Rationale of the Exercise and Magnitude of Concern

Over the recent past years, illicit financial outflows have emerged as an alarmingly growing phenomenon in Bangladesh, a malignant tumour that was devouring a significant part of the country’s economy and wealth. Such outflows constituted a complex web of shadow economy that thrived on criminal activities of diverse nature and drew sustenance from an unholy alliance of sections of corrupt politicians, businessmen, financial players, middlemen, government officials, influence peddlers and wheeler-dealers of different types. By taking their ill-gotten resources out of the country, through various illicit channels, these people did enormous harm to the country’s economy and undermined its development potentials. They worked in connivance with and corrupted the country’s executive, legislative, financial, legal, and other institutions, undermined domestic investment and revenue mobilisation efforts, depleted forex reserves, weakened the country’s macroeconomic management, and did serious damage to the cause of good governance in all spheres.

Over the recent past years, illicit financial outflows have emerged as an alarmingly growing phenomenon in Bangladesh, a malignant tumour that was devouring a significant part of the country’s economy and wealth. Such outflows constituted a complex web of shadow economy that thrived on criminal activities of diverse nature and drew sustenance from an unholy alliance of sections of corrupt politicians, businessmen, financial players, middlemen, government officials, influence peddlers and wheeler-dealers of different types. By taking their ill-gotten resources out of the country, through various illicit channels, these people did enormous harm to the country’s economy and undermined its development potentials. They worked in connivance with and corrupted the country’s executive, legislative, financial, legal, and other institutions, undermined domestic investment and revenue mobilisation efforts, depleted forex reserves, weakened the country’s macroeconomic management, and did serious damage to the cause of good governance in all spheres.

In the backdrop of the above, this chapter makes an attempt to understand the magnitude of the laundered money from Bangladesh, identify sources and channels of illicit outflows, propose measures to bring back the stolen wealth, and suggest ways to confront the attendant challenges in going forward.

Origin and Magnitude of the Illicit Outflows

While the exact magnitude of illicit outflows is not easy to capture, for understandable reasons, a review of relevant documents and consultations with concerned stakeholders provide some indication about the magnitude of laundered money, origin of ill-gotten finances, channels of illicit outflows, and the diverse range of assets in which these are then invested overseas.

While the exact magnitude of illicit outflows is not easy to capture, for understandable reasons, a review of relevant documents and consultations with concerned stakeholders provide some indication about the magnitude of laundered money, origin of ill-gotten finances, channels of illicit outflows, and the diverse range of assets in which these are then invested overseas.

Origin and Forms of Illicit Outflows

Illicit financial outflows from Bangladesh originated in various forms- mostly through illegal but sometimes also legal activities. A large part of laundered money was accumulated within the country through a range of illegal and criminal activities e.g. bribe and corruption, financial crimes, trade-mispricing, stealing of bank money and non-repayment of loans, rent seeking,

misuse of political power and influence peddling, over-costing of projects, share market scams, exploitation of migrant workers, tax dodging, drugs and human trafficking, and a host of other means. These sometimes also originate in earnings from legally earned sources (e.g. earnings from business and professional activities carried out in the country; sales proceeds including from the sale of inherited property), which are then taken out of the country through illicit channels. These resources also include those that were supposed to be repatriated to the country but are not (e.g. through export under-invoicing, remittance repatriation through informal channels). These resources can also originate in illegal activities and deals within the country for which payments are made abroad. While previously a large part of the ill-gotten money originating in the country tended to be invested in the domestic economy, forming a sizeable shadow economy, in more recent times, taking the money out of the country and keeping it abroad, in financial and non financial assets, was considered to be a more secure way of guaranteeing a safe haven for the ill-gotten money.

Magnitude of Illicit Flows

Magnitude of Illicit Flows

Attempts have been made by various entities such as Global Financial Integrity Reports (GFIRs), Tax Justice Network and others to come up with an idea about the magnitude of illegal financial outflows, both on global scale, and across countries. For example, successive Global Financial Integrity Reports (GFIRs), based on a range of assumptions, and by deploying various analytical tools, have attempted to estimate the amount of annual illicit financial outflows from various countries including Bangladesh. An attempt has been made here to estimate the amount of illicit financial outflows from Bangladesh between 2009 and 2023, based on GFIR data, and under certain assumptions437. These estimates indicate that the amount of illicit outflows during this period was in the range of about USD 234.0 billion, at an average annual outflow of about USD 16.0 billion (equivalent to about 180 thousand crore taka, on average, annually). This average amount was equivalent to 3.4% of Bangladesh’s current GDP. In other words, this was about one-fifth of forex earnings from export of goods and services and remittance flows to Bangladesh in FY2023-24, and about 11.2% of the national savings. In other words, the amount of illicit outflows, on average, was more than twice the net flows of foreign aid and FDI flows over the corresponding period. This significantly high amount of illicit financial outflows estimated for Bangladesh is not an outlier though. The United Nations Office on Drugs and Crime (UNODC) estimates illicit financial outflows to be equivalent to about 2-5% of annual global GDP (or USD 800 billion-2000 billion). If taxed (at 25%) this would have generated revenues equivalent to about 9.8% of total tax earnings (taking FY 2022-23 as the reference year).

Illicit financial outflows from Bangladesh were found to be destined to, or routed primarily through UAE, UK, Canada, USA, Hong Kong, Malaysia, Singapore, India, as also a number of tax havens. By remaining anonymous, individuals can use the laundered money to buy real estate or funnel the funds through business operations. Global literature survey indicates that an increasing amount of stolen money was being converted to real estate, business enterprises and commercial activities of various kinds. Many corrupt Bangladeshis have taken advantage of this. The indicative amount of illicit financial outflows from Bangladesh is also corroborated by a host of other information: 532 property owners of Bangladeshi origin had real estate worth USD 375.0 million in Dubai (EU Tax Observatory, 2024). 459 Bangladeshis owned a total of 972 residential properties in Dubai worth about USD 315.0 million (Centre for Advanced Defence Studies-C4ADS report, n, d). It has been estimated that USD 47-100 billion worth of money was washed or laundered into Canada (2018) as a haven to conceal harmful and illegal financial activities (End Snow Washing, n, d.). Till March 2024, Malaysian Second Homeowners of Bangladeshi origin numbered more than 3,600440. Estimate of offshore financial wealth held by Bangladeshis was about USD 8.15 billion in 2021 (EU Tax Observatory Report, 2023). Bangladesh currently ranks 52 among 141 in the Financial Secrecy Index441 (Tax Justice Network, 2023).

The deposited amount of Bangladeshis in Swiss banks increased from about BDT 8,988 crore in 2008 to BDT 31,238 crore in 2013. Since 2014, in the backdrop of the Swiss Bank’s policy shift to disclose certain information about deposit holders, this amount has come down in recent years. There was hardly any effort from the Bangladesh side to get more information from the Swiss authorities so that grounds could be created to investigate concerned individuals and entities who have kept money illegally in Swiss banks. The decline indicates that concerned account holders may have shifted their money to other less hazardous destinations or converted it to other assets.

