Asset-quality reviews conducted by foreign firms this year have uncovered hidden bad debts and under-reported non-performing loans (NPLs) in domestic banks and other financial institutions, exposing the futility of the local credit rating industry.

Experts say the industry is overcrowded, creating fierce competition among agencies that allows clients to secure higher ratings at lower costs. As a result, credit ratings-the core product they sell-lose credibility, undermining the very risk assessments on which investors rely before deciding where to invest.

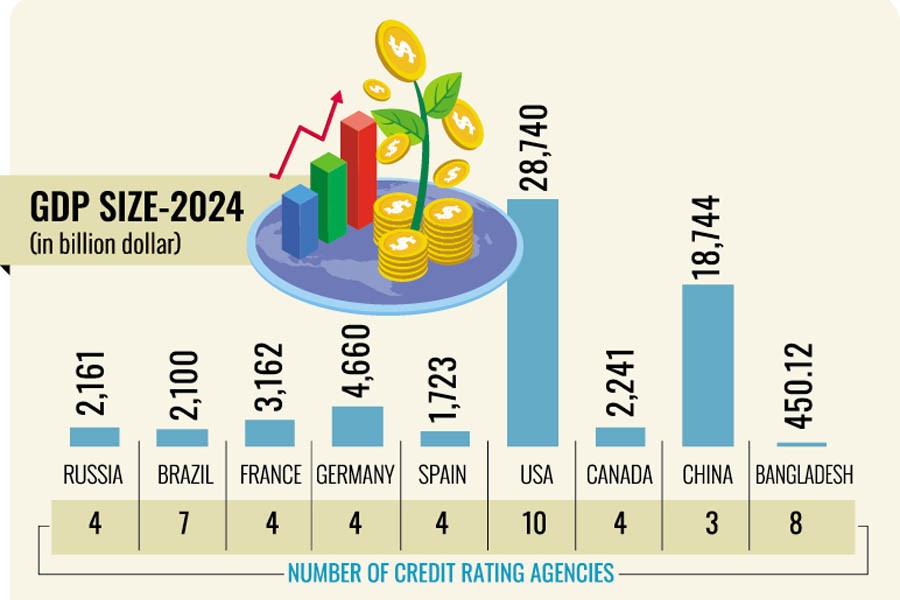

Bangladesh has four times as many rating agencies as India and 2.6 times as many as China, despite its economy being only 8.7 per cent the size of India's and just 2.4 per cent that of China's.

The growth of the financial sector depends heavily on rating agencies, and the challenges they face in Bangladesh have drawn attention as the government now considers measures to support the expansion of the bond market.

While presenting research findings at a recent event, Professor M. Kabir Hassan of the University of New Orleans, USA, said Bangladeshi rating agencies compromised on both service quality and pricing as a survival strategy.

For years, they have masked deep asset-quality problems in several banks.

Earlier this year, the public became aware of the sheer scale of non-performing loans-surpassing 90 per cent of total loans disbursed in extreme cases-at Shariah-compliant banks.

Independent reviews by KPMG, EY, and other international auditors exposed the stark mismatch between previous credit ratings, audit reports, and the banks' actual financial health.

For example, First Security Islami Bank had consistently received an ST-2 short-term rating and an A+ long-term rating since FY16, continuing through the change of political regime in August last year. These ratings implied a strong ability to meet financial obligations with low credit risk.

The latest review, however, downgraded the Islamic bank's ratings to ST-4 short-term and BB+ long-term. While A+ indicates a strong but somewhat vulnerable repayment capacity, BB+ suggests inadequate repayment ability, substantial uncertainties, and speculative elements.

Similarly, the shift from ST-2-meaning very strong capacity for timely repayment and low credit risk-to ST-4, which indicates weaker repayment capacity and higher risk, highlighted a sharp deterioration in the bank's financial health.

"In the case of First Security Islami Bank, we clearly see an example of mis-rating by the credit rating agencies. A bank's rating cannot change overnight. This suggests that the agencies either acted under political influence or were swayed by financial incentives," said M. Jahangir Alam Chowdhury, professor of finance at the University of Dhaka, in a telephone conversation with the correspondent.

The research paper presented by Professor Kabir Hassan recommends adequate oversight and support to ensure the credit rating industry conforms to international standards.

The study also identifies the lack of credible rating agencies as one of the key obstacles to bond market development in Bangladesh.

Bangladesh will require around $608 billion in investment for sectors such as water, power, telecom, ports, airports, railways, and others. A significant portion of this funding should ideally come from the bond market.

Globally, bond issuance requires a credit rating, which involves a comprehensive risk assessment covering financial and economic factors, accurate cash flow forecasts, bond structure, and project viability. Rating agencies serve as impartial and professional assessors of such risks worldwide.

Until 2008, Bangladesh had only two licensed credit rating agencies. Later, six more licences were granted. With limited rating assignments, many of these agencies are now on the verge of collapse.

"We need stronger regulation to systematically reduce the number of agencies. If only one or two strong firms remain, they would be able to hire qualified experts-mathematicians, finance professionals, accountants, statisticians-ensuring credible ratings," said Prof. Alam Chowdhury.

There should also be mandatory re-audits of ratings. Agencies responsible for poor or misleading ratings should face penalties, and ultimately such firms should be forced out of the market.

"We must change the current situation, where too many agencies are chasing too few issuers," added Prof. Chowdhury.

farhan.fardaus@gmail.com

© 2026 - All Rights with The Financial Express