![]() In Bangladesh, the landscape of financial inclusion has undergone a massive change as reflected in the stark contrast between deposit accounts in rural and urban areas. A notable trend has emerged with deposit accounts in rural areas surpassing the total number in urban areas by more than six-fold. This phenomenon suggests a remarkable improvement in banking accessibility for the rural and underprivileged populace, primarily facilitated through the burgeoning system of agent banking.

In Bangladesh, the landscape of financial inclusion has undergone a massive change as reflected in the stark contrast between deposit accounts in rural and urban areas. A notable trend has emerged with deposit accounts in rural areas surpassing the total number in urban areas by more than six-fold. This phenomenon suggests a remarkable improvement in banking accessibility for the rural and underprivileged populace, primarily facilitated through the burgeoning system of agent banking.

The significant surge in deposit accounts in rural areas points to proactive efforts to bridge the financial inclusion gap between urban and rural communities. This shift is largely attributed to the expanding reach of agent banking, where financial services are extended to remote locations through intermediaries.

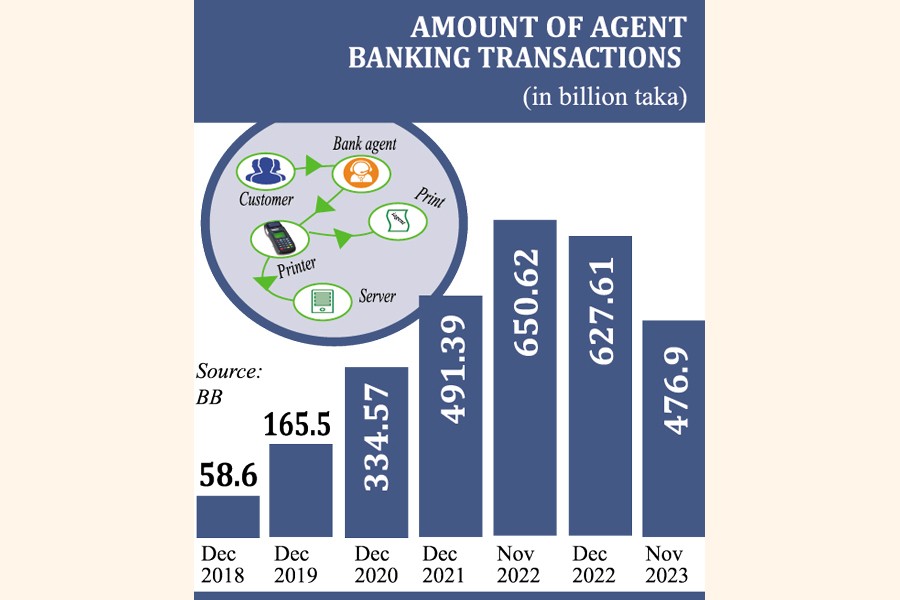

Agent banking services were formally introduced in Bangladesh in 2013, spearheaded by Bank Asia and Agrani Bank. Subsequently, other banks have extended these services up to the union level, broadening their accessibility across the country. At present, 31 banks are operating such services in the country.

Agent banking services were formally introduced in Bangladesh in 2013, spearheaded by Bank Asia and Agrani Bank. Subsequently, other banks have extended these services up to the union level, broadening their accessibility across the country. At present, 31 banks are operating such services in the country.

Agent banking is providing financial services to rural and underprivileged people who get less access to traditional banking facilities.

Moreover, it is encouraging participation of women in financial activities. The higher activities under such banking in rural areas indicate the financial inclusion of more marginal people.

Rural outlets exceeded urban outlets by nearly six-fold until November last year, indicating extensive coverage of banking facilities in rural areas through such banking, according to the latest Bangladesh Bank (BB) data.

In 2017, the central bank had issued a policy guideline on this matter.

As of November 2023, the total number of agents and outlets were 15,581 and 21,506 respectively, the BB data reveals. The number of urban and rural agents stood at 2,461 and 13,120, respectively.

Until November last year, the cumulative number of accounts reached 21.20 million, accompanied by a deposit balance of Tk 351.69 billion. In comparison, October witnessed a total of 20.93 million accounts with deposits amounting to Tk 350.50 billion.

The crucial remittance inflow through agent banking reached Tk 21.24 billion in November whereas it stood at Tk 20.47 billion in October, according to the BB data.

When it comes to outstanding loans, disbursement and recovery, the BB data showed that the outstanding balance in November stood at Tk. 83.87 billon, of which Tk 23.95 billion was in urban areas and Tk. 59.92 billion in rural areas. The urban-rural outstanding ratio is 1:2.50, which indicates that disbursement in rural areas is more than twice that in urban areas.

The total disbursed amount was Tk. 8.57 billion for the month of November while the loan recovery during the month was Tk. 5.45 billion. Microcredit loans are disbursed more preferably through such banking outlets compared to the traditional banking system, as per BB data.

According to the central bank, some 15,581 agents were deployed with 21,506 outlets in November, while it was 15,542 agents with 21,463 outlets in October.

In November, 2481 agents were operating in urban areas and 13,100 agents in rural areas. This marked an increase from October when there were 2,480 agents in urban areas and 13,062 agents in rural areas.

Amid the current economic scenario, loan disbursement through agent banking increased by 5.56 per cent in November last year from October's over Tk 8.09 billion, according to the BB data.