Channels and Process of Illicit Outflows

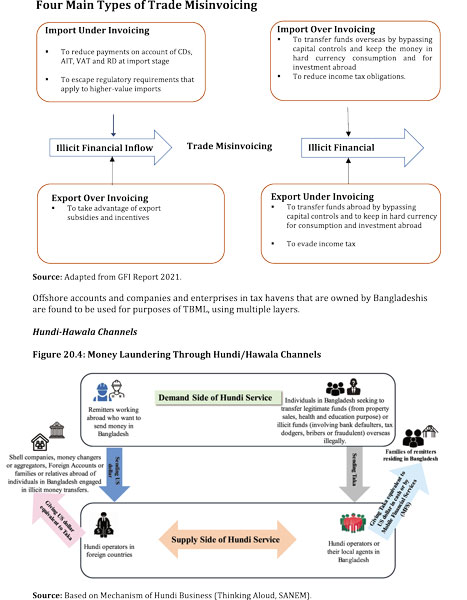

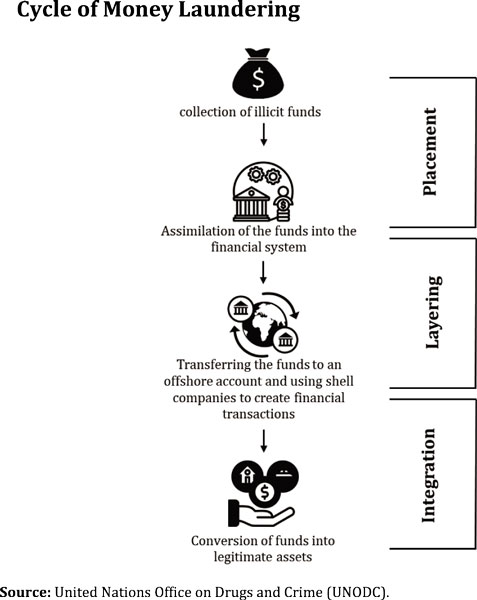

Illegal money originating in Bangladesh appears to have gone through two stages. In the earlier stage, such financial resources constituted a significant part of the domestic economy in the form of a shadow economy. In the later stage, a large part of such resources was transferred overseas through various illicit channels. Bangladesh Financial Intelligence Unit (BFIU), other concerned agencies and KIIs have identified a number of ways in which money is laundered: trade-based money laundering; cash-based money laundering; laundering through the banking, financial and insurance sectors; hundi/hawala channels; courier and carrier; electronic payment; payment through debit and credit cards; bearer instruments; misuse of bank guarantee, correspondent account, and brokerage account; gold smuggling; online betting; via capital market intermediaries. Trade-Based Money Laundering (TBML) remains a key channel for laundering money. This involves the illicit transfer of financial resources by falsifying the declared value of goods on customs invoices. What also transpires from KIIs is that there is a close nexus between import under-invoicing and hundi/hawala operators.

The Hundi/Hawala market is a complex system, developed over the years, with a complex web of players and transactions, both in country and overseas. A simplified version of how this works is presented in Figure 4. Settlement of the illicit outflows with remittances generated overseas is a key mechanism that features prominently in all these transactions, with remitter households in Bangladesh being paid the equivalent amount in BDT (with a premium). Illegal operators and aggregators in host countries collect remittance earnings and transfer money to designated accounts overseas and to accounts of hundi/hawala syndicates in Bangladesh. Some mobile financial services were also found to be involved in this chain. This ends up with an equivalent amount being transferred to beneficiary accounts in Bangladesh.

In recent times, there have been reports of large-scale capital flight through hundi/hawala mechanisms via the medium of offshore financial hubs (Dubai, Panama, Singapore etc.), in offshore accounts or trusts set up by high-net-worth people individuals. Ownership is often multilayered, making detection extremely difficult. Layers of entities are created between laundered money and the ultimate beneficiary to avoid detection. Often destinations with lax banking regulations are used (Panama, Cayman Island, Channel Islands); sometimes citizenship is purchased through investment programmes (St. Lucia, Malta, Vanuatu). Some countries pursue don’t ask don’t tell policies to attract FDI which facilitates the transfer of ill-gotten money to, and investment in, those countries. The overseas subsidiary business houses are now moneyed and mature enough to go for largescale investment in real sectors and setting up industries. Tax advantage makes destinations such as Singapore, Dubai and Hong Kong popular destinations.

Other forms of Money Laundering

Money is also laundered by unregistered foreign workers in Bangladesh, who dodge tax payments and transfer money (often in the form of cash) to host or other countries. Legally earned money such as proceeds from sale of real estate and other assets are also transferred through illicit channels. Double taxation also induces such transfers.

Measures to Address the Problem

Generation of ill-gotten money must be attacked by improving quality of governance, strengthening institutions and instituting a culture of zero tolerance against corruption. Measures will need to be put in place to curb and eliminate identified channels of outflows. Investigative actions and legal measures will need to be undertaken to bring back the stolen wealth. In this backdrop, strengthening and empowerment of concerned institutions, regulatory reforms, legal enforcement, coordination involving concerned agencies, and cross-agency, cross-country cooperation will play a crucially important role. Some concrete measures are proposed below in view of the above.

Address Trade Mispricing

TBML constitutes a significant part of illicit financial outflows from Bangladesh. There is a need to criminalise trade misinvoicing, with high penalties to deter violations and improve coordination among various concerned government agencies. Strengthening the capacity of customs officials, transfer pricing cell (TPC) at the NBR and AML focal points in banks, must be given priority. Access to realtime prices of commodities must be ensured. The use of risk assessment tools must be strengthened by investing in advanced IT and data technologies, such as GF Trade system, to enable customs to identify and flag potentially fraudulent invoices in realtime. Globally, use of AI and blockchain technology in detecting mispricing and fraudulent practices are on the rise; Bangladesh should be prepared to make use of those tools. To forestall over-invoicing in imports, special care should be taken in case of imports of goods on which import duties tend to be either zero or very low, such as capital machineries.

Predominance of manual analysis undermines efficiency of concerned anti-money laundering entities. Bangladesh may consider setting up an independent Trade Transparency Unit to Combat TBML, as is the case in some countries.

Take Measures to Recover Stolen Wealth

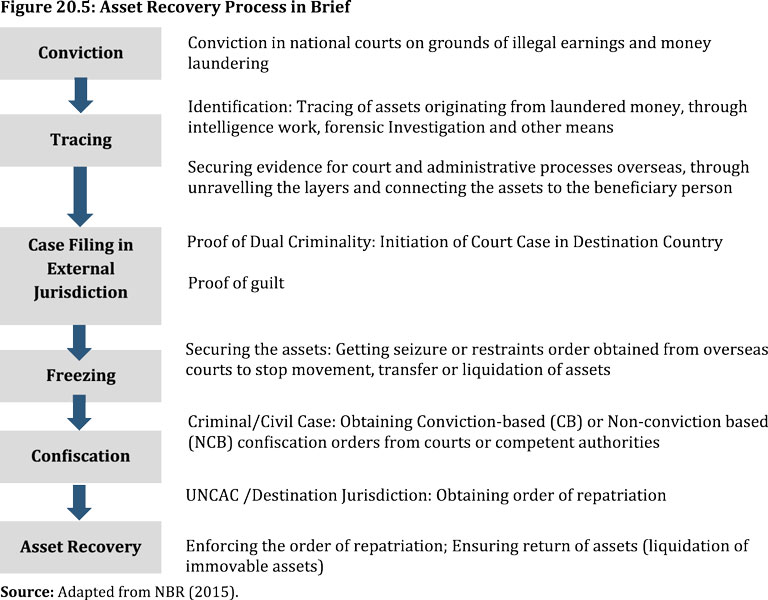

There is a growing demand from all quarters that the Interim Government takes energetic steps to bring back the stolen money. It is not easy to establish the chain of connections involving ill-gotten money, money laundered from the country and the ultimate beneficiary in destination country, which will be needed to ensure return of the stolen assets to Bangladesh. ACC will have to submit charge sheet against the concerned person. It will need to send MLAR to various possible destination countries seeking information456. The cases will need to be successfully presented in Bangladeshi courts. Competent Bangladeshi authorities will have to send formal request letters to destination countries to seize, freeze and sequester wealth of Bangladeshi nationals, as per their relevant laws. For example, Canadian anti-money laundering laws have specific guidelines in such cases (Government of Canada, n, d.). Bangladesh then acquires the legal power to lodge and pursue the cases in destination countries. This will call for hiring of competent lawyers/firms specialising in these matters. Sometimes this is done on recovered money sharing basis.

Tax authorities will also need to be included in the asset recovery process. Stolen asset recovery involves several stages as depicted in Figure 5: (a) forensic audit and establishment of criminal responsibility and amount of liability; (b) criminal accountability through the judicial system and establishment of guilt of money laundering; (c) filing of cases in destination countries for recovery of assets procured through money laundered, directly or through intermediate channels.

