Most listed banks posted higher profits year-on-year in the first quarter this year, buoyed by higher gains from investments in government securities.

While interest income grew during the period, interest payments to depositors and lenders also jumped due to higher deposit rates, squeezing net interest income. In such a situation, higher gains from T-bonds and T-bills offset the decline in net interest income and boosted lenders' profits.

As of Wednesday, some 23 banks had published financial data for January-March (the first quarter) this year, out of 36 listed banks (five banks are under a merger process).

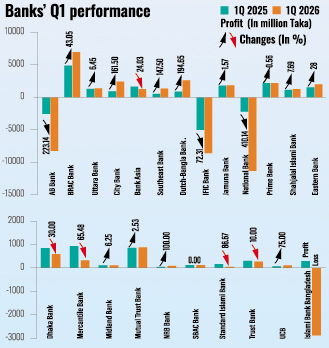

Of them, 12 reported year-on-year profit growth, five saw their profits decline, three endured an increase in losses and the results of another remained almost flat, while Islami Bank entered the red again in the March quarter, according to the unaudited financial statements of the lenders.

The top performers include BRAC Bank, City Bank, Dutch-Bangla Bank, Uttara Bank, Jamuna Bank, Midland Bank, Mutual Trust Bank, NRB Bank, Shahjalal Islami Bank, Southeast Bank and United Commercial Bank. They posted growth ranging from 6.5 per cent to 194 per cent.

Among them, BRAC Bank posted the highest profit of Tk 6.96 billion, followed by Dutch-Bangla Bank with Tk 2.61 billion, City Bank with Tk 2.41 billion, Prime Bank with Tk 2.08 billion, Eastern Bank with Tk 1.99 billion and Southeast Bank with Tk 1.32 billion in the January-March quarter this year.

BRAC Bank's consolidated profit jumped 44 per cent year-on-year in January-March this year, buoyed by substantial earnings from investments and contributions from subsidiaries.

The leading bank's net interest income grew 21 per cent year-on-year to Tk 4.98 billion while investment income jumped 36 per cent, leading to impressive profit growth.

Dutch-Bangla Bank's profit climbed a whopping 195 per cent despite a 3 per cent year-on-year growth in net interest income. Its investment income grew 41 per cent, helping it achieve higher profits year-on-year.

City Bank's net profit more than doubled year-on-year to Tk 2.41 billion in the March quarter, driven by growth across core income streams.

"While I am happy with such a strong increase in profit, I am equally concerned about the sharp slowdown in credit growth in the first quarter," said City Bank Managing Director and Chief Executive Officer Mashrur Arefin in a statement.

"The direction in which credit growth in our sector is heading is, quite frankly, a matter of great concern," he said.

Improved asset quality helped optimise provisioning levels, further supporting City Bank's bottom line.

City Bank's income from loans rose 14 per cent year-on-year to Tk 1.30 billion, while investment income grew more sharply, climbing from Tk 6.03 billion to Tk 10.14 billion and accounting for 32 per cent of total operating income.

Eastern Bank reported a 28 per cent year-on-year growth in earnings in the March quarter, supported by strong investment income, higher foreign exchange earnings and lower provisioning.

"We continue to remain focused on maintaining strong asset quality, liquidity and capital strength while ensuring superior financial results for our shareholders," said Hassan O. Rashid, managing director of EBL, in a statement.

With private-sector credit demand slowing, EBL channelled a larger share of its funds into government securities rather than loans. It maintained strong asset quality, with its non-performing loan (NPL) ratio standing at 2.8 per cent on a standalone basis as of March this year, almost unchanged from 2.79 per cent a year ago and significantly below the industry average.

Akramul Alam, head of research at Royal Capital, said the well-performing banks have always been able to keep operating costs down and mobilise funds at relatively low costs, riding on their excellent market reputation.

The trusted banks also witnessed deposit migration as clients of weak banks transferred their funds to well-governed banks, he said.

As private-sector credit demand remained weak amid persistent economic uncertainties, banks with high liquidity preferred to invest their excess funds in risk-free government securities and reaped handsome returns.

"Banks with low bad loans could invest more in Treasury bonds. These returns were risk-free and fully secured, requiring no provisions, which supported their profit growth," Mr Alam added.

During the same period, some banks suffered due to poor asset quality and substantial bad loans, forcing them to set aside huge amounts of provisions.

The bad loans that the banks had tucked away by taking advantage of the political clout of the Awami League-led regime have come to light since the 2024 political changeover.

"If a bank has a high volume of bad loans, it cannot earn interest income from them. Moreover, it has to keep provisions against the loans from profits, hitting the bottom line," Alam explained.

For example, National Bank's financial woes deepened as the bank's losses increased by a massive 410 per cent year-on-year to Tk 11.33 billion in the first quarter ended March this year.

AB Bank's losses escalated 223 per cent year-on-year to Tk 8.25 billion while IFIC Bank's losses soared 72 per cent year-on-year to Tk 8.61 billion in January-March this year.

Islami Bank entered into fresh losses of Tk 2.88 billion in January-March, against profits of Tk 298 million in the same quarter last year, due to higher provisioning requirements and a negative net interest margin.

babulfexpress@gmail.com

© 2026 - All Rights with The Financial Express