The state-run Investment Corporation of Bangladesh (ICB) has reported first-time loss for the Q1, FY24, but the last 14-year data points to inefficient management from the start that has pushed it to the verge of collapse.

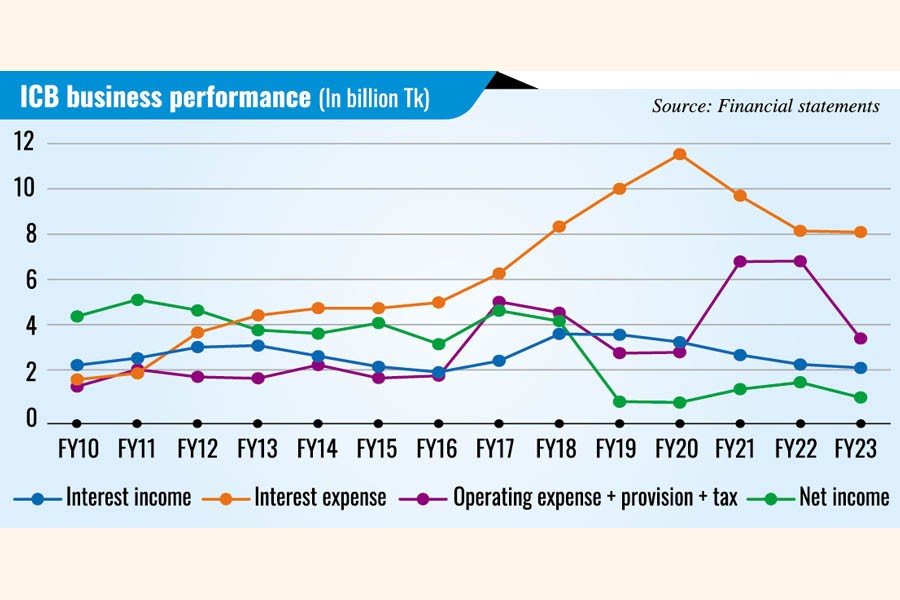

Its interest expense grew at a much faster pace every year between FY10 and FY23, compared to the growth of interest income, but nothing was done to rein in the situation. As a result, interest expenditure ballooned to nearly double the operating income by the end of FY23.

If all the expenses and earnings are taken into consideration, the overall cost was almost equal to its total income in FY23.

Against the backdrop of the high interest rate regime that began in July and is expected to continue to tame inflation, the burden of interest payment will only mount.

With the floor price in place in the stock market, another major source of income of the ICB, the possibility of a boost to its earnings is thin.

In that case, there is a risk that the biggest investment bank of Bangladesh will be dragged into negative equity. The cash flow already turned negative in FY23, corroborating the analysis by the FE correspondent.

"It is true that we will deal with negative equity if the floor price is lifted. But I believe we will be able to recover," said Md. Abul Hossain, managing director of the ICB.

"Negative equity is not uncommon for ICB; we had negative equity in FY20," he added.

To survive through the period of higher interest, Mr Hossain said the ICB would require support from the Bangladesh Bank. He said the organisation was in such a sorry state because it had to provide liquidity and other support to the capital market.

"We gave funds to the Capital Market Stabilisation Fund to support the capital market. We have already informed the government about our situation and the government is convinced. If the market situation improves after the national election, we will recover. Our 80 per cent investment is in A category securities. Our portfolio is good.

"We are not solely responsible for this situation. We need at least Tk 50 billion [from the BB] to operate smoothly.

Gradual decline in financial health

The average annual rise in interest expense was 16 per cent in the 14 years to the end of July, whereas interest income had risen at an average 1 per cent every year during the period.

In FY23, the ICB paid Tk 8.14 billion in interest against the funds that it had borrowed, while earned only Tk 2.24 billion against the money it had lent.

Its interest income came mainly from investments in bonds, government securities, loans given to its subsidiaries, and margin loans. On the other hand, the investment bank mainly paid interests on short-term loans and subordinated bonds it had floated.

As the widening gap had kept weakening the financial health of the organisation, the yearly 22 per cent increase in operating expenses (salaries, allowances, tax and other bills) over the 14-year timeframe added to the woes.

Apart from interest income, the ICB had income in the form of dividend, capital gains and fees.

On an average, the annual interest expense was as big as two thirds of the aggregate income from dividends, capital gains, and fees.

The head of the ICB said the annual net income eroded as the opportunity to make capital gains diminished for the floor price.

Asked what will happen if the market does not recover anytime soon, Mr Hossain said, "ICB will be able to survive for six months even if the market goes into a bad situation after the withdrawal of the floor price. We believe the capital market will gain back its momentum before June 2024.

"But there is no doubt we will need backing to operate and survive."

farhan.fardaus@gmail.com

© 2026 - All Rights with The Financial Express