realisation of Sustainable Development Goals (SDGs). The industrial sector has been particularly affected by the inadequate quality of power supply and the lack of sufficient gas. These problems can be attributed to ill-conceived policies and widespread corruption within the sector. Moving forward necessitates a comprehensive analysis of both past processes and the current state of affairs.

realisation of Sustainable Development Goals (SDGs). The industrial sector has been particularly affected by the inadequate quality of power supply and the lack of sufficient gas. These problems can be attributed to ill-conceived policies and widespread corruption within the sector. Moving forward necessitates a comprehensive analysis of both past processes and the current state of affairs.

The dependence on a single fuel source – gas — for electricity generation, along with its shortages and inadequate capacity in 2007, resulted in a severe power crisis. This situation compelled the government to seek quick solutions, leading to an initial rush to construct oil-based rental generation units in 2010. Consequently, this resulted in the rise of oil-based Independent Power Producers (IPP) causing increased oil dependency. Unfortunately, during this period, no significant efforts were made to enhance local supplies of gas, coal, or renewable energy. Expanding coal-based power production was particularly challenging, as the government had previously opposed the establishment of a coal-based power station in Fulbari during its time in opposition. Additionally, there were considerable delays in the development of new baseload power plants, which relied on Liquefied Natural Gas (LNG) and imported coal. As a result, the entire power sector became vulnerable to fluctuations in international energy supply and prices.

In the power sector, there has been a significant mismatch between demand and supply. Additionally, the government opted for an artificially ambitious forecast, disregarding the professional projections of previous master plans. As a result, installed capacity exceeds actual demand. At the same time, this strategy significantly exposed the power sector to the global energy market due to the import of LNG and coal for electricity generation. Critics have suggested that the revision of demand forecasts to justify this increased capacity was driven by unscrupulous motivations, leading to allegations of corruption within the sector.

Current and Projected Power Generation Capacity

As of now, Bangladesh has an effective generation capacity of 26,700 MW, with just 893 MW derived from renewable sources, including a dated 230 MW hydroelectric plant. This figure excludes the 3,700 MW from mainly oil-based rental and Independent Power Producer (IPP) plants that have been phased out after their contracts ended. Furthermore, an additional 6,000 MW of generation capacity, which includes 2,400 MW from nuclear energy, is expected to be added by 2030. The agreements for all Combined Cycle Gas Turbine (CCGT) plants span 22 years, while coal plants have 25-year contracts. If some older plants owned by the Bangladesh Power Development Board (BPDB) are decommissioned and certain IPP contracts come to an end, the country is anticipated to reach around 30,000 MW of power generation capacity, predominantly from fossil fuels, by 2030. Additionally, over 25,000 MW of contractual obligations for power plants extend into 2040 and beyond.

