Thousands of investors burnt their fingers in the stock market debacles in 1996 and 2010, and many of them are yet to recover from the financial damages inflicted on them in the latest incident.

They see the value of their assets is still less than their investment, a factor discouraging enough for liquidation of securities.

The negative equities in investors' portfolios currently amount to Tk 46.59 billion, and so the liquidity flow in the money market must be impacted or reduced by nearly as much.

Until the latest market crash, the capital market stood only on equity-based securities. That raises a question whether investors could have cut down investment risks had they have diversified products to put their money on.

Examples of other countries indicate that a diversified market protects investors better from market volatility. They create multiple options for investments by introducing products, such as bonds, ETF (exchange traded funds), Sukuk (Shariah-compliant bonds) etc. Risk with equity shares is usually higher than with others.

The diversification of the country's capital market had remained pending for years in the absence of rules and regulations, market infrastructures and adequate training of the market operators.

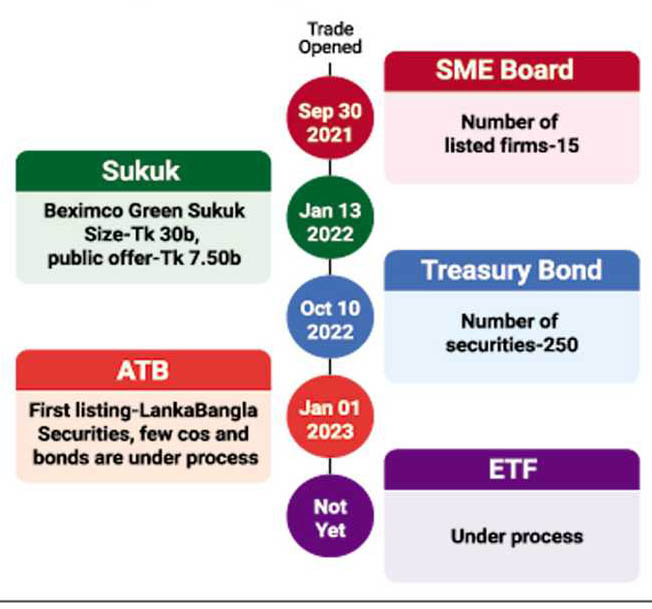

Over the last couple of years as the pandemic added to the market instability, the regulator has brought in a separate trading board for listing and trading of stocks of small and medium enterprises (SMEs) and two new products - Sukuk and treasury bonds.

Alternative Trading Board will come into operation in January and ETF is still in the pipeline.

The already-operational SME board has not boosted investor participation much.

A matter of great concern in this is the investors' lack of understanding about the market dynamics. The greatest weakness of the country's capital market is that around 80 per cent of the investors are retailers with a tendency to make short-term gains from trading in the secondary market.

The same reason is pointed out for not-so-enthusiastic response towards T-bonds.

Supply shortage is another major factor as to why the transaction of T-bonds has not gained momentum.

Chairman of the Bangladesh Securities and Exchange Commission Prof. Shibli Rubayat Ul Islam said in a recent programme that even if the newly-introduced products were yet to make any visible impact, the market and investors would be benefitted in the long run.

Chairman of the Dhaka Stock Exchange (DSE) Md. Yunusur Rahman echoed the view. He said it takes time to make a product popular.

However, insiders say a state-of-the-art trading platform is imperative to run simultaneous and quick trading of multiple products. The frequent technical disruptions observed in the premier bourse send out warnings to investors.

"We cannot deny the flaws. But the situation will improve soon through the introduction of a new data centre," said the DSE chairman.

Trading of T-bonds insignificant

The long-anticipated trading of treasury bonds (T-bonds) began on October 11. The system of transferring the units of the bonds to BO (beneficiary owner's) accounts is yet to become smooth as several parties are involved there.

The Bangladesh Bank is the regulator of T-bonds, and these are usually traded through beneficiary participant identification (BPID) accounts. But when the bonds are traded on the secondary platform, the sell-buy activities should take place through investors' BO (beneficiary owner's) accounts.

DSE officials said the process of transferring bonds had eased to a great extent but the bonds were in short supply.

Executive Director at the Policy Research Institute (PRI) Ahsan H Mansur said the government's policy was not supportive of the bond market.

He said banks wanted to purchase treasury bills at an interest rate that ensured their profit, but the government often cancelled auction of treasury bills when banks demanded interest at above 9 per cent.

The lending rate cap is set at 9 per cent by the central bank.

"The central bank purchases the treasury bills at lower interest rates. This is not supportive of the growth of the bond market," Mr. Mansur said.

Investors of long-term bonds are not willing to hand over such instruments, he said, adding that savings certificates should be tradable and the government must come up with flexible policies to create demand for new products.

The securities regulator has introduced a mandatory provision of 30 per cent debt securities in the portfolios of stock brokers and dealers, a DSE official said.

"We hope investors' participation in transactions of the T-bonds will increase in the days to come," he added.

ETF yet to start operation

An ETF is a collective investment scheme that continuously issues and redeems its shares. Three companies are at an advanced stage of launching the ETF. The LanakaBangla Finance has submitted an ETF of Tk 1.0 billion.

Green Delta Insurance has come up with a proposal of forming an ETF of Tk 500 million while Shanta Capital has set out for forming a fund of Tk 1 billion.

The ETF can be in passive or active form. Insiders say that the securities regulator wants the ETF to be in active form, meaning investments can be in diversified products. Information about the security purchases with the funds will be available in quarterly disclosures.

On the other hand, ETF in passive form is index-based such as DS30. In this case, investors are well aware of the securities comprising the ETF, but in the context of Bangladesh's capital market, investment would lack diverse products.

Dr Mizanur Rahman, a commissioner of the securities regulator, said the three funds had been applied for in the last three months.

The ETF funds will be approved by the end of the year, he said.

mufazzal.fe@gmail.com

© 2026 - All Rights with The Financial Express