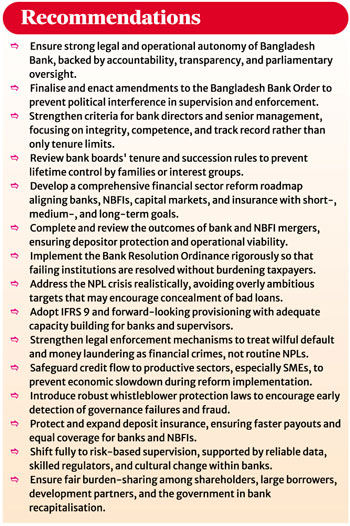

The banking sector of Bangladesh has been under intense strain after years of weak governance, political interference, and regulatory failure. Doctored financial statements and large-scale loan defaults have eroded public confidence and threatened overall economic stability. The central bank, under the present interim administration, has, however, initiated a series of reforms aimed at stabilising the system and protecting depositors with the sector stakeholders feeling the necessity of greater and sustained reforms. Against such a backdrop, The Financial Express organised a roundtable discussion titled "Banking Sector Reforms" to facilitate informed dialogue on the need for reforms. Finance Adviser Dr Salehuddin Ahmed graced the event as the chief guest and Bangladesh Bank Governor Dr Ahsan H Mansur as the special guest. The Financial Express Editor and CEO Shamsul Huq Zahid chaired the event where BIBM Professor Dr Shah Md. Ahsan Habib presented the keynote paper. FE's Head of Online & Multimedia Shiabur Rahman (Shihab) moderated the discussion.

Dr Salehuddin Ahmed

Adviser, Ministry of Finance

Dr Ahsan H. Mansur

Governor, Bangladesh Bank

We decided that we will not constitute any commission; rather we will implement reforms through direct task force. And we have already formed three separate task forces on banking sector reform, Bangladesh Bank reform, and asset recovery. We started reform tasks directly through formation of the task forces because we understood that commissions would take a long time, and the economy cannot wait. The proposal for amendments to Bangladesh Bank Order is an outcome of the Bangladesh Bank Reform Task Force. We have seen that many industries were affected over the years for political and economic reasons, and due to crises like COVID-19 and the Ukraine-Russia war. Some factories were at risk of closing, and we decided to keep them running irrespective of the political affiliation of the owners. We believe politics should not destroy business. This is the biggest difference the current administration has with the 1/11 regime. Had we run the financial sector with 'mob culture' mind set after the political changeover, half of the economy would have been destroyed. Given circumstances, we tried our best to save the industry and economy. We have taken an approach, forming Joint Investigation Teams (JITs), comprising representatives from relevant agencies, to address financial crimes. What the next government should ultimately do is forming National Crime Agency like in the UK. Crimes will keep happening in the financial sector and we have to have a mechanism to contain them and go after the culprits. We have to maintain the nature of the joint investigation task force. We have managed to have two important laws passed - on deposit insurance and bank resolution, which we are actively applying, including for NBFIs. Now we are trying to have passed the amendments to the Money Loan Court law without which it will be difficult to recover money. The Bank Company (Amendment) Act is critical, and we need to ensure it is passed to strengthen banking governance. We have worked to reduce regulatory overreach, giving more operational power to banks while maintaining necessary oversight.

We decided that we will not constitute any commission; rather we will implement reforms through direct task force. And we have already formed three separate task forces on banking sector reform, Bangladesh Bank reform, and asset recovery. We started reform tasks directly through formation of the task forces because we understood that commissions would take a long time, and the economy cannot wait. The proposal for amendments to Bangladesh Bank Order is an outcome of the Bangladesh Bank Reform Task Force. We have seen that many industries were affected over the years for political and economic reasons, and due to crises like COVID-19 and the Ukraine-Russia war. Some factories were at risk of closing, and we decided to keep them running irrespective of the political affiliation of the owners. We believe politics should not destroy business. This is the biggest difference the current administration has with the 1/11 regime. Had we run the financial sector with 'mob culture' mind set after the political changeover, half of the economy would have been destroyed. Given circumstances, we tried our best to save the industry and economy. We have taken an approach, forming Joint Investigation Teams (JITs), comprising representatives from relevant agencies, to address financial crimes. What the next government should ultimately do is forming National Crime Agency like in the UK. Crimes will keep happening in the financial sector and we have to have a mechanism to contain them and go after the culprits. We have to maintain the nature of the joint investigation task force. We have managed to have two important laws passed - on deposit insurance and bank resolution, which we are actively applying, including for NBFIs. Now we are trying to have passed the amendments to the Money Loan Court law without which it will be difficult to recover money. The Bank Company (Amendment) Act is critical, and we need to ensure it is passed to strengthen banking governance. We have worked to reduce regulatory overreach, giving more operational power to banks while maintaining necessary oversight.