Strengthen Concerned Institutional Capacity

Bangladesh has a number of laws and regulations in place to deal with money laundering and return of confiscated property. It has in place the Money Laundering Prevention Act which criminalises laundering of money and authorises confiscations of laundered assets. It has also signed mutual legal assistance treaties with some countries. BFIU has signed MoUs with 81 foreign counterparts and is a member of some anti-money laundering bodies such as Financial Action Task Force (FATF), Asia Pacific Group (APG) and Egmond Group. It can choose to expand this network458. However, no energetic step was taken to make use of those. Even when concerns were raised by involved institutions, actions in many cases depended on signals from high-ups. Political considerations largely influenced work of BFIU, ACC, NBR and other institutions. Intelligence agencies did have a wealth of information about stolen wealth. However, absence of active initiatives and follow-ups was the norm of the day. True, BFIU did take some actions, but mainly against small time operators. In case of none of the widely reported large bank scams, STRs were submitted to the BFIU and no concrete action was taken.

Recovery of stolen assets is also emerging as a global agenda, and it is fast gaining traction in view of the demand for establishing global economic good governance. StAR has helped recover about USD 2.0 billion of stolen assets since its launch in 2007. Philippines, Malaysia, Nigeria and several other developing countries have been able to recover significant amounts of stolen assets, often stowed away in jurisdictions across the world (StAR, n, d.)

Concerned analysts in BFIU/ACC often lack adequate training in strategic analysis in the use of advanced analytical tools. Framework, ACC lacks the authority to arrest suspects or search premises during inquiries, which allows offenders to evade capture and destroy evidence. Customs Risk Management Commissionerate (CRMC) must be strengthened, and Automated Risk Management Systems (ARMs) and other systems must be put in place. Policymakers may think of taking the STR analysis wing outside of the Bangladesh Bank to allow it to function independently, as in India. Bangladesh should not wait for development partners to underwrite such necessary investments.

Put in Place an Independent Prosecution Body

Weak prosecution capacity and succumbing to political pressure have constrained the work of follow-up actions by ACC, BFIU, CID and other institutions. In view of this, an Independent Prosecution body needs to be put in place with proper mandate to undertake follow-up actions.

Deepen Cross-Country Cooperation

A report by the Intergovernmental Group on Financing for Development states that challenges of illicit financial flows have increased in scope and complexity and need to be tackled through close bilateral and international cooperation UN Economic and Social Council, 2024). Bangladesh has acceded to the UN Convention Against Corruption (UNCAC) in 2007. Bangladesh is part of the Stolen Asset Recovery (StAR), a partnership between the WB and UNODC which is geared to take measures to deal with transfer of corrupt funds to safe havens.

As was noted earlier, sometimes, lodging cases in civil courts is a relatively quicker way to get results. Bangladesh should formally apply to join the OECD Convention on Mutual Administrative Assistance in tax matters (commonly known as MAAC) and adopt Common Reporting Standard which is a system of automatic exchange of information.

Law enforcement support (e.g. assistance provided by the Interpol) will need to be sought where needed collaboration deepened467. Destination countries will need to be urged to change national regulations to make repatriation of stolen assets less difficult.

Make Necessary Changes in Existing Regulations

Illicit transfers also take place because of regulations that need to be revisited and revised: money earned through freelancing and BPO activities cannot be legally repatriated to Bangladesh (because of absence of gateways such as PayPal). Double taxation avoidance, transfer of sales of proceeds from sale of inherited property by Bangladeshi citizens living abroad, and visa fees to be sent overseas to employers of migrant workers abroad are some of the areas that call for a closer look. Some existing regulations may need to be reviewed in this connection of migrant workers.

Vigorously Pursue Interim Government’s Ongoing Initiatives

In a welcome move, the Interim Government has set up an Asset Recovery Committee to be led by the governor of Bangladesh Bank to work towards recovering the stolen money. It has also decided to discard the provision that allowed the whitening of black money. It was also decided that the provision of submission of wealth statements by government officials will henceforth be enforced. All these steps are in the right direction.

Unshackled from political pressure, ACC is now taking a number of measures to recover stolen assets from abroad469. The Interim Government is collaborating with the WB, IMF, FBI, Swiss government and UNODC to help identify and recover stolen assets. Bangladesh currently has Customs Cooperation Agreement only with three countries. It needs to have agreements with UAE, India, China, EU, USA, and Singapore to deal with TBML. ACC may also need to seek support from overseas legal experts and firms specialising in stolen asset recovery.

Concluding Remarks

Money laundering from Bangladesh through illicit financial channels had thrived and flourished in an environment of political indulgence and patronage, institutionalised corruption, legal impunity and overall lack of good governance in economic management. Getting rid of this curse will call for an uncompromising political will to address the problem head on. This will entail restoration of accountability and good governance in economic management, enforcement of legal provisions, zero tolerance against corruption and corrupt practices, institutional strengthening, interagency coordination and greater collaboration with destination countries to bring back the stolen wealth to where it belongs, to Bangladesh.

The interim government has inherited a heavily distressed financial sector, especially banks and stock markets, that are fundamentally undercapitalised in the balance sheet of trust. The financial sector used to shine in Bangladesh’s development story. The shine could not be sustained. Loan defaults, frauds, scams and unethical banking practices proliferated with policy reversals and regulatory capture. The safeguards lost guard. Financial repression came back. Cronyism as a business model gained currency.

The interim government has inherited a heavily distressed financial sector, especially banks and stock markets, that are fundamentally undercapitalised in the balance sheet of trust. The financial sector used to shine in Bangladesh’s development story. The shine could not be sustained. Loan defaults, frauds, scams and unethical banking practices proliferated with policy reversals and regulatory capture. The safeguards lost guard. Financial repression came back. Cronyism as a business model gained currency.

This chapter focuses on the banking system. Its macro-criticality can hardly be underestimated. The chapter describes the solvency and liquidity of banks, digging beneath their balance sheet to assess the depth of insolvency, liquidity shortfall and distressed assets. The ailments of the sectors have been diagnosed hard by many stakeholders on a continuing basis. It has produced an unwritten Dhaka Consensus on how the banking system got into and what needs to happen to get out of this deep blackhole.

Macro Criticality of Banking

Macro Criticality of Banking

Scheduled banks in Bangladesh are the core financial intermediaries. Their assets reached Tk 25,462.60 billion at end-June 2024, equivalent to 47 per cent of GDP. Their loans and advances accounted for 66 per cent of total assets. The rest are invested in government securities and cash. Total deposits in the banking sector, excluding inter-bank deposits, amounted to Tk 18,412.38 billion at end June 2024, equivalent to 34 per cent of GDP. A vibrant privately owned set of financial institutions emerged from broad based financial liberalisation in the early 1990s. The restructured and corporatised State-owned Banks (SOB) functioned better for a while until taken for a ride by predators.

Growth model based studies indicate private credit growth became more important over time. The coefficient linking private credit growth to GDP growth nearly doubled from 2001 to 2019. Measures of financial deepening such as broad money to GDP and private credit to GDP surged, supporting the growth of private investment, foreign trade, and GDP per capita. A flexible market based interest rate regime since the early 1990s served Bangladesh well.

Growth model based studies indicate private credit growth became more important over time. The coefficient linking private credit growth to GDP growth nearly doubled from 2001 to 2019. Measures of financial deepening such as broad money to GDP and private credit to GDP surged, supporting the growth of private investment, foreign trade, and GDP per capita. A flexible market based interest rate regime since the early 1990s served Bangladesh well.

Progress faltered prematurely in the past decade. The correlation between the credit impulse, defined as change in the private credit to GDP ratio, and real activity has diminished lately at a time of rising credit intensity of growth, signalling growing resource misallocation. Abrupt and ad hoc changes in the forms of financial repression since the mid-2010s increased regulatory uncertainties. Directed credit expanded coverage from early 2010s followed by generously targeted regulatory easing in the mid-2010s. A 9 per cent lending rate cap at retail level came into effect in April 2020. Moratoriums on loan repayments introduced in response to the pandemic gained a life of their own.