Excess Capacity and Economic Strain

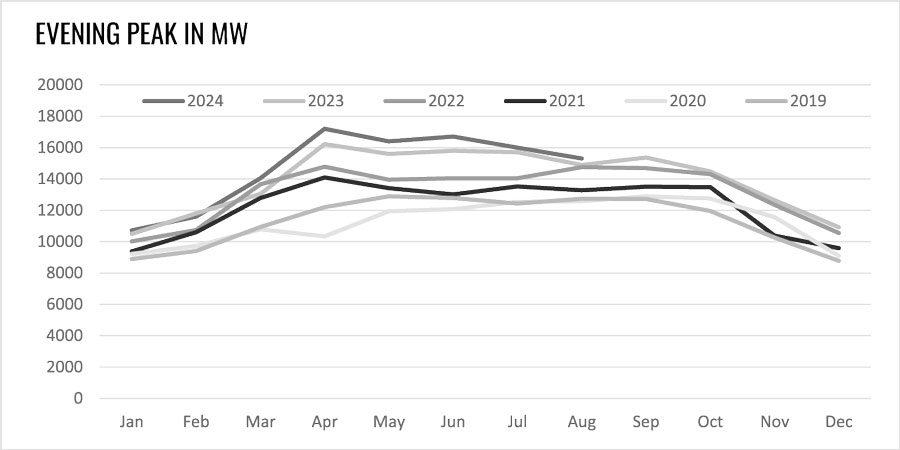

Until the recent retirement of all rental and some Independent Power Producer (IPP) plants, along with non-operational state-owned facilities, an installed capacity of nearly 32,000 MW was claimed. However, due to aging infrastructure, this capacity was derated to approximately 30,000 MW. During peak summer demand in 2024, the highest recorded electricity demand reached 17,000 MW, while production peaked at 16,477211 MW. If 10% of capacity is reserved for standby power and another 10% allocated for maintenance, the total required generation capacity for supplying the remaining 80% is 25,500 MW. Consequently, the country has maintained nearly 5,000 MW of excess capacity, which is 20% more than necessary, leading to significant capacity charges that burden consumers.

With installed capacity far exceeding actual needs and the sector’s heavy reliance on imported primary fuels, the entire economy is at risk, particularly as Bangladesh struggles with foreign exchange shortages necessary to finance essential imports. The Energy Regulatory Commission, which is supposed to oversee the producers and protect consumer interests, has not only failed to monitor this situation but has also justified successive increases in power tariffs. This has imposed a significant fiscal burden on the economy and created a comparative disadvantage by raising the cost of living for the general population and increasing production costs for all producers, putting the competitiveness of the ready-made garment (RMG) sector in jeopardy.

Simultaneously, this misalignment led to an excess investment of approximately $4.48 billion in the sector. Since nearly all private sector Independent Power Producers (IPPs) are owned by Bangladeshi entrepreneurs, this over-investment has heightened Bangladesh’s exposure to the global credit market. Furthermore, many of these investments were secured by sovereign guarantees, which further increased the country’s economic vulnerability to global credit risks.

Operational Challenges and Political Influence

To address the operational challenges of maintaining a stable power supply during both peak and off-peak periods, coal and nuclear plants typically function as baseload power sources, while the majority of gas and dual-fuel plants are combined cycle power plants (CCGTs) that serve primarily for baseload generation. The availability of peaking and intermediate gas turbine power plants is limited. Due to fuel shortages and grid constraints, oil-fired power plants have been relied upon to satisfy both baseload and peak demands. With a sufficient gas supply, CCGTs can modulate their output to accommodate intermediate and peak loads, thereby effectively replacing oil plants and resulting in cost savings. Furthermore, solar energy can offset the use of oil plants during peak daylight hours, reducing oil dependency and lowering production costs. However, the emphasis on meeting peak demand, combined with the rushed installation of only baseload power plants, signifies a failure in planning. Many contend that this is indicative of political interference, where non-professional groups influenced the types and locations of the power plants. This misalignment has led to operational strain and increased production costs. Such allegations appear credible, given the political ties between power plant owners and the ruling government.

Fuel Requirement and its burden

The evolving fuel mix in the power sector has also affected the country’s foreign exchange reserves. The gas-based capacity, including dual-fuel plants, stands at 11,300 MW, which requires 1.8 billion cubic feet per day (Bcfd) of gas to operate at full capacity—over 650 billion cubic feet annually. Approximately 70% of this gas is procured from International Oil Companies (IOCs) under production sharing contracts (PSCs), with payments made in foreign currency based on the equivalent price of crude oil in the Singapore spot market, within a specified minimum and maximum range stipulated by the PSC.

Excluding the Adani power plant, the annual coal requirement for operating 5,670 MW is around 18 million tons. For oil-based power plants, the private sector imported 2.84 million tons and 1.09 million tons of heavy fuel oil (HFO) for the years 2022-2023 and 2023-2024, respectively. During the same period, the Bangladesh Petroleum Corporation (BPC) procured 0.43 million tons and 0.66 million tons of HFO. BPC plans to import 0.55 million tons of HFO and 0.1 million tons of diesel for power plants from October 2024 to June 2025, with an estimated cost of 3,000 crore taka. Since 2018, Bangladesh has purchased a total of 1,360 million MMBTU of LNG from Qatar, Oman, and the spot market, amounting to 164,000 crore taka, including 17% VAT and advance income tax (AIT213.). Imported LNG has supplied about 25% of the total gas needs

As a result, in addition to the strain of over-investment, the power sector also bears the additional burden of operating these plants and paying annual capacity charges associated with them.