Mahbubur Rahman

President, International Chamber of Commerce Bangladesh

Shamsul Haq Zahid

Editor & CEO, The Financial Express

The banking sector, in a dire state, needs massive reforms. For years, some banks doctored their financials, hiding the true picture. Political interference in loan sanctioning, frequent amendments favouring certain groups, and regulatory indulgence allowed looters to prey on depositors' money. Since the collapse of the autocratic regime, the central bank, with the Ministry of Finance, has worked hard to protect depositors, merging five Islami banks into one. These steps have restored some confidence, but non-performing loans remain huge - nearly a third of total loans. The central bank initially took a tough stance on defaulters but later softened to save jobs in large manufacturing units linked to cronies. The issue of Bangladesh Bank's autonomy is critical. Legislation alone won't ensure independence; the culture of political interference must end, though guaranteeing non-interference in Bangladesh is challenging.

The banking sector, in a dire state, needs massive reforms. For years, some banks doctored their financials, hiding the true picture. Political interference in loan sanctioning, frequent amendments favouring certain groups, and regulatory indulgence allowed looters to prey on depositors' money. Since the collapse of the autocratic regime, the central bank, with the Ministry of Finance, has worked hard to protect depositors, merging five Islami banks into one. These steps have restored some confidence, but non-performing loans remain huge - nearly a third of total loans. The central bank initially took a tough stance on defaulters but later softened to save jobs in large manufacturing units linked to cronies. The issue of Bangladesh Bank's autonomy is critical. Legislation alone won't ensure independence; the culture of political interference must end, though guaranteeing non-interference in Bangladesh is challenging.

Dr Shah Md Ahsan Habib

Professor, Bangladesh Institute of Bank Management (BIBM)

A K Azad

Chairman, Shahjalal Islami Bank PLC

We have been hearing about the proposed Banking Commission and reforms for a long time. We need reforms not just for government banks, where 50% of loans are classified, but also for many private banks. Many private banks need mergers. The boards of private banks remain unchanged for decades. Why should someone serve more than three years, with their family or associates taking over after them? We need a system to prevent lifetime board positions. Much has been achieved in the past one and a half years. Many bold steps have been taken that could have taken five years otherwise. Still, some defaulters have received repeated opportunities, which creates unfair competition. I urge a review of these policies before the current leadership leaves.

We have been hearing about the proposed Banking Commission and reforms for a long time. We need reforms not just for government banks, where 50% of loans are classified, but also for many private banks. Many private banks need mergers. The boards of private banks remain unchanged for decades. Why should someone serve more than three years, with their family or associates taking over after them? We need a system to prevent lifetime board positions. Much has been achieved in the past one and a half years. Many bold steps have been taken that could have taken five years otherwise. Still, some defaulters have received repeated opportunities, which creates unfair competition. I urge a review of these policies before the current leadership leaves.

Taskeen Ahmed

President, Dhaka Chamber of Commerce & Industry (DCCI )

Mohammad Hatem

President, BKMEA

The business situation is worsening. Many factories have shut down - 278 so far - and more are at risk. In export, buyers take goods on deferred payments of 120-180 days but often delay payment. When payment is delayed, banks immediately stop back-to-back LCs and other facilities, making it impossible to ship goods on time. What will happen to the businesses which are being affected by non-cooperation of banks? Let me highlight Section 18B of Foreign Exchange Regulation Act, which deals with registration of buying houses. That registration provision has stopped and now buying houses are accountable to none. The current system forces exporters to rely on intermediaries who delay payments, which is unfair and risky.

