The insurance sector regulator has amended rules to ease the appointment of chiefs to insurance companies, as the earlier eligibility criteria were tough to meet.

Insurance company representatives have welcomed the amendment to the Insurance Company (Chief Executive Officer Appointment and Removal) Regulations, 2012.

The revised rules are intended to simplify the CEO appointment process, widen the pool of eligible candidates, and ensure the placement of qualified and competent professionals, while introducing stricter measures against corruption and misconduct.

"The changes have long been needed," said Syed Sehab Ullah Al-Manjur, CEO of Pragati Insurance.

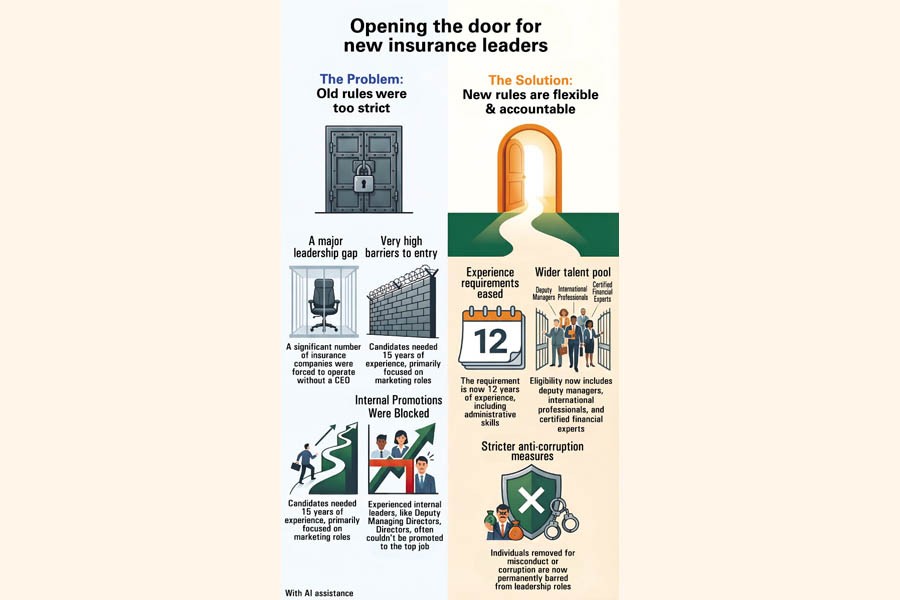

According to the Insurance Development and Regulatory Authority (IDRA), a significant number of insurance companies are currently operating without chief executive officers (CEOs). Many firms have experienced professionals serving as additional managing directors (ADMDs) and deputy managing directors (DMDs), but they could not be promoted to the top positions due to the stringent recruitment criteria under the previous rules.

This is the backdrop against which IDRA amended the regulations to facilitate the appointment of CEOs. The revised rules are also expected to help ensure timely appointments.

Under the revised framework, senior officials from the general insurance and life insurance sectors, as well as ADMDs and DMDs of private insurance companies, will be eligible for the position of CEO. The eligibility criteria have also been expanded to include senior management professionals working with internationally recognised multinational insurance companies.

In addition, the amended regulations ease appointment conditions for candidates holding recognised professional qualifications or designations, including actuaries and fellows or associates of CPA, CFA, CLU, ICAB, ACCA, and ICMAB.

The regulator has also extended the timeline for CEO appointment and renewal processes. The maximum time between the submission of applications and the authority's announcement of decisions has been increased to 60 days from 15 days.

Previously, 15 years of experience was required for the position, which has now been reduced to 12 years. Earlier, candidates' marketing experience was taken into account; now, administrative experience will also be considered when appointing CEOs in insurance companies.

Moreover, anyone who has worked as a DMD for at least one year will qualify for the chief executive position, which was not allowed under the previous rules.

At the same time, IDRA has introduced stricter provisions to prevent individuals with records of misconduct from holding executive positions. Under the new rules, any person who has been removed from an insurance company or financial institution for abuse of power, corruption, money laundering, or financial irregularities-or whose appointment as CEO or renewal application has been rejected-will be barred from being hired by any insurance company in the future.

IDRA expects that the revised regulations will facilitate the appointment of highly qualified professionals and strengthen transparency and accountability across the insurance sector, ultimately boosting public confidence in the industry.

farhan.fardaus@gmail.com

© 2026 - All Rights with The Financial Express