BB switched back to a de jure market determined system in May 2024 after briefly experimenting with a crawling interest rate regime labelled as SMART. Moral suasion by BB subjected retail rates to an invisible 14 per cent ceiling as part of their policy gaming under the IMF program. The IMF pushed for removing SMART. BB complied on paper. The Fund had no way of proving invisible ceilings even though it was public knowledge. The new leadership in BB moved swiftly in July-August to credibly signal change in their regulatory conduct. Retail lending rates are now presumably left to the play of the market based on bank-customer relationships.

BB switched back to a de jure market determined system in May 2024 after briefly experimenting with a crawling interest rate regime labelled as SMART. Moral suasion by BB subjected retail rates to an invisible 14 per cent ceiling as part of their policy gaming under the IMF program. The IMF pushed for removing SMART. BB complied on paper. The Fund had no way of proving invisible ceilings even though it was public knowledge. The new leadership in BB moved swiftly in July-August to credibly signal change in their regulatory conduct. Retail lending rates are now presumably left to the play of the market based on bank-customer relationships.

Retail real lending and policy rates have been negative too long. Retail rates have tended to increase with increase in the policy rate and liquidity stresses in the system. In September, they varied between 11 to 16 per cent depending on banks and sectors. The policy rate has increased cumulatively by 525 basis points since May 2022. It is expected to stay stable at the current 10 per cent until a decisive change in inflation data signals the need for adjustment either way. The real policy rate and the real weighted average lending and deposit rates have remained negative despite increases in the nominal rates. However, rates on government treasury bills moved ahead of inflation over the past 12 months.

Aggregate indicators hide more than they reveal. The advance-to-deposit ratio (ADR) stood at 80.2 per cent at the end of FY24, below the regulatory limit of 87 per cent set for conventional banks. Deposit growth was hit by negative real deposit rates, dented confidence from a series of large-scale fraud allegations and the growth of Non-Performing Loans (NPL). The quality of loans deteriorated to an extent that the banking industry, at the aggregate level, is close to breaching solvency standards. Increased cash holding by the public and government borrowing from commercial banks tightened liquidity deeper than manifest in the formal financial disclosures by the private and state-owned banks.

Aggregate indicators hide more than they reveal. The advance-to-deposit ratio (ADR) stood at 80.2 per cent at the end of FY24, below the regulatory limit of 87 per cent set for conventional banks. Deposit growth was hit by negative real deposit rates, dented confidence from a series of large-scale fraud allegations and the growth of Non-Performing Loans (NPL). The quality of loans deteriorated to an extent that the banking industry, at the aggregate level, is close to breaching solvency standards. Increased cash holding by the public and government borrowing from commercial banks tightened liquidity deeper than manifest in the formal financial disclosures by the private and state-owned banks.

Solvency and Liquidity

Capital too low for comfort. The capital adequacy ratio, at 10.64 per cent in June 2024, is barely above the minimum 10 per cent regulatory requirement, and down from 11.64 per cent in December 2023. State-Owned Banks (SOBs), Specialized Development Banks (SDBs), and several Private Commercial Banks (PCBs) share the neighbourhood of insolvency. The aggregate CRAR was short of meeting the 2.5% extra amount of money banks must keep as a safety net to face adversities (known as capital conservation buffer). Banks are expected to limit dividend and bonus payments when the CCB falls below the prudential limit.

The buffer is less than apparent from data. Underlying the reported increase in CRAR in recent years was the increase in net profit after taxes of the banking sector at a time when the growth and quality of assets deteriorated. The reported net profits were overstated by lax regulatory standards and gaming of the standards. Under provisioning against non-performing loans was 77.3% of the reported profits in 2022. The provisioning shortfall spiked in the previous two years without looking back subsequently.

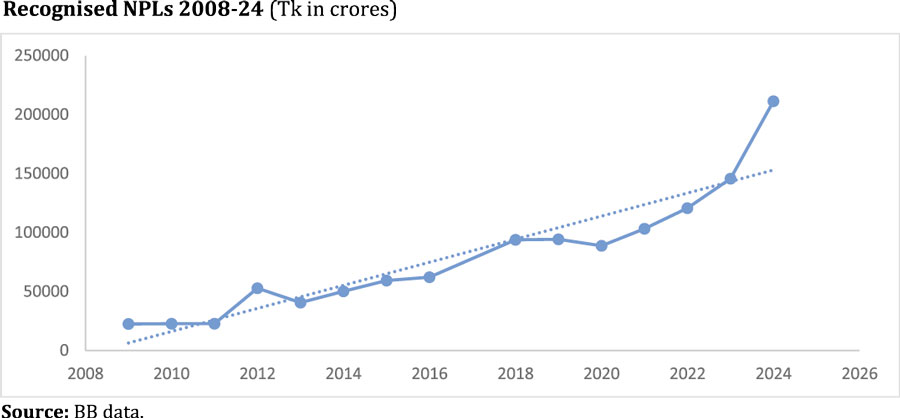

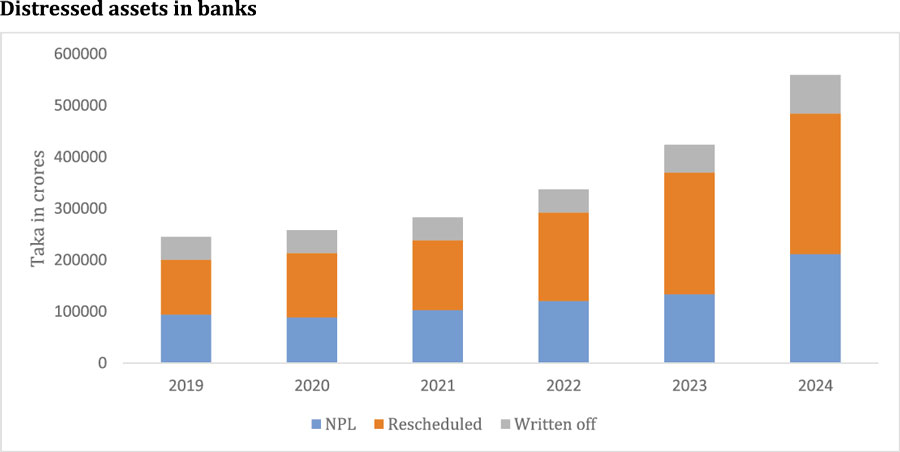

Solvency undermined by loan defaults. Recognised NPLs have increased exponentially in recent years, soaring above 12% in June 2024 from 7.9% in June 2021, reaching a record-high of over Tk 2.11 trillion. These represent the loans recognised under BB’s existing lenient nonperforming loan recognition policy. The NPL is dominated (over 88%) by the worst category called Bad Loans (BL). SOBs are a common denominator in all types of classified loan clusters with a significant share of assets and an even more significant share of NPLs. But they no longer have a monopoly in nontransparent disclosure.

The industry overall on the edge of illiquidity. There is large variation across banks with Islamic PCBs having the severest liquidity shortfall. FCBs are most liquid followed by SOBs and a few conventional PCBs. The industry was able to maintain the minimum required Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) until end-December 2023. Liquidity has been sloping downwards, driven by SOBs and Islamic PCBs since then. Local currency reserve shortfall of the banking system has recently been running consistently between Tk 15,000 to 20,000 crores on a daily basis.

Several private banks are zombies. They vastly window dress their net worth and liquidity. The Annex illustrates the cases of 10 weak private banks. These 10 banks represent 33 per cent of the market share in terms of loans and 32 per cent in terms of deposit. A few corrections for the recoverability and liquidity of their assets turn positive net worth into large negatives for all ten and somewhat comfortable liquidity into illiquidity in eight out of ten. It is ironic that many of these banks use Shariah based banking models that attract a large number of people who prefer Shariah consistent financial ethics. Scams, fraud and misappropriations of funds to related parties in these banks is public knowledge. Their owners profited unethically from the gullible religious sentiments of their depositors.