The business situation is worsening. Many factories have shut down - 278 so far - and more are at risk. In export, buyers take goods on deferred payments of 120-180 days but often delay payment. When payment is delayed, banks immediately stop back-to-back LCs and other facilities, making it impossible to ship goods on time. What will happen to the businesses which are being affected by non-cooperation of banks? Let me highlight Section 18B of Foreign Exchange Regulation Act, which deals with registration of buying houses. That registration provision has stopped and now buying houses are accountable to none. The current system forces exporters to rely on intermediaries who delay payments, which is unfair and risky.

Syed Abu Naser Bukhtear Ahmed

Chairman, Agrani Bank PLC

Dr Arifur Rahman

Chairman, Premier Bank PLC

We often ask whether the thief or the lock came first. We all know first came the thief. We should give thanks to the "thieves" who taught us how to make better locks. While we criticise those who stole from our banks and fled, we should acknowledge that they have taught us how to protect our systems. I want to give a standing ovation to our Governor, Ahsan H. Mansur, who has effectively "locked everyone," ensuring our banking system is much safer.

We often ask whether the thief or the lock came first. We all know first came the thief. We should give thanks to the "thieves" who taught us how to make better locks. While we criticise those who stole from our banks and fled, we should acknowledge that they have taught us how to protect our systems. I want to give a standing ovation to our Governor, Ahsan H. Mansur, who has effectively "locked everyone," ensuring our banking system is much safer.

However, as a banker, I feel that providing relief loans to borrowers has affected banks' income. A possible solution is for the central bank to allow commercial banks to have deposits at lower rates, similar to government banks, which would benefit all.

Sharif Zahir

Chairman, United Commercial Bank PLC

Md Ali Hossain Prodhania

Chairman, NRBC Bank PLC

In the late eighties, classified loans went beyond 50 per cent, but today the percentage looks lower. The reality, however, is different. Earlier, loans were classified mainly due to business failure, but now looted and stolen money has entered the loan system. If we do not clearly separate genuine classified loans from outright theft, the burden of these loans will remain on the banking sector indefinitely unless they are written off. When loans are diverted, misused, or stolen, they should not be treated as normal defaults. Theft is a different matter and needs a different legal and recovery approach. Through forensic audits, we often see that a significant amount of money is still traceable within the banking system.

In the late eighties, classified loans went beyond 50 per cent, but today the percentage looks lower. The reality, however, is different. Earlier, loans were classified mainly due to business failure, but now looted and stolen money has entered the loan system. If we do not clearly separate genuine classified loans from outright theft, the burden of these loans will remain on the banking sector indefinitely unless they are written off. When loans are diverted, misused, or stolen, they should not be treated as normal defaults. Theft is a different matter and needs a different legal and recovery approach. Through forensic audits, we often see that a significant amount of money is still traceable within the banking system.

Helal Ahmed Chowdhury

Chairman, BASIC Bank PLC

Syed Mahbubur Rahman

Managing Director, Mutual Trust Bank PLC

The key issue we face in the banking sector is shattered trust. Political resistance is widespread, and powerful borrowers with political connections often push back against accountability. Regulatory weaknesses are evident, with limited supervisory capacity, especially in risk-based supervision, stress testing, and early-warning systems. Legal and judicial bottlenecks delay loan recovery for years, which encourages a culture of tolerance for default. Weak corporate governance allows directors to prioritise personal and political agendas over fiduciary duty. State-owned banks remain fragile, chronically undercapitalised, and vulnerable to political misuse. To address these problems, regulatory independence must be enforced through updated banking company orders and amendments to the Banking Companies Act.

The key issue we face in the banking sector is shattered trust. Political resistance is widespread, and powerful borrowers with political connections often push back against accountability. Regulatory weaknesses are evident, with limited supervisory capacity, especially in risk-based supervision, stress testing, and early-warning systems. Legal and judicial bottlenecks delay loan recovery for years, which encourages a culture of tolerance for default. Weak corporate governance allows directors to prioritise personal and political agendas over fiduciary duty. State-owned banks remain fragile, chronically undercapitalised, and vulnerable to political misuse. To address these problems, regulatory independence must be enforced through updated banking company orders and amendments to the Banking Companies Act.