In November, the number of female account holders reached over 10.51 million while male account holders totalled 10.35 million. This shows an increase from October when there were over 10.39 million female account holders and more than 8.48 million male account holders.

In November, agent banking services facilitated the payment of electricity, gas, and water bills amounting to Tk 1.21 billion, compared to more than Tk 1.56 billion in October.

Syed Mahbubur Rahman, Managing Director & CEO of Mutual Trust Bank Limited (MTB), has highlighted the significant growth of agent banking over the past decade. This expansion has seen a notable increase in deposit collection, remittance inflow, and loan disbursement, positively impacting financial inclusion, particularly in rural areas.

However, Mr Rahman emphasised a critical concern regarding the nomination of agents by banks.

He pointed out instances where agents, taking advantage of the predominantly uneducated and simple-minded customers, engaged in fraudulent activities. To address this issue, Mr Rahman proposed that banks should actively nominate agents who could effectively promote and conduct transactions, reaching out to people at their doorsteps to explain the benefits of such services.

To curb fraudulent activities, Mr Rahman also suggested restricting transactions only within the branches, ensuring a secure environment. He also highlighted a challenge where sub-branches of different banks sometimes outperformed agent banking. Additionally, he noted that the volume of loans was smaller than deposits.

Mr. Rahman stressed the importance of raising awareness, especially in rural areas, to encourage participation in agent banking. He called for regulatory guidelines to be simplified especially where multiple regulators were involved and proposed incorporation of corporates to instil confidence in people and boost the credibility of agent banking.

Regarding location and region-wise distribution of agents and outlets until November last year, the latest BB data reveals that Dhaka division has the maximum 3,996 agents (26 per cent) and Mymensingh division has the minimum 841 agents (6.0 per cent). When it comes to outlets, Dhaka division has the maximum 5,376 outlets (25 per cent) and Mymensingh division has the minimum 1,223 outlets (6.0 per cent).

Such banking business is higher in both Dhaka and Chattogram divisions compared to other divisions. Furthermore, district-wise information suggests that Dhaka district has the highest number of agents and outlets, which are 1,035 and 1,180, respectively. In addition, Bandarban has the lowest number of agents and outlets, which are 32 and 40, respectively. Also, at the upazila level, Lakshmipur Sadar has the highest number of agents, which is 113 and Savar has the highest number of outlets, which is 172. Ruma upazila has the lowest number of agents and outlets. There is only one agent and one outlet in this upazila.

Until November last, the central bank data showed that private banks were in the first position with respect to the number of agents and outlets. The state-owned banks were in the last position.

In terms of percentage of agents, private commercial banks (PCBs) had the maximum number of agents at 10,849. It was 70 per cent of the total agents. Islamic banks (IBs) possess 3,938 agents which are 25 per cent of total agents. Moreover, 794 agents or 5.0 per cent of the total are occupied by the state owned banks (SOBs).

When it comes to outlets, private commercial banks (PCBs) have the largest number of outlets at 16,543 or 77 per cent of the total. Islamic banks (IBs) possess 4,169 outlets or 19 per cent of the total. Moreover, State-owned banks (SOBs) account for 794 outlets or 4.0 per cent of the total. Zafar Alam, Managing Director & CEO of Social Islami Bank PLC, highlights the challenge of high costs in traditional banking hindering financial services for the economically-disadvantaged people.

He points out that catering to customers' need with modest balances through conventional methods becomes economically unfeasible. Consequently, there's a need for banks to explore more cost-effective approaches, such as agent banking, to provide accessible and secure formal financing for agriculture and rural SMEs.

Mr. Alam emphasises that these innovative delivery models not only enhance financial inclusion but also transform the economic landscape for underserved rural communities. Through such initiatives, banks can now effectively address the financial needs of individuals with limited resources, making formal financing a viable option for rural SMEs and agriculture.

Mr. Alam stresses the importance of adapting banking practices to meet the unique requirements of rural populations, fostering economic growth and development in these underserved communities.

How does agent banking work?

The agent banking model ensures real-time banking for customers at agent points, providing services equivalent to those at the main branch. Only for the sake of additional security, work is done at the agent point using biometric devices, meaning everyone has to operate by providing their fingerprint. Fingerprint verification is mandatory when opening a primary bank account.

Individuals can open an account at an agent point or access various services if they already have an account at another branch. This includes activities such as withdrawing and depositing money, remittance, and transferring funds between different bank accounts, both within the same bank and across other banks.

Who can be agents?

Individuals eligible to become agents include regulated NGOs and other NGOs registered by the Microcredit Regulatory Authority of Bangladesh, cooperative societies (under the Cooperative Societies Act 2001), postal offices registered under the Ministry of Posts and Telecommunications, courier and mailing service companies registered under the Companies Act, agents of mobile network operators, offices of local government institutions in rural and urban areas, union information and service centres, IT-based financial services, agents of insurance companies, pharmacy owners, grocery store owners, and individuals capable of managing and operating petrol pumps/gas stations and any organisation recommended or approved by the Bangladesh Bank.

However, an agent of one bank cannot be an agent of another bank.

Agents must maintain and secure the electronic devices provided by the bank for monitoring and recording all transactions. They are required to assist the bank in auditing. The responsibility for distributing loans and collecting instalments also lies with the agent.

Agents are not allowed to impose any additional charges, and transactions cannot be conducted without fingerprint verification and a card.

sajibur@gmail.com

© 2026 - All Rights with The Financial Express