The Depth of Distress

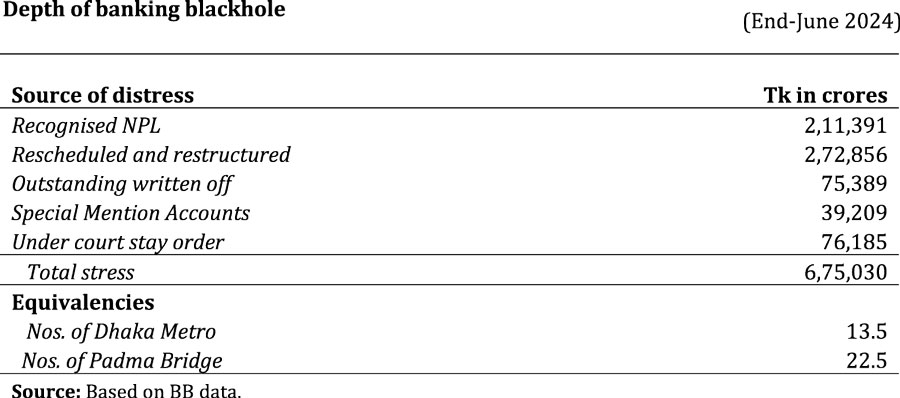

The unseen is over three times the seen. The window dressed part of the NPLs are the loans rescheduled or restructured, because they turned bad in the past, and the amounts written off because they have been on the balance sheet as Bad Loans for too long. 180 All these categories have grown over time. Adding the stock of written off (net of recovered) and the non-classified part of the rescheduled loans to the recognised NPLs, the incidence of “distressed” assets was 31.7% of total bank loans at end-June 2024.

The depth of the banking blackhole exceeded Tk 6,75,000 crores at the end of FY24. This amount is equivalent to 13.5 Dhaka Metro systems and 22.5 Padma bridges. Banks did not get into such a deep hole due to idiosyncratic factors or a few bad apples. The fragmented regulatory system provided multiple avenues for wrongdoing. The banking system is inadequately provisioned to withstand such excruciating stress. Recognised provisioning shortfall amounted to a paltry Tk 19,261 crores at end-June 2024. The size of actual provisioning is puzzling. The BLs, which require 100 per cent provisioning, at end-June 2024 was Tk 1,67,889 crores. The actual provision was Tk 89,355.8 crores, well below even the BLs Generous and allegedly nepotistic provisioning deferral facility to banks of certain genre explain such a gigantic mismatch.

The distress is even larger when the bad loans of the non-bank financial institutions (NBFIs) are accounted for. Bangladesh’s 35 NBFIs had Tk 21,658 crore at end-September 2023, constituting 29.8 per cent of their disbursed loans, with 10 institutions accounting for 67.5 per cent. The incidence of their NPLs was 25 per cent in September 2022. The notorious People’s Leasing and Financial Services and International Leasing and Financial Services faced high profile scams and irregularities. The NBFIs were Tk 2,020 crore short on provisioning. The regulator was largely unmoved, going after a few small fries once in a while.

The Deep Determinant of Stress

The culprits within the banking system are all heavy weights. The big ones coincide with the bad ones. NPL concentration mirrors loans concentration and more. The fastest growing manufacturing sector accounted for 49% of the loans extended and 55% of NPLs. Such disproportionalities are particularly notable in cases of RMG, textiles, ship building and ship breaking. There is a significant overlap between the concentration of loans, the propensity to default, and the bank types (ownership, generation). Capture by dominant business interests disabled the safeguards in the system leading to the dire state it is currently in. Operational and allocational inefficiencies have hurt growth and inclusion by excluding innovations and startups by entrepreneurs without tradable collaterals. The use of forbearance and directives in diverse forms created rents for lawyers, accountants, auditors, and regulatory supervisors.

The same heavyweights demolished confidence In the share market. Market rigging is endemic. Several powerful investors and institutions artificially inflate the share prices through a series of trades violating securities laws.185 The book-building process is manipulated to the extent that it no longer effectively determines the true valuation of a company’s shares. Anomalies in IPO valuations (mostly underpricing) give the sponsors an upper hand over the general investors in the secondary market. Trillions of takas were embezzled from the stock market through fraud, manipulation, placement shares, and deceit in the IPO process. A major manipulation network involving influential entrepreneurs, issue managers, auditors, and a certain class of investors emerged. Stock market intermediaries suffered bankruptcy with negative equity of Tk 13,000 crores. Of this, the merchant bankers accounted for Tk 7,000 crores and the brokerage houses accounted for Tk 6,000 crores. Annex – II provides a more detailed account of the stock market and regulatory failures.

Safeguards don’t guard

Regulatory safeguards subjugated to malpractices. The collusion between BB insiders at the top and influential outsiders was never as open as it was during 2015-2024. The equation between BB and the leadership in the cabinet was recalibrated when fiscal and political dominance found a friendly reception in the leadership of BB. How this coalition of interests tilted the rules of the game is best illustrated by the Bank Company (Amendment) Act 2023 passed on 21 June 2023. The amendment extended tenure of bank sponsor directors to 12 years. Earlier in 2018, the Bank Company Act 2013 was amended, allowing a director to hold bank directorship for nine years in 2018. For optical reasons perhaps, the number of members of the same family in a private bank’s board was reduced from 4 to 3, still higher than the 2 allowed under the 1991 act until amended to 4 in 2018. The 2023 amendments undermined the Bangladesh Corporate Governance Code requiring listed banks, non-banks, insurance companies and statutory bodies to have no less than five and no more than 20 directors at a time, of which at least one in five must be independent or non-executive directors. The 2023 amendment enabled having as few as 2 independent directors.

The amendments introduced the distinction between willful and unwilful defaulters with the former ambiguously defined as those who “do not repay though they have the capacity to do so”, leaving the clarification open to judicial interference. It exempted the sister concerns of defaulting companies from ineligibility to get new loans subject to BB discretion. The penalties for willful included travel restrictions, denial of trade license or new company registration in capital markets, and few other slaps in the wrist. Board members or their relatives were allowed to borrow with collateral or bond or security. These together constituted a giant leap of the banking system from rule of law to law of the rulers.

Enforcement was unevenly lax. Insufficient number of independent directors in overpopulated boards served the purposes of complying and rubber stamping the will of the sponsors. Weighing of relevant skills and experience is not evident from the actual composition of boards in several banks, both state and private. Internal and external auditors do not necessarily get chosen for their technical skills and impact. Biased enforcement by the BB enabled serious misconduct both in domestic and state-owned banks. It failed to monitor on an ongoing and forward looking basis the changing risk profile. The level of concern and stringency of supervisory constraint appear unrelated to movements in capital ratios. BB does not have full discretion in supervisory actions against SOBs noncompliant with prudential requirements for years without sanctions. The Ministry of Finance holds a broad regulatory mandate for the SOBs.

Licensing was transactional. Predators surmounted licensing bars all too easily. The current system does not require establishing a proper corporate governance framework, determining the suitability of major shareholders in the context of “fit and proper” criteria and disclosure of the ultimate beneficial owner.189 The licensing of the PCBs largely became a tool for political patronage. Ownership predominantly went to individuals with incumbent political identities despite questions based on an economic rationale from outsider stakeholders. The Finance Ministry’s politically motivated overreach in licensing private banks was yet another manifestation of policy and regulatory capture.

Capture by dominant groups

Big players siphoned big money. Embezzlement of big chunks of money from different banks by a number of groups through fake companies or without proper documentation became a privilege of large borrowers. CPD documented 24 cases of malfeasance involving forgery, embezzlement, fraud, theft, money laundering, misappropriations and irregularities from compilations of published reports during 2008-23. The perpetrators include the Hallmark Group, Bismillah Group, AnnonTex, Regent Hospital, NRB Global Bank and so on, all big players. All the 24 cases together added up to Tk 922.6 billion or Tk 3.86 billion or $32 million per case. Average per capita income in Bangladesh is about $2600. If the average person earns this income for 50 years with an annual growth of 10 per cent, she makes $0.31 million in her lifetime. The stolen amount per case is nearly 105 times this estimate of the lifetime income of the average Bangladeshi.