Mohammad Naser Ezaz Bijoy

CEO, Standard Chartered Bank Bangladesh

Mohammad Ali

Managing Director, Pubali Bank PLC

I want to start by talking about political affiliation. When the board changed due to state sponsorship, boards were reformed overnight, and foreign investors were forced to leave banks. This created an asset bubble, which was a major reason for instability. If this had not happened, classification issues would have been minor. At that time, independent directors, including myself, observed the situation and how Bangladesh Bank gained autonomy. The banking sector must be free from political hostility so that strategic partners, especially foreign investors, remain unaffected. Another key issue is bank governance. Loan sanction should not be approved by the executive committee; it should be vested on the management.

I want to start by talking about political affiliation. When the board changed due to state sponsorship, boards were reformed overnight, and foreign investors were forced to leave banks. This created an asset bubble, which was a major reason for instability. If this had not happened, classification issues would have been minor. At that time, independent directors, including myself, observed the situation and how Bangladesh Bank gained autonomy. The banking sector must be free from political hostility so that strategic partners, especially foreign investors, remain unaffected. Another key issue is bank governance. Loan sanction should not be approved by the executive committee; it should be vested on the management.

Alamgir Hossain

Managing Director, Citizens Bank PLC

Sohail R K Hussain

Managing Director, Bank Asia PLC

What has really driven the current banking sector reforms is a complete failure of governance and the breakdown of checks and balances over the last ten years. Reforms are always necessary, but this is not a routine situation. We need to ask whether the solutions being proposed are truly adequate and whether they match international best practices. Bangladesh is not the first country to face this kind of crisis, so there are lessons to learn. The caps and restrictions proposed by the central bank have strong justification, but by themselves they are not enough. In banking, boards, management, auditors, rating agencies, and regulators have their roles in ensuring a check and balance. What happened in the last decade shows that this entire chain was weakened by political influence and lack of will.

What has really driven the current banking sector reforms is a complete failure of governance and the breakdown of checks and balances over the last ten years. Reforms are always necessary, but this is not a routine situation. We need to ask whether the solutions being proposed are truly adequate and whether they match international best practices. Bangladesh is not the first country to face this kind of crisis, so there are lessons to learn. The caps and restrictions proposed by the central bank have strong justification, but by themselves they are not enough. In banking, boards, management, auditors, rating agencies, and regulators have their roles in ensuring a check and balance. What happened in the last decade shows that this entire chain was weakened by political influence and lack of will.

Rizwan Dawood Shams

Managing Director, IPDC Finance PLC

M Khurshed Alam

Additional Managing Director, NCC Bank PLC

I want to highlight key legal issues for banking sector reforms. I suggest that if any writ petition is filed against a bank's suit or execution case, no stay order should be allowed without hearing the bank. Any challenge to a bank's order should require depositing 20% of the suit value with the bank or Bangladesh Bank. Special training should be arranged by Bangladesh Bank and the Judicial Service Commission for presiding judges of these cases. I propose forming five special benches in the High Court Division to handle Arthorin cases efficiently. Banks should have the power to impose travel restrictions on defaulting borrowers and to publish the names and addresses of defaulters and guarantors in newspapers.

I want to highlight key legal issues for banking sector reforms. I suggest that if any writ petition is filed against a bank's suit or execution case, no stay order should be allowed without hearing the bank. Any challenge to a bank's order should require depositing 20% of the suit value with the bank or Bangladesh Bank. Special training should be arranged by Bangladesh Bank and the Judicial Service Commission for presiding judges of these cases. I propose forming five special benches in the High Court Division to handle Arthorin cases efficiently. Banks should have the power to impose travel restrictions on defaulting borrowers and to publish the names and addresses of defaulters and guarantors in newspapers.

Doulot Akter Mala

President, Economic Reporters' Forum (ERF)