Bangladesh is undergoing a major transformation in its financial system as mobile financial services (MFS) increasingly replace cash-based transactions. Over the past decade, digital financial platforms such as bKash, Nagad, and Rocket have expanded financial access to millions of people, particularly those previously excluded from formal banking services. What began primarily as a money-transfer service has now evolved into a broader digital financial ecosystem covering merchant payments, salary disbursement, utility bills, savings, remittances, and small-scale lending.

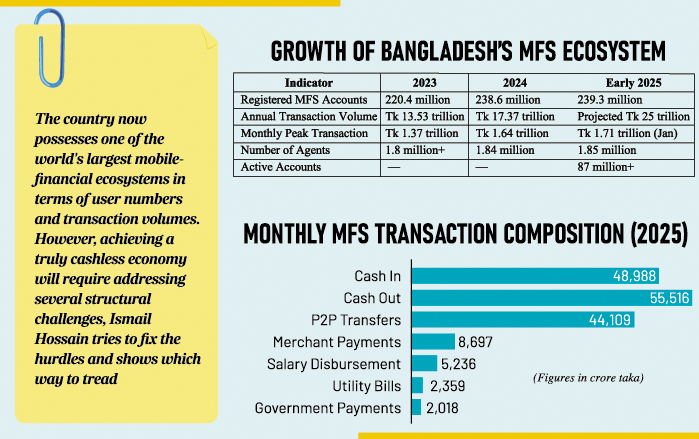

According to Bangladesh Bank data, the country had more than 239 million registered MFS accounts by early 2025. Annual transactions exceeded Tk 17 trillion in 2024, while monthly transactions reached a record Tk 1.64 trillion in December last year. The rapid growth demonstrates how mobile-based financial systems are reshaping economic activities across urban and rural Bangladesh alike.

Expansion of mobile financial services: The expansion of MFS has largely been driven by Bangladesh's high mobile-phone penetration, simplified account-opening systems, and widespread agent networks. Traditional banking services historically remained inaccessible for many low-income and rural citizens because of long travel distances, documentation requirements, and minimum-balance conditions. Mobile financial services provided a low-cost alternative.

Bangladesh now has nearly 1.85 million MFS agents operating across the country. These agents, often small grocery shops or local retailers, function as cash-in and cash-out points, effectively creating a nationwide decentralised banking infrastructure. This extensive network has played a critical role in building public trust in digital transactions.

The fast-growing sector has also benefited from strong policy support aimed at promoting digital financial inclusion and reducing dependence on cash transactions. Government initiatives encouraging digital payments, salary transfers, and social safety-net disbursements have accelerated adoption.

Dominance of bKash: Among all operators, bKash remains market leader and the most influential player in Bangladesh's digital financial transformation. Established in 2011 as a joint venture involving BRAC Bank, the platform succeeded by combining simple technology with a strong agent-based distribution system.

Initially, bKash relied heavily on USSD technology, allowing even feature-phone users to conduct transactions without internet access. This made digital finance accessible to millions who did not own smartphones.

Over time, the company expanded beyond peer-to-peer money transfers into merchant payments, utility bills, education fees, transport ticketing, savings products, and digital loans. During the COVID-19 pandemic, bKash became an important channel for salary payments and government stimulus disbursement, especially in the readymade garment sector.

The company's merchant-payment ecosystem has also expanded rapidly, enabling small shops, pharmacies, restaurants, and transport operators to accept QR-code payments.

Growing competition in MFS Sector:

Although bKash dominates the market, competition has intensified in recent years. Nagad, backed by Bangladesh Post Office, expanded quickly through simplified digital Know Your Customer (dKYC) verification linked with the national identification database. This reduced account-opening time significantly and lowered onboarding costs.

Rocket, operated by Dutch-Bangla Bank, retained a strong position in salary disbursement, industrial payroll management, and utility bill payments.

The growing competition among providers has contributed to lower transaction costs, better digital services, and faster innovation in financial technology or fintech.

Rising merchant payments: One of the most important indicators of a cashless economy is the growth of merchant payments. Bangladesh has experienced significant expansion in digital retail transactions as businesses increasingly accept MFS payments.

According to Bangladesh Bank statistics, merchant payments through MFS platforms crossed Tk 86 billion monthly in early 2025. QR-code payment systems are now common in urban shops, restaurants, pharmacies, supermarkets, and ride-sharing services. The expansion of merchant payments has several economic advantages. It reduces the risks associated with carrying cash, lowers cash-handling costs for businesses, improves transaction transparency, and helps integrate small enterprises into the formal economy.