Related parties capitalised relations. Related-party lending, a correlate of regulatory capture, is widespread among banks controlled by individuals or entities with a substantial interest in nonfinancial firms. Restrictions on related-party transactions do not bite. Directors can borrow from banks other than the one for which they are directors. Not surprisingly, related party lending soared. For instance, reciprocal loans of directors of eight banks amounted to Tk 45,000 crore at the end of 2023. These banks bent rules and norms under the regulator’s watch. The contribution of the eight bank directors to lending banks’ paid-up capital was a paltry 5 per cent of the loans they took from each other.195 The definitions of “controlling interest” and “ultimate beneficial ownership” as well as “related parties” exclude complex interfamilial relationships that mask the real size of related-party lending. Regulatory enforcement on related-party lending was blind to breaches.

Technocratic explanations have no clothes. Explanations centering on organisational capacity deficits and the deviations from international best practices merely scratch the symptoms. A story centering around the symbiosis of interests of bank owners, regulators, politicians and bureaucrats holds better promise. Patronage through regulatory and policy capture caused collapse in regulatory and corporate governance aided and abetted by influential members in government and association of bank owners. A single conglomerate gained control over seven private commercial banks in 2017. Imprudent credit underwriting practices led to a rapid increase in NPLs of several third-generation conventional PCBs. Their owners and boards survived with impunity. Prominent politically exposed persons and owners of large business groups were on the boards of many banks, with independent directors who did not function as intended. Business tycoons maintained unbridled lobbying power with powerful politicians and bureaucrats to ensure policy inaction against irregular and corrupt practices.

A Dhaka Consensus

There is hardly any controversy on the predicaments of the financial system. The interim government has inherited a Dhaka Consensus on the plight of the financial system in general, banking in particular.

The system is undercapitalised, illiquid and malfeasant. The extent of undercapitalisation and illiquidity is anybody’s guess anchored on hugely exaggerated capital adequacy and liquidity. Distressed assets in the banking system multiplied in the past decade and half in both state and private domains encompassing conventional and most shariah banks. The rest of the financial system such as non-bank financial institutions and insurance are similarly on the precipice of bankruptcy. The share markets have turned into a den of financial foul play. Company fundamentals are irrelevant to market valuations in ways very different from the bull and bear runs observed in developed stock markets.

It’s not the economy, stupid. Bangladesh’s financial sector distress did not emerge from economic disruptions or financial crises or even political instability. Economic factors such as trade, remittances, investments, inflation, commodity prices, exchange rates, and interest rates cannot explain the sustained drain in balance sheets and trust in market makers and regulators. An organised network of business conglomerates, bureaucrats and politicians coalesced explicitly and implicitly to use the financial system to mine public money by capturing corporate and regulatory governance. Laws and regulations were tailored and retrofitted to serve the interests of this troika in the spot and forward markets for local and foreign currencies. De jure accountability systems were de facto deposited in deep fridge. The web of institutions to adjudicate disputes, regulate markets, and allocate resources largely exhausted the trust of the public.

A few islands of sound banking and bailout expectations prevented runs. The troika needed financial business growth to sustain depositor and investor faith in the system, so their Ponzi game remains viable. They had to give space to professionals to do business playing by the rules. The professionals were able to survive on their own merit deftly navigating many adversities. These islands of excellence in conventional banking, micro finance and mobile financial services combined with a shared belief that no incumbent leadership in government will take the existential risk of allowing the system to fail. This kept depositor angst below run inducing thresholds. The disease may not yet be terminal, but it is painfully disabling. Financial stability and the capacity of the financial sector in general, banking especially, to support inclusive and sustainable growth are in jeopardy.

An opportunity to contest oligarchic power in banking. Views on how to reset the system to mitigate risks and deliver services in keeping with changing times do not obviously converge. Differences in understanding the fine details on the ground and how best to manage the political economy of change account for differences in views on how to change. However, there is general recognition of the opportunity opened by recent political changes to credibly contest the oligarchy in banking. Oligarchic powers who made SOBs and several PCBs a nagging threat to financial stability are currently on backfoot. But they are yet to be bowled out. The reforms that should have happened yesterday, so to say, must make sure new oligarchs do not entrench themselves and replay the game of their predecessors.

Mitigating systemic risk is currently the overarching priority. The recent shock therapies need well considered follow up to produce durable results by changing the game. The prior actions under the IMF programme and the World Bank’s budget supports are putting in place a few reforms that correct the deviations from international norms and standards. By themselves, these won’t change the culture of impunity. BB has taken some necessary measures to reconstitute bank board’s following the flight of their owners and directors from the seats of power. The path going forward is long and arduous. It will test the power of political will to steadfastly transform the state of play in the banking system from foul to fair.

How bad are the balance sheets?

A banking system can only be protected by its capital and liquidity in a distressed situation. We chose 10 distressed banks to dig into their solvency and liquidity. Of the 10 banks, 2 are state owned banks that were mostly hit by scams in the last decade. The other 8 are extremely weak shariya based banks and conventional private commercial banks. The names of these banks are not disclosed for confidentiality. All the 10 banks are termed ‘distressed’ by the regulators, media and public. Combined loans and deposits of these 10 banks constitute 33% of the total loans and 32% of the total deposit of the banking sector. In fact, some of these banks are domestically systemically important bank (D-SIB) in Bangladesh.

Most of these banks did not disclose the fair value of their assets in their financial reporting. We had to identify the hidden toxic assets based on expert judgement backed by information gleaned from indirect disclosures in the bank’s annual report, regulators and various news published in the media in the last couple of years (the specific references are listed at the end).

The assessment covers their audited balance sheets at end-December 2023 digging into each and every asset: Cash & Balance with BB, Balance with Other Banks, Money Market Placement, Investment, Loan & Advances, Fixed & Other Assets etc. When the approximate valuation of these was completed, we adjusted the reported value of assets less for those that differ derive at the adjusted capital of the bank as the difference between the adjusted values of assets and liabilities. Similarly, we assessed the quality of liquid assets of each bank to derive the adjusted liquid assets to total assets ratio of the bank. This ratio indicates the amount of intrinsic liquid resources these banks have to meet their depositors’ demand.

Beneath the balance sheets

Analysis of each bank’s balance held with other banks considered the credit profile of the counterparty (other banks and financial institutions) to determine the magnitude of needed adjustment. The adjusted total assets is 37 per cent of the reported value. One large bank, for instance, had balance with other banks and FIs worth Tk 6,652 crore as of December 31, 2023. Detail breakdown of their balance held with the counterparty revealed around Tk 2,000 crore cannot be recovered. It also had Tk 584 crore with Non-Bank Financial Institutions, 80% of which are not recoverable. Similarly, another big bank has Tk 10,158 crore of which, as various media reported, around Tk 8,000 crore is stuck with 5 distressed banks.

The story is fundamentally not very different in cases of other financial placements such as Money at Call and investment in government securities. Several banks placed large amounts with another bank who placed the money with a related party from whom money is not recoverable. Investment in Government Securities, Shares (quoted and unquoted) and Bonds of these 10 banks are adjusted by only 10 per cent. Government securities could not be valued on a mark-to-market basis. There is no publicly available data on the amount, tenor and yield of each investment. Unquoted shares were adjusted considering the credit profile of the investee, particularly their holdings in sub bonds (mostly invested in distressed banks).

Actual valuation of loan portfolio requires on site in depth due diligence reviewing each credit file, loan statement and loan documentation. Getting to this ideal is limited by data. Data mirroring the portfolio quality is indicative. For instance, a bank reporting 5% NPL should not have negative balance with Bangladesh Bank. Considering available information on such correlates suggest reducing their combined Loans and Advances by 64 per cent.

All the 10 banks are technically bankrupt and illiquid. Their combined adjusted value of the assets is 52 per cent of the reported value. As a result, net worth is negative. Liquidity measured by the ratio of liquid assets to total tangible assets indicates 8 out of ten are illiquid.

