actually, agent banking is playing a pivotal role in providing adequate financial services, especially for rural women, small business entrepreneurs and beneficiaries of remitters.

More than 21,000 entrepreneurs, including a certain number of women, have already been developed, particularly in rural areas, during the last 11 years following the introduction of the agent- banking operations in Bangladesh.

Agent banking provides a platform for individuals, especially in rural areas, to become entrepreneurs. By becoming agents, individuals may generate income, gain business experience, and contribute to the economy.

Banks may extend support to the agents by offering training, financial-literacy programmes, and business -development services for enhancing their entrepreneurial capabilities.

After more than one month of issuing the guidelines by the central bank, Bank Asia introduced its agent banking services through establishing Joyinsar outlet at Serajdikhan in Munshiganj district for the first time in Bangladesh on January 17, 2014, aiming to help minimise social inequality through empowering particularly the small-and vulnerable- income groups across the country.

Earlier on December 09, 2013, Bangladesh Bank, the country's central bank, introduced agent banking through issuing a guideline.The central bank has taken the initiative to boost the financial- inclusion campaign through providing a safe alternate delivery channel (ADC) of banking services to the under-served population who generally live in geographically remote locations that are beyond the reach of the formal banking networks.

The BB had issued the guidelines to provide a regulatory framework for the agent banking, which will create an enabling environment for offering such ADC services to the new target group.

All the scheduled banks have been allowed to launch their agent- banking operations to infuse dynamism in the rural economy by offering ADC services using the latest financial technology (FinTech) for the new target group, people living in remote and hill areas of Bangladesh.

FinTech is the new technology and innovation that aims to compete with traditional financial methods in the delivery of financial services by way of using smartphones or the internet.

The report on state of agent banking prepared for the July-September 2024 period by the central bank shows the loan-to-deposit ratio in the agent-banking system was more than 53 per cent although it was over 80 per cent on average in traditional banking. In the last quarter, the ratio was 46.77.

Increase in loan-to- deposit ratio compared to the last quarter indicates that investment through agent outlets is gradually getting momentum.

However, in this quarter, only 23 banks out of 31 distributed loans through agent banking. "The low lending-to-deposit ratio indicates that agent- banking window is serving banks' purpose more on deposit collection than lending," according to the central bank's latest report.

Considering the fact of loan -deposit ratio and the portion of lending to women/entrepreneurs, the central bank is constantly encouraging banks to facilitate CMSME, women- entrepreneurship loan and some refinance schemes for marginal people through agent banking.

The BB is also monitoring the progress closely and emphasizing disbursing loans to rural people to stimulate the rural economy.

Currently, customers may avail banking services like deposits, loans, overseas and local remittances, payment services, and receiving government social -safety-net benefits through agent-banking outlets. But the customer awareness about transactions should be enhanced to avert any possible financial risks.

Banks are operating their agent-banking activities in line with the 'prudential guidelines' for this mode of banking operations in Bangladesh, issued by the central bank on 18 September 2017, covering various aspects that include agent-approval process, permissible activities, responsibilities of the banks and the agents.

It also focuses on the requirements for anti-money laundering and combating financing of terrorism (AML/CFT), and customer protection and business continuity to facilitate "safe and effective proliferation of agent banking" in the country.

The rising trend in agent banking, especially in the rural area, indicates that there is a remarkable potential to bring the rural unbanked people under the umbrella of formal banking services.

Overall, agent banking is having "a significant positive impact on financial inclusion and, therefore, has the potential to fill up the market gap created by an insufficient outreach of branch banking", the central bank explains.

On the other hand, agent banking faces several challenges, including infrastructure constraints, lack of financial literacy, security risks, competition, operational risks and lack of awareness that may hamper its growth and effectiveness in promoting financial inclusion.

A coordinated effort from financial institutions, regulators, and other stakeholders should be taken for addressing these challenges to create a robust, inclusive, and sustainable agent-banking ecosystem in Bangladesh.

Actually, agent banking holds immense potential to transform the financial landscape of Bangladesh by bringing the unbanked population into the formal financial system.

Moreover, continued support from regulatory bodies, coupled with technological innovations and financial literacy, will be crucial for shaping the future of agent banking in Bangladesh.

siddique.islam@gmail.com

© 2026 - All Rights with The Financial Express