Transmission and Distribution (T&D) Limitations

All large baseload coal power plants in the south, along with three new Combined Cycle Gas Turbine (CCGT) plants in the Meghnaghat area, cannot operate at full capacity due to limitations in transmission and distribution capacity, as well as fuel shortages. Additionally, the transmission lines needed to evacuate power from the nuclear plant are still incomplete, which could delay the commissioning of the Rooppur power plant. This is yet another instance of a mega plant built without paying attention to the infrastructure needed for the plant to feed the national grid. Bangladesh will have to pay $500 million annually from 2026 onwards as amortisation of the loan against this project. In several areas, many 400/132 kV and 230/132 kV transformers are overloaded, requiring local oil generation to maintain stability and balance on the 132 kV line. If these oil plants, critical for stability, and other power plants receive a full fuel supply, they could meet the country’s energy demands.

In the 2023-24 period, transmission and distribution (T&D) system losses were recorded at 10.06%. However, by addressing the remaining instances of pilferage and upgrading the grid, it is feasible to reduce these losses to single digits. This highlights the connection between misplanning and the increasing financial burden on the economy.

Renewable Energy (RE)

Various plans and agencies state different objectives for renewable energy. 8th five-year plan states the addition of 3700 MW renewable by 2025, Delta Plan 2100 talks about a minimum of adding 30% renewable by 2041, Mujib Climate Prosperity Plan 2022-2041, which is the newest plan, states to achieve 30% renewable energy by 2030 and 40% by 2041. On the other hand, PSMP 2016 and Perspective Plan 2021 did not have any scope of renewable by 2041 although they provided a 10% and 20% alternate renewable scenario. The new Integrated Energy and Power Master Plan (IEPMP) 2023 is cautiously optimistic on both onshore and offshore wind although their projection or plan for 2041 is not very favourable to solar power. As a result, researchers, investors, and policymakers get confused and pick up the numbers they like. Climate and environmental activists also set lofty goals further puzzling the general people.

According to the BPDB and Power Grid Company of Bangladesh (PGCB) engineers, the existing infrastructure of the Power Grid can accommodate 4000 MW RE across different zones of Bangladesh. For smooth operation, especially with the introduction of Nuclear, a lot of spinning and non-spinning reserve (including battery) will be required to maintain stable frequency and voltage. With system upgradation, the Grid can integrate another 6000 MW RE214. It is interesting to note that there is only 600 MW of RE connected to the grid now emphasizing the level of neglect of RE in the last decade by the previous government.

Nuclear Power

In May 2016, a deal was finalised with Russia for $12.65 billion to construct two 1,200 MWe nuclear power plants at Rooppur. Russia is providing $11.385 billion as credit, with the funds offered at an interest rate of LIBOR plus 1.75 per cent, capped at 4%. Bangladesh will have to repay the loan over 28 years with a 10-year grace period. With an initial expense of $550 million, the total cost amounts to $13.2 billion. However, some argue that this is an overpriced deal, making this plant one of the costliest. For example, the 4th and 5th units of the Kudankulam Nuclear Plant in Tamil Nadu, India, built by Rosatom, cost $6.7215 billion for 2,000 MWe. Even when adjusted for capacity, the cost exceeds that of Rooppur by $5.2 billion. The same Russian state-owned nuclear corporation, Rosatom, is also constructing a 4,800 MWe plant in Egypt at an estimated cost of $30 billion. Factors such as the engineering, procurement and construction (EPC) contract, availability of local expert manpower, logistics, geological surveys, and other considerations can significantly impact the cost of a nuclear power plant. Typically, countries with a domestic nuclear industry and trained personnel have a cost advantage. In comparison, India’s unit cost is $3,350/kWe, while the unit cost for Rooppur stands at $5,500/kWe, which appears to be higher. Apart from the high cost, the readiness of our grid to operate a nuclear power plant seems inadequate, especially without an independent National Load Dispatch Center (NLDC) and its automation. It would create major operational challenge and the power plant commissioning would be delayed. In the name of fuel diversification, the choice of nuclear was a misadventure. With the same kind of investment, 6000 to 8000 MW of renewable, gas or coal power plants could be installed.

