![]() The insurance sector of the country reached a major milestone in 2023 with introduction of bancassurance-a partnership between insurers and banks. It ushered in a new era, creating an opportunity for one of the country's most underdeveloped financial services to scale a new height.

The insurance sector of the country reached a major milestone in 2023 with introduction of bancassurance-a partnership between insurers and banks. It ushered in a new era, creating an opportunity for one of the country's most underdeveloped financial services to scale a new height.

Though this new-found market in Bangladesh is still at a nascent stage, insurers who have been using this model told The Financial Express (FE) that the early response had been highly encouraging.

Bancassurance is typically aimed at streamlining the claim settlement process while offering customers more accessible, convenient, and transparent ways to purchase and manage insurance policies. Popular in many countries abroad, including neighbouring India, the model allows customers to buy insurance policies through trusted banking channels.

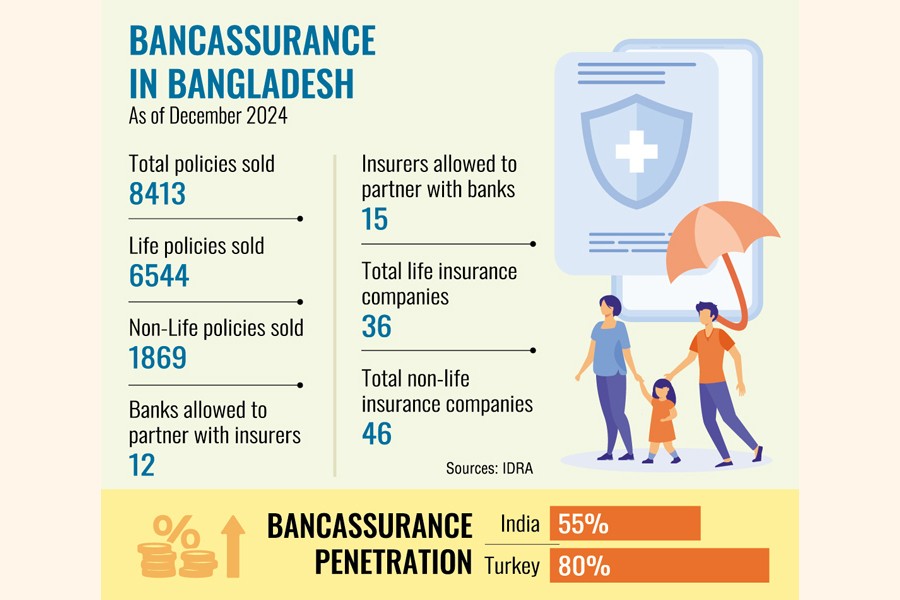

In 2022 bancassurance accounted for 55 per cent of the total insurance business in India, up from nearly 20 per cent in 2016, according to a FALIA survey. In Turkey, the model commands an even greater presence, with a market share exceeding 80 per cent.

In Bangladesh, banks began formally selling insurance products under this model after receiving regulatory approval from the Insurance Development and Regulatory Authority (IDRA) in September 2023. Since then, the model has gained momentum.

As of December 2024, a total of 8,413 insurance policies had been sold through bank branches-6,544 of which were life insurance policies and 1,869 non-life, according to data available with IDRA.

So far, 15 insurance companies and 12 banks have received approval to offer bancassurance services.

MetLife Bangladesh has been involved with the process from the very beginning of this initiative, partnering with three leading banks-BRAC Bank, Eastern Bank, and Standard Chartered Bank-to make international-standard insurance services more accessible for the local bank customers.

"While it's still early days, the response has been encouraging," said Mr. Ala Ahmad, CEO of MetLife Bangladesh.

He noted that in the initial phase the focus had been less on achieving high sales volumes, rather the full focus had been on building the foundation-such as integrating systems between banks and insurers, training bank staff, and ensuring insurance solutions tailored for banking customers.

"Insurance is a relatively new product for banks to offer, so ensuring alignment, support, and understanding has been a key priority," he said.

MetLife has prioritised optimising customer footprints and ensuring seamless and trustworthy services for the sake of better experiences of the clients.

"Looking ahead, bancassurance has high potential to complement the traditional agent-led sales channel," Mr. Ahmad told the FE about the progress in popularising the model in the country.

Mr. Ahmad suggested allowing insurers to partner with more than three banks and that could accelerate the model's success and unlock the greater potential of both banks and insurers.

Guardian Life Insurance, one of the newer and more dynamic players in the life insurance market, also embraced bancassurance from the start. It issued the first-ever life insurance policy under this model-a landmark moment for the industry.

The company has led from the front in digital innovation, launching a fully digital, end-to-end onboarding process that simplifies policy issuance and enhances the customer experience.

As of April 25, 2025, Guardian Life issued more than 5,200 policies through partnerships with City Bank PLC, Dutch-Bangla Bank PLC, and Mutual Trust Bank PLC.

The model leverages the credibility of banks to build customer trust while reducing distribution costs for insurers, who can now rely on bank networks instead of maintaining large, expensive sales teams, the insurer said.

"This combination of cost efficiency, convenience, and trust positions bancassurance as a promising growth engine aiding expansion of financial protection and increase in insurance penetration in Bangladesh."

However, despite early successes by players like Guardian Life and MetLife, many other insurers have yet to tap the strategic opportunity bancassurance offers.

Most still rely on costly, traditional distribution methods and are missing out on the cross-selling potential and customer access that bancassurance offers.

The insurance regulator (IDRA) argued that wider approval might be challenging unless insurers improved in areas such as claim settlement and service quality.

Still, the initial success of bancassurance underscores the need for greater industry awareness and stronger regulatory support to encourage broader adoption and accelerate market development.

Challenges that lie ahead:

The long-term success of bancassurance will depend on sustained collaboration between banks and insurers, along with the regulator's efforts to raise public awareness and facilitate timely claim settlements, product development and other related services.

Product innovation may become a friction point. Banks often want customised insurance products tailored to the need of their clientele. For example, a bank serving clients who frequently send money abroad for their children's education may need a policy designed to meet that specific need.

For such a section of clients, if insurers push for existing products, they will not succeed. Banks increasingly want co-developed or exclusive offers. This difference in approach could create tensions, unless the regulator intervenes to facilitate cooperation in product designing.

A major gap is the lack of insurance-educated professionals in the banking sector. While regulatory guidelines emphasise this issue, the country currently lacks enough skilled personnel familiar with insurance product development, actuarial science, and customer education.

Last not the least, awareness building is also essential. Insurance can be particularly valuable for bank customers with considerable savings. Wealthy clients, for example, may benefit from the tax advantages associated with insurance policies-an aspect that deserves more public promotion.

In conclusion, as Bangladesh's economy grows, developing a stronger, more trusted, and more accessible insurance ecosystem is essential for financial inclusion and long-term security. Bancassurance, if properly nurtured, could be the catalyst that brings insurance into the financial mainstream for millions of people and emerge as a game-changer for the industry.

jasimharoon@yahoo.com

© 2026 - All Rights with The Financial Express