All banks are rated Very Weak. Fundamentally, a bank’s financial profile depends on Profitability, NPL and Capital as part of solvency and funding structure and liquid assets to meet depositors’ demands. Solvency and liquidity are interrelated. Each of the 10 banks are rated in 3 classes: Assets, Capital and Liquidity after all the adjustments on the following ordinal scale: VS=Very Strong; S=Strong; M=Moderate; W=Weak; VW=Very Weak, + a notch up, - a notch down.

All get VW-, the worst rating. They are all extremely weak in assets and capital. Two banks have moderate liquid assets. The remaining 8 are nearly illiquid. Most of these banks have apparently defaulted in their obligations. They have been denied support from the market and their support from the central bank is exhausted. Currently they are taking cover under the BB’s Guarantee Scheme to stay afloat.

The precarities of these banks are public knowledge. The public know their reported finance and the stories day in day out on how much and how these banks invested in delinquent non-financial corporates, insolvent financial corporates, and a significant amount into entities that don’t exist. Hence, the story of the massive difference between reality and the reported financials is no surprise.

amounted to a paltry Tk 19,261 crores at end-June 2024. The size of actual provisioning is puzzling. The BLs, which require 100 per cent provisioning, at end-June 2024 was Tk 1,67,889 crores. The actual provision was Tk 89,355.8 crores, well below even the BLs Generous and allegedly nepotistic provisioning deferral facility to banks of certain genre explain such a gigantic mismatch.

The distress is even larger when the bad loans of the non-bank financial institutions (NBFIs) are accounted for. Bangladesh’s 35 NBFIs had Tk 21,658 crore at end-September 2023, constituting 29.8 per cent of their disbursed loans, with 10 institutions accounting for 67.5 per cent. The incidence of their NPLs was 25 per cent in September 2022. The notorious People’s Leasing and Financial Services and International Leasing and Financial Services faced high profile scams and irregularities. The NBFIs were Tk 2,020 crore short on provisioning. The regulator was largely unmoved, going after a few small fries once in a while.

The Deep Determinant of Stress

The culprits within the banking system are all heavy weights. The big ones coincide with the bad ones. NPL concentration mirrors loans concentration and more. The fastest growing manufacturing sector accounted for 49% of the loans extended and 55% of NPLs. Such disproportionalities are particularly notable in cases of RMG, textiles, ship building and ship breaking. There is a significant overlap between the concentration of loans, the propensity to default, and the bank types (ownership, generation). Capture by dominant business interests disabled the safeguards in the system leading to the dire state it is currently in. Operational and allocational inefficiencies have hurt growth and inclusion by excluding innovations and startups by entrepreneurs without tradable collaterals. The use of forbearance and directives in diverse forms created rents for lawyers, accountants, auditors, and regulatory supervisors.

The same heavyweights demolished confidence In the share market. Market rigging is endemic. Several powerful investors and institutions artificially inflate the share prices through a series of trades violating securities laws.185 The book-building process is manipulated to the extent that it no longer effectively determines the true valuation of a company’s shares. Anomalies in IPO valuations (mostly underpricing) give the sponsors an upper hand over the general investors in the secondary market. Trillions of takas were embezzled from the stock market through fraud, manipulation, placement shares, and deceit in the IPO process. A major manipulation network involving influential entrepreneurs, issue managers, auditors, and a certain class of investors emerged. Stock market intermediaries suffered bankruptcy with negative equity of Tk 13,000 crores. Of this, the merchant bankers accounted for Tk 7,000 crores and the brokerage houses accounted for Tk 6,000 crores. Annex – II provides a more detailed account of the stock market and regulatory failures.

Safeguards don’t guard

Regulatory safeguards subjugated to malpractices. The collusion between BB insiders at the top and influential outsiders was never as open as it was during 2015-2024. The equation between BB and the leadership in the cabinet was recalibrated when fiscal and political dominance found a friendly reception in the leadership of BB. How this coalition of interests tilted the rules of the game is best illustrated by the Bank Company (Amendment) Act 2023 passed on 21 June 2023. The amendment extended tenure of bank sponsor directors to 12 years. Earlier in 2018, the Bank Company Act 2013 was amended, allowing a director to hold bank directorship for nine years in 2018. For optical reasons perhaps, the number of members of the same family in a private bank’s board was reduced from 4 to 3, still higher than the 2 allowed under the 1991 act until amended to 4 in 2018. The 2023 amendments undermined the Bangladesh Corporate Governance Code requiring listed banks, non-banks, insurance companies and statutory bodies to have no less than five and no more than 20 directors at a time, of which at least one in five must be independent or non-executive directors. The 2023 amendment enabled having as few as 2 independent directors.

The amendments introduced the distinction between willful and unwilful defaulters with the former ambiguously defined as those who “do not repay though they have the capacity to do so”, leaving the clarification open to judicial interference. It exempted the sister concerns of defaulting companies from ineligibility to get new loans subject to BB discretion. The penalties for willful included travel restrictions, denial of trade license or new company registration in capital markets, and few other slaps in the wrist. Board members or their relatives were allowed to borrow with collateral or bond or security. These together constituted a giant leap of the banking system from rule of law to law of the rulers.

Enforcement was unevenly lax. Insufficient number of independent directors in overpopulated boards served the purposes of complying and rubber stamping the will of the sponsors. Weighing of relevant skills and experience is not evident from the actual composition of boards in several banks, both state and private. Internal and external auditors do not necessarily get chosen for their technical skills and impact. Biased enforcement by the BB enabled serious misconduct both in domestic and state-owned banks. It failed to monitor on an ongoing and forward looking basis the changing risk profile. The level of concern and stringency of supervisory constraint appear unrelated to movements in capital ratios. BB does not have full discretion in supervisory actions against SOBs noncompliant with prudential requirements for years without sanctions. The Ministry of Finance holds a broad regulatory mandate for the SOBs.

Licensing was transactional. Predators surmounted licensing bars all too easily. The current system does not require establishing a proper corporate governance framework, determining the suitability of major shareholders in the context of “fit and proper” criteria and disclosure of the ultimate beneficial owner.189 The licensing of the PCBs largely became a tool for political patronage. Ownership predominantly went to individuals with incumbent political identities despite questions based on an economic rationale from outsider stakeholders. The Finance Ministry’s politically motivated overreach in licensing private banks was yet another manifestation of policy and regulatory capture.

Capture by dominant groups

Big players siphoned big money. Embezzlement of big chunks of money from different banks by a number of groups through fake companies or without proper documentation became a privilege of large borrowers. CPD documented 24 cases of malfeasance involving forgery, embezzlement, fraud, theft, money laundering, misappropriations and irregularities from compilations of published reports during 2008-23. The perpetrators include the Hallmark Group, Bismillah Group, AnnonTex, Regent Hospital, NRB Global Bank and so on, all big players. All the 24 cases together added up to Tk 922.6 billion or Tk 3.86 billion or $32 million per case. Average per capita income in Bangladesh is about $2600. If the average person earns this income for 50 years with an annual growth of 10 per cent, she makes $0.31 million in her lifetime. The stolen amount per case is nearly 105 times this estimate of the lifetime income of the average Bangladeshi.

Related parties capitalised relations. Related-party lending, a correlate of regulatory capture, is widespread among banks controlled by individuals or entities with a substantial interest in nonfinancial firms. Restrictions on related-party transactions do not bite. Directors can borrow from banks other than the one for which they are directors. Not surprisingly, related party lending soared. For instance, reciprocal loans of directors of eight banks amounted to Tk 45,000 crore at the end of 2023. These banks bent rules and norms under the regulator’s watch. The contribution of the eight bank directors to lending banks’ paid-up capital was a paltry 5 per cent of the loans they took from each other.195 The definitions of “controlling interest” and “ultimate beneficial ownership” as well as “related parties” exclude complex interfamilial relationships that mask the real size of related-party lending. Regulatory enforcement on related-party lending was blind to breaches.

