Mohammad Mufazzal and Farhan Fardaus | August 22, 2024 00:00:00

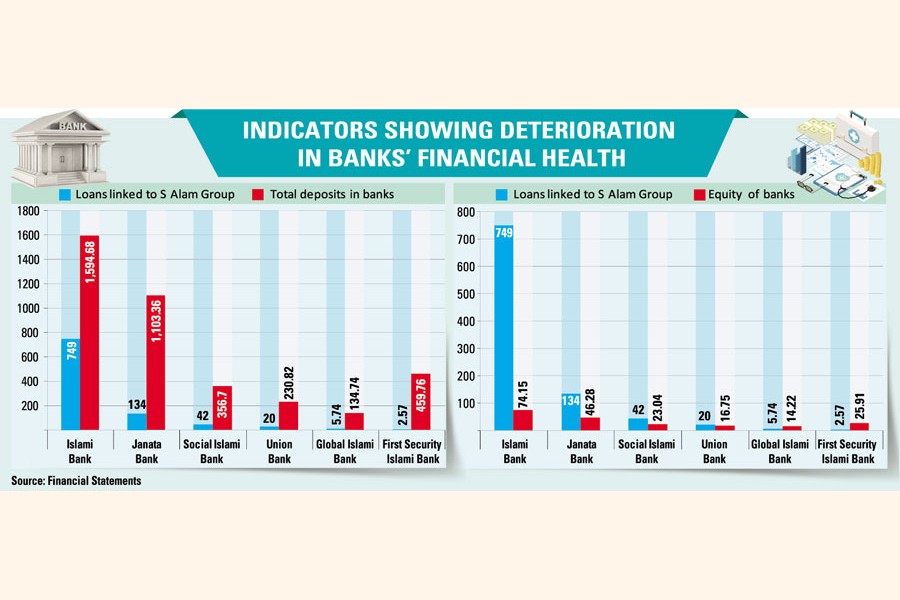

S Alam Group and its associates took out loans from Islami Bank ten times its equity whereas a single party or group should not be given more than 25 per cent of a bank's capital in loans.

The Bangladesh Bank enforced the exposure limit in a directive issued in 2022 but overlooked its violation by Islami Bank.

The group that has become infamous for defaulting on huge amounts of loans exceeded the exposure limit with four other banks too -- Social Islami Bank, Janata Bank, Union Bank, and Global Islami Bank.

Altogether, S Alam Group borrowed Tk 953.31 billion from six banks whereas the lenders' aggregated equity is Tk 200.35 billion. First Security Islami Bank is the only one among the six banks which lent 10 per cent, within the limit, of its capital to the group.

This is the backdrop against which the securities regulator imposed restrictions on purchase, sales and transfer of shares by entities of S Alam Group, its owners and family members of the banks.

The move will help recover loan money - at least partially, said Md. Moniruzzam, managing director of Prime Bank Securities.

"The government will have to set rules to sell out the shares of S Alam Group and his associates," he added.

However, the loan amounts are much higher than the banks' total equity, which means the money, if recovered, from selling S Alam's stakes in the banks will be negligible.

The problem was made worse as the lenders kept on rescheduling loans over the years, taken by S Alam Group and its associates.

Banks usually keep 1 per cent general provision against regular loans while they are supposed to keep 100 per cent provision against bad loans. Loans become sour when 12 installments are missed in a row.

Thanks to rescheduling, defaulted loans of S Alam Group were shown as regular loans. So, any support from the provision against the loans is unlikely.

Moreover, the central bank's relaxation of loan classification policy and rescheduling process made it harder to understand the magnitude of the problem.

Lets' consider an example to illustrate the matter in hand.

Suppose, a listed bank X has equity worth Tk 22, the amount invested by owners.

Deposits received by the bank amount to Tk 200 and S Alam Group took out a loan worth Tk 42 from this bank.

If the borrower defaults on loan repayments, the equity will be Tk 20 in the negative, meaning shareholders' equity will get wiped out.

In consequence, the actual value of the deposits will come down to Tk 180 from Tk 200.

In that case, depositors will have to sacrifice 10 per cent of their funds kept under the custody of X unless the government takes any measure to compensate for the loss.

The bank's provisioning, if any, against the bad loan can be an instrument to tackle the negative impact on the depositors. If the bank can get a support worth Tk 20 from the provision account, depositors will remain unaffected.

Apart from the lack of proper provisioning, the Shariah-compliant banks are facing absence of other support mechanisms as well.

The scheduled banks are required to maintain cash reserves equivalent to 4 per cent of total deposits and 13 per cent statutory liquidity with the Bangladesh Bank.

Statutory liquidity remains invested in government bonds.

The banks which maintain these compliances properly get support from the tools during a crisis period.

But Shariah-compliant banks maintain compliances at a reduced ratio for their limited scope of operations.

Hence, Islami Bank, Social Islami Bank, First Security Islami Bank, and Global Islami Bank will not have the support at this critical juncture.

Besides, industry experts are skeptical about the collateral used for the loans since in most cases S Alam Group had its own men deployed in the boards of the banks when the loans were sanctioned. The business conglomerate had forcefully taken over control of the boards of Islami Bank and Social Islami Bank. Its ownership of First Security Islami Bank and Global Islami Bank is also marred by corrupt banking practices.

S M Galibur Rahman, head of research & strategic planning of Shanta Securities, said the loans granted to S Alam Group had been approved based on political grounds rather than project merits.

"We expect the new governor will ensure the proper reporting and provisioning in accordance with international standards," he said.

The banking commission, a proposed body, is expected to take proper steps to solve the issue of non-performing loans.

Asif Khan, chairman of EDGE Asset Management, said an audit is required to address the problems with the troublesome banks.

If the equity of a bank is wiped out, depositors may not get back a portion of their money.

To revive a bank, small depositors should be paid back fully while large ones can be offered equity against deposits.

"A further inclusion of fresh funds and management efficiency can turn a troublesome bank into a profitable entity. This is the strategy that helped Eastern Bank to get in the good books of the financial sector."

mufazzal.fe@gmail.com

farhan.fardaus@gmail.com

© 2026 - All Rights with The Financial Express