However, cash transactions still dominate many sectors, particularly in rural areas and informal markets.

Cash-out dependency remains a major challenge: Despite the rapid expansion of digital transactions, Bangladesh still faces a major structural challenge: excessive dependence on cash-out transactions. A large share of money transferred through MFS platforms is eventually withdrawn as physical cash from agent points. Monthly cash-out volumes continue to exceed merchant payments by a substantial margin. This suggests that many users still treat digital wallets primarily as temporary transfer channels rather than long-term digital financial accounts.

Several factors contribute to this dependence on cash.

First, many small businesses and local markets still operate entirely in cash. Second, users often lack confidence in storing large balances digitally. Third, limited interoperability between platforms and transaction fees discourage wider digital usage.

Reducing cash-out dependency will be essential if Bangladesh aims to become a genuinely cashless economy.

Digital literacy and inclusion gaps:

Although MFS penetration is high, digital financial literacy remains uneven. Many users, particularly elderly people and rural populations, rely on agents to conduct transactions on their behalf. This dependence can expose users to fraud, hidden charges, and privacy risks.

Limited understanding of digital security practices also increases vulnerability to scams, phishing attempts, and fraudulent phone calls. Cybercriminals frequently target MFS users by attempting to obtain one-time passwords (OTPs) and account information.

To address these issues, financial institutions and regulators need to invest more heavily in public- awareness campaigns and digital financial education.

Another important barrier to deeper digital financial integration is smartphone affordability. Although smartphone usage is increasing, many low-income households still rely on basic feature phones because of the high cost of quality smartphones and mobile internet services.

Advanced MFS applications offer more user-friendly interfaces and support a wider range of services, including savings products, investment tools, and biometric security systems. Users without smartphones remain dependent on limited USSD-based systems.

Experts argue that reducing taxes on entry-level smartphones and promoting locally assembled devices could help accelerate digital inclusion.

Expansion into savings and digital credit:

Bangladesh's MFS sector is now evolving beyond simple transactions into broader digital financial services. Several operators have introduced micro-savings schemes, insurance services, and nano-loans through mobile applications. These services allow low-income users to access formal financial products without visiting bank branches.

Algorithm-based nano-loans are becoming increasingly common. Using transaction histories and behavioural data, MFS operators can assess creditworthiness and provide instant small loans to users.

Digital remittance services have also grown rapidly. Migrant workers abroad can now send money directly into mobile wallets, reducing dependence on traditional exchange houses and improving transaction speed.

These developments are contributing to greater financial inclusion and expanding access to formal economic opportunities.

Cybersecurity and regulatory concerns:

As digital financial transactions increase, cybersecurity has become a major concern. Bangladesh has experienced a growing number of phishing attacks, account hacks, fake customer-service calls, and transaction fraud targeting MFS users. Even small security failures can undermine consumer confidence in digital-finance systems.

The central bank has introduced tighter regulations, revised transaction limits, and enhanced monitoring requirements to reduce fraud risks. However, experts believe stronger safeguards are still needed.

Future regulatory priorities may include multi-factor authentication, AI-based fraud-detection systems, real-time transaction monitoring, and stronger consumer-protection mechanisms.

Importance of interoperability:

The introduction of 'Binimoy,' Bangladesh's interoperable digital transaction platform, represents an important step toward a more integrated digital-financial ecosystem. The platform aims to connect banks, MFS operators, and payment-service providers, enabling smoother cross-platform transactions. Improved interoperability could significantly reduce transaction friction and encourage wider digital payment adoption.

However, transaction charges remain an important issue. Many small businesses still prefer cash because digital- transaction fees can reduce profit margins. Lowering these costs will be critical for expanding merchant adoption.

The future: Bangladesh has made remarkable progress in digital financial inclusion through the rapid expansion of mobile- financial services. Platforms such as bKash, Nagad, and Rocket have transformed how millions of people send money, receive salaries, pay bills, and access financial services.

The country now possesses one of the world's largest mobile- financial ecosystems in terms of user numbers and transaction volumes. However, achieving a truly cashless economy will require addressing several structural challenges, including cash-out dependency, limited digital literacy, smartphone affordability, cybersecurity risks, and interoperability barriers.

If these challenges can be managed effectively, Bangladesh has the potential to become one of the leading examples of digital financial transformation among developing economies.

© 2026 - All Rights with The Financial Express