Eastern Bank Limited (EBL) has registered 55-per cent growth in net profit in the first half (H1) of this calendar year amidst the Covid-19 pandemic.

This growth has been ascribed to efficient management of its balance sheet complying with all the key regulatory requirements of liquidity.

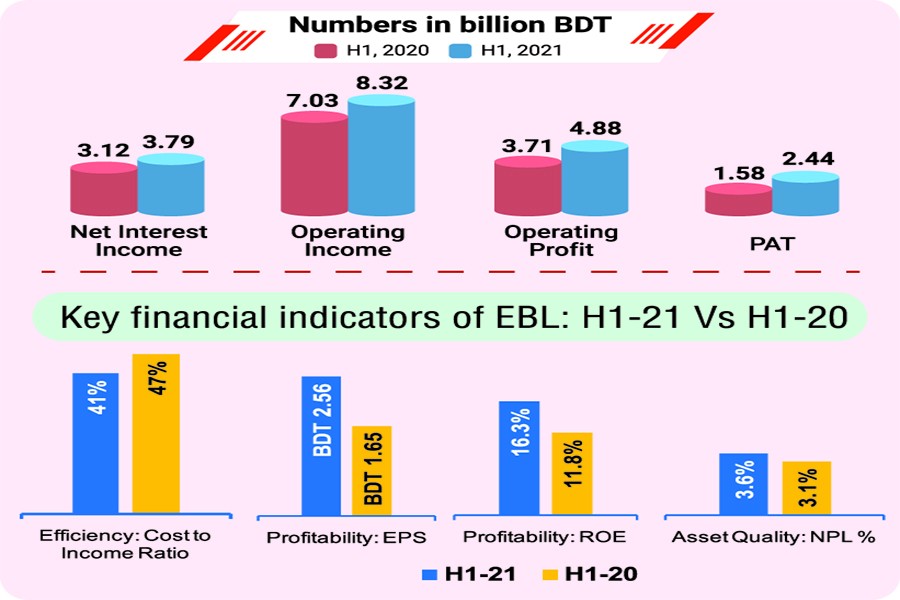

The bank's operating profit grew over 31 per cent to Tk 4.88 billion during the January-June period of 2021 from Tk 3.71 billion in the same period last year.

In the meantime, its operating income rose more than 18 percent to Tk 8.32 billion from Tk 7.03 billion.

Net interest income (NII), the core component of operating income of a bank, of this lender grew 21 per cent in H1 of 2021 over that of H1 in 2020.

It appears at the top of the income statement.

On the other hand, operating profit is the result of operating income (NII and other revenues like investment and fees) less operating expenses.

However, EBL's net profit, officially known as profit after tax, jumped nearly 55 per cent to Tk 2.44 billion in H1 of 2021 despite a lower demand for credit due to Covid-19.

It was Tk 1.58 billion a year ago.

Credit growth, particularly in the private sector, has maintained a falling trend in recent months for the ongoing second wave of the pandemic in Bangladesh.

Private-sector credit growth rose to 8.40 per cent year on year in June 2021 from 7.55 per cent a month ago.

The growth was 8.79 per cent in March 2021.

It was 6.40-percentage point lower than the Bangladesh Bank (BB)'s target of 14.80 per cent for the second half of fiscal year 2020-21.

“Actually, the private commercial bank (PCB) has been able to reduce its cost-to-income ratio through rationalising operational expenses”, according to EBL chief financial officer Masudul Hoque Sardar.

The bank's ratio came down to 41 per cent in the first six months of 2021 from 47 per cent in the same period of 2020.

Such ratio is important for determining the profitability of any bank or financial institution. It is calculated by dividing the operational expenses by the operating income generated.

On the other hand, deficit net operating cash flow of the EBL dropped by over 23 per cent or Tk 2.71 billion to Tk 8.83 billion in H1 of 2021 from Tk 11.54 billion in the same period of 2020.

Deficit of consolidated net operating cash flow per share was Tk 9.25 for H1 of 2021 against last year's Tk 12.10 in the same period, according to the bank's data.

Negative cash flow does not mean that the EBL is facing a liquidity shortfall, rather indicates that it has funded loans by borrowing from other sources instead of deposits in this period under review.

"It is not the negative operating cash flow, but consistent compliance with all the key liquidity ratios by EBL indicate its true strength in liquidity," Mr Sardar told the FE while explaining the overall liquidity situation of the PCB.

EBL deputy managing director Mehdi Zaman said, "Our core deposit decreased slightly during the period under review because of withdrawing a significant amount of high-cost fixed deposits, particularly double return deposit schemes."

The EBL has funded loans by borrowing from other sources instead of deposits to ensure maximum return from investments, he tells the FE.

"We've a strong footing on our capital base," the senior banker says, adding that they have enough buffers to withstand minor-to-moderate shocks.

Meanwhile, the EBL has been able to manage all the regulatory liquidity ratios in line with Basel-III framework excepting net stable funding ratio (NSFR) during the period in question.

The second-generation PCB maintained liquidity coverage ratio at 143.10 per cent against minimum requirement at 100 per cent in H1 of 2021 while the NSFR was 94.30 per cent instead of 100 per cent.

Besides, the EBL's advance-deposit ratio (ADR) stood at nearly 80 per cent during the period against the regulatory maximum ceiling of 87 per cent, meaning it has still room to grow as far as ADR is concerned.

The BB earlier set the safe limit of ADR at 87 per cent for conventional banks and at 92 per cent for Sharia-based Islamic banks.

The EBL is very much aware of following good governance and compliance culture to ensure world-class banking services through continuous improvement in customers' experience, according to Mr Sardar.

siddique.islam@gmail.com

© 2026 - All Rights with The Financial Express