Gas Shortages and Mismanagement

The gas shortage that started in 2007 with a 300 MMcfd (million cubic feet per day) shortfall could never be alleviated. Today the gas deficit is estimated at 1000-1500 MMcfd. In 2009-10, Petrobangla knew about the looming gas shortage and had a plan to explore new reserves and enhance existing production although it hinted at a 500 MMcfd LNG import in its annual report. By 2010, the first LNG regasification plant proposal was made that was supposed to deliver in 2012. In 2009, Petrobangla and International Oil Company (IOC) combined production was approximately 2000 MMcfd which peaked at about 2650 MMcfd between 2015 and 2019. Since then, the Petrobangla production started declining whereas IOC kept producing 1200-1500 MMcfd gas with a lower gas reserve at their disposal.

At the same time, despite its falling production level, Petrobangla more or less abandoned its plan of exploration and development of domestic gas resources and since 2018, Petrobangla started importing LNG to plug the gas supply deficit gap. Today, along with IOC, Petrobangla supplies about 2000 MMcfd of gas from our reserve and another 500 to 700 MMcfd from imported LNG. The LNG supply has been sporadic either for high price or for technical problems of the Floating Storage and Regasification Units (FSRU). The current demand for natural gas is at least 4,000 MMcfd. Interestingly, of the remaining producible 2P (Proven + Probable) gas reserves totaling 8.66 Tcf (trillion cubic feet), International Oil Companies (IOCs) hold 2.62 Tcf, while the remaining 6.04 Tcf is managed by Petrobangla. Ironically, Petrobangla’s decision to continue importing LNG under the controversial QEEES (Quick Enhancement of Electricity and Energy Supply) Act 2010 has led to LNG being overpriced compared to global prices218, contributing to Bangladesh’s debt issues. The deal signed with the Summit Group involves supplying LNG at prices 15% higher than global long-term rates. Critics argue that utilizing the QEEES Act 2010 to purchase LNG at a premium while natural gas reserves are available with Petrobangla constitutes a misuse of public funds.

If production enhancement from existing reserves is not achieved or new fields are not discovered, indigenous gas supply will decline rapidly in the next five years necessitating higher import of LNG. The economy is heavily dependent on natural gas. Switching to any other fuel will be expensive and time consuming.

Gas Demand Supply Plan

Petrobangla gas demand projection varies between 3000 MMcfd to 6600 MMcfd for 2029-30 under three different scenarios. The most likely demand would be about 5000 MMcfd which meets the entire demand of the power sector. The supply projection is a deficit plan heavily dependent on imported LNG. The gas development fund which was meant for enhancing local gas production was utilised to import LNG preventing any gas exploration effort. The new production enhancement plan provided by BAPEX expects about 300 MMcfd from workover and another possible 810 MMcfd from new discovery. A total of 54 exploration, 15 development and 31 workover wells totaling 100 wells are planned to be drilled by 2028 – a very ambitious program. It must be mentioned that a total of 93 exploratory wells have been drilled in Bangladesh from the beginning of exploration in early fifties. Nine shallow and fifteen deep sea blocks have been put under the 2024 offshore bidding process and seven IOCs have purchased the bid documents.

The locally produced gas and LNG are transmitted throughout the country by Gas Transmission Company Ltd (GTCL). They have a total capacity to handle 4000 MMcfd of gas but now transfers only 2100 MMcfd219. This leaves almost 50% of their capacity unused making it a losing concern.