Technocratic explanations have no clothes. Explanations centering on organisational capacity deficits and the deviations from international best practices merely scratch the symptoms. A story centering around the symbiosis of interests of bank owners, regulators, politicians and bureaucrats holds better promise. Patronage through regulatory and policy capture caused collapse in regulatory and corporate governance aided and abetted by influential members in government and association of bank owners. A single conglomerate gained control over seven private commercial banks in 2017. Imprudent credit underwriting practices led to a rapid increase in NPLs of several third-generation conventional PCBs. Their owners and boards survived with impunity. Prominent politically exposed persons and owners of large business groups were on the boards of many banks, with independent directors who did not function as intended. Business tycoons maintained unbridled lobbying power with powerful politicians and bureaucrats to ensure policy inaction against irregular and corrupt practices.

A Dhaka Consensus

There is hardly any controversy on the predicaments of the financial system. The interim government has inherited a Dhaka Consensus on the plight of the financial system in general, banking in particular.

The system is undercapitalised, illiquid and malfeasant. The extent of undercapitalisation and illiquidity is anybody’s guess anchored on hugely exaggerated capital adequacy and liquidity. Distressed assets in the banking system multiplied in the past decade and half in both state and private domains encompassing conventional and most shariah banks. The rest of the financial system such as non-bank financial institutions and insurance are similarly on the precipice of bankruptcy. The share markets have turned into a den of financial foul play. Company fundamentals are irrelevant to market valuations in ways very different from the bull and bear runs observed in developed stock markets.

It’s not the economy, stupid. Bangladesh’s financial sector distress did not emerge from economic disruptions or financial crises or even political instability. Economic factors such as trade, remittances, investments, inflation, commodity prices, exchange rates, and interest rates cannot explain the sustained drain in balance sheets and trust in market makers and regulators. An organised network of business conglomerates, bureaucrats and politicians coalesced explicitly and implicitly to use the financial system to mine public money by capturing corporate and regulatory governance. Laws and regulations were tailored and retrofitted to serve the interests of this troika in the spot and forward markets for local and foreign currencies. De jure accountability systems were de facto deposited in deep fridge. The web of institutions to adjudicate disputes, regulate markets, and allocate resources largely exhausted the trust of the public.

A few islands of sound banking and bailout expectations prevented runs. The troika needed financial business growth to sustain depositor and investor faith in the system, so their Ponzi game remains viable. They had to give space to professionals to do business playing by the rules. The professionals were able to survive on their own merit deftly navigating many adversities. These islands of excellence in conventional banking, micro finance and mobile financial services combined with a shared belief that no incumbent leadership in government will take the existential risk of allowing the system to fail. This kept depositor angst below run inducing thresholds. The disease may not yet be terminal, but it is painfully disabling. Financial stability and the capacity of the financial sector in general, banking especially, to support inclusive and sustainable growth are in jeopardy.

An opportunity to contest oligarchic power in banking. Views on how to reset the system to mitigate risks and deliver services in keeping with changing times do not obviously converge. Differences in understanding the fine details on the ground and how best to manage the political economy of change account for differences in views on how to change. However, there is general recognition of the opportunity opened by recent political changes to credibly contest the oligarchy in banking. Oligarchic powers who made SOBs and several PCBs a nagging threat to financial stability are currently on backfoot. But they are yet to be bowled out. The reforms that should have happened yesterday, so to say, must make sure new oligarchs do not entrench themselves and replay the game of their predecessors.

Mitigating systemic risk is currently the overarching priority. The recent shock therapies need well considered follow up to produce durable results by changing the game. The prior actions under the IMF programme and the World Bank’s budget supports are putting in place a few reforms that correct the deviations from international norms and standards. By themselves, these won’t change the culture of impunity. BB has taken some necessary measures to reconstitute bank board’s following the flight of their owners and directors from the seats of power. The path going forward is long and arduous. It will test the power of political will to steadfastly transform the state of play in the banking system from foul to fair.

How bad are the balance sheets?

A banking system can only be protected by its capital and liquidity in a distressed situation. We chose 10 distressed banks to dig into their solvency and liquidity. Of the 10 banks, 2 are state owned banks that were mostly hit by scams in the last decade. The other 8 are extremely weak shariya based banks and conventional private commercial banks. The names of these banks are not disclosed for confidentiality. All the 10 banks are termed ‘distressed’ by the regulators, media and public. Combined loans and deposits of these 10 banks constitute 33% of the total loans and 32% of the total deposit of the banking sector. In fact, some of these banks are domestically systemically important bank (D-SIB) in Bangladesh.

Most of these banks did not disclose the fair value of their assets in their financial reporting. We had to identify the hidden toxic assets based on expert judgement backed by information gleaned from indirect disclosures in the bank’s annual report, regulators and various news published in the media in the last couple of years (the specific references are listed at the end).

The assessment covers their audited balance sheets at end-December 2023 digging into each and every asset: Cash & Balance with BB, Balance with Other Banks, Money Market Placement, Investment, Loan & Advances, Fixed & Other Assets etc. When the approximate valuation of these was completed, we adjusted the reported value of assets less for those that differ derive at the adjusted capital of the bank as the difference between the adjusted values of assets and liabilities. Similarly, we assessed the quality of liquid assets of each bank to derive the adjusted liquid assets to total assets ratio of the bank. This ratio indicates the amount of intrinsic liquid resources these banks have to meet their depositors’ demand.

Beneath the balance sheets

Analysis of each bank’s balance held with other banks considered the credit profile of the counterparty (other banks and financial institutions) to determine the magnitude of needed adjustment. The adjusted total assets is 37 per cent of the reported value. One large bank, for instance, had balance with other banks and FIs worth Tk 6,652 crore as of December 31, 2023. Detail breakdown of their balance held with the counterparty revealed around Tk 2,000 crore cannot be recovered. It also had Tk 584 crore with Non-Bank Financial Institutions, 80% of which are not recoverable. Similarly, another big bank has Tk 10,158 crore of which, as various media reported, around Tk 8,000 crore is stuck with 5 distressed banks.

The story is fundamentally not very different in cases of other financial placements such as Money at Call and investment in government securities. Several banks placed large amounts with another bank who placed the money with a related party from whom money is not recoverable. Investment in Government Securities, Shares (quoted and unquoted) and Bonds of these 10 banks are adjusted by only 10 per cent. Government securities could not be valued on a mark-to-market basis. There is no publicly available data on the amount, tenor and yield of each investment. Unquoted shares were adjusted considering the credit profile of the investee, particularly their holdings in sub bonds (mostly invested in distressed banks).

Actual valuation of loan portfolio requires on site in depth due diligence reviewing each credit file, loan statement and loan documentation. Getting to this ideal is limited by data. Data mirroring the portfolio quality is indicative. For instance, a bank reporting 5% NPL should not have negative balance with Bangladesh Bank. Considering available information on such correlates suggest reducing their combined Loans and Advances by 64 per cent.

All the 10 banks are technically bankrupt and illiquid. Their combined adjusted value of the assets is 52 per cent of the reported value. As a result, net worth is negative. Liquidity measured by the ratio of liquid assets to total tangible assets indicates 8 out of ten are illiquid.

All banks are rated Very Weak. Fundamentally, a bank’s financial profile depends on Profitability, NPL and Capital as part of solvency and funding structure and liquid assets to meet depositors’ demands. Solvency and liquidity are interrelated. Each of the 10 banks are rated in 3 classes: Assets, Capital and Liquidity after all the adjustments on the following ordinal scale: VS=Very Strong; S=Strong; M=Moderate; W=Weak; VW=Very Weak, + a notch up, - a notch down.

All get VW-, the worst rating. They are all extremely weak in assets and capital. Two banks have moderate liquid assets. The remaining 8 are nearly illiquid. Most of these banks have apparently defaulted in their obligations. They have been denied support from the market and their support from the central bank is exhausted. Currently they are taking cover under the BB’s Guarantee Scheme to stay afloat.

The precarities of these banks are public knowledge. The public know their reported finance and the stories day in day out on how much and how these banks invested in delinquent non-financial corporates, insolvent financial corporates, and a significant amount into entities that don’t exist. Hence, the story of the massive difference between reality and the reported financials is no surprise.

© 2026 - All Rights with The Financial Express