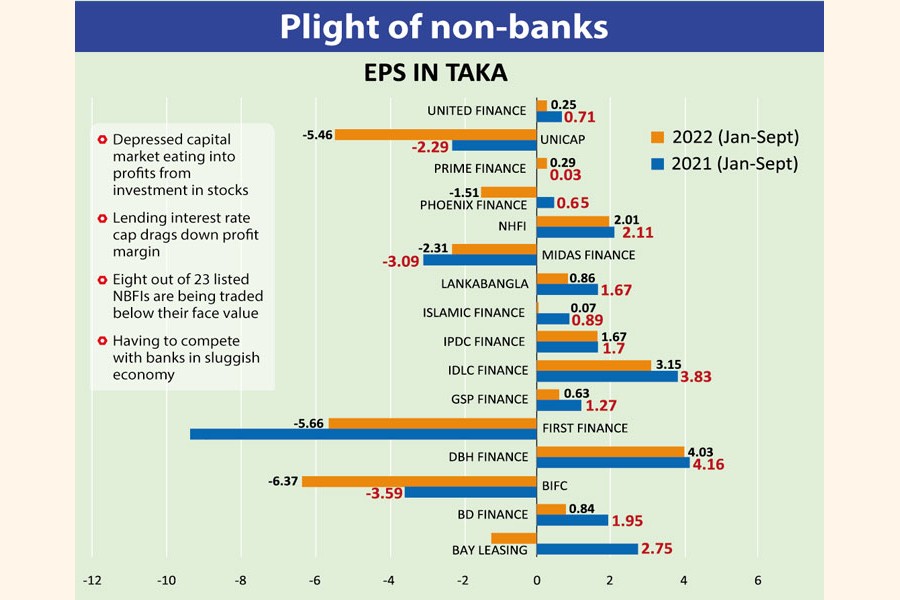

The bearish stock market and the lending interest rate cap have been eating into profits of non-bank financial institutions, worsening the health of the overall sector.

Most of the companies that logged handsome profits in 2021 watched their income drop, while some others went into the red between January and September this year.

Of the 23 NBFIs listed with the Dhaka Stock Exchange, 16 have published their quarterly financial statements until November 6. Except for one, all suffered a year-on-year fall in earnings per share in the nine months through September.

Two of them, Bay Leasing & Investment and Phoenix Finance & Investments stepped into the loss-making zone during the time.

Four companies, Bangladesh Industrial Finance, First Finance, Midas Financing and Union Capital continued to incur losses for the second year this year.

"The main reason behind the erosion of the profits is lower interest income from lending and lower return from the share market investments," said Mominul Islam, chairman of the Bangladesh Leasing and Finance Companies Association, a platform of non-bank financial institutions.

The global economic crisis that emerged out of the Russia-Ukraine war resulted in a tightening of the liquidity flow in the financial sector of Bangladesh this year.

Against this backdrop, the leasing company association recently requested the Bangladesh Bank to lift the cap on interest rates on loans and deposits.

The interest rate cap --7.0 per cent for deposits and 11 per cent for loans - for non-bank financial institutions affected their profit growth, said Mir Ariful Islam, managing director of Sandhani Asset Management.

"A major constraint on the business of the financial institutions has been the narrowing of the gap between the deposit rate and the lending rate," he added.

Some weak NBFIs have felt compelled to offer higher interest rates than 7 per cent to collect deposits while their lending rate has remained the same, bringing down their profit margin, said a merchant banker requesting anonymity.

"This way these institutions are putting depositors' money at risk," he said, adding that some of them have already been struggling to pay back depositors upon the maturity of their schemes.

Meanwhile, the central bank has decided to raise the maximum bank interest rate on consumer loans to 12 per cent from 9.0 per cent after economists and bankers repeatedly insisted on the withdrawal of the cap on loans to contain inflation.

The central bank should also consider lifting the interest rate cap on other loans and issue a circular to ensure transparency in this regard, said a managing director of a leasing company, requesting anonymity.

NBFIs are expecting a similar move for them.

IDLC Finance, one of the leading non-bank financial institutions, lost 17.61 per cent profit year-on-year to Tk 1.31 billion in the nine months until September.

IPDC Finance's profit sank 1.75 per cent to Tk 620 million in the same period while the company watched its total operating costs go up 24 per cent to Tk 1.11 billion.

LankaBangla Finance's profit declined 48 per cent year-on-year to Tk 471 million in the nine months.

Six companies have yet to make their earnings data public. People's Leasing & Financial Services has not published reports for three years after the trading of its shares was suspended in July 2019 for persistent deterioration of its financial health for several years.

Dr. Suborna Barua, associate professor at the International Business Department of the University of Dhaka, said the operating cost of financial institutions remained high, but they could not make much profit due to the interest rate cap.

The NBFIs have to compete with banks while the banking sector itself is in a tight situation due to the sluggish private sector credit growth, he said.

Moreover, the country's NBFIs have been following almost the same business model as banks, without any innovation, another reason for lower profit, Suborna added.

Since the capital market is on a downward trend, financial institutions need to keep higher provisions against their share market investments.

Last year, the stock market was bullish and financial institutions did not require provisions amid a suspension of loan classification, which ultimately boosted profits.

Macroeconomic uncertainties owing to the Russia-Ukraine war rendered a volatile stock market. The DSEX, prime index of the DSE, plunged 4.0 per cent or 244 points in the nine months to September.

In contrast, the DSEX had jumped 36 per cent or 1,927 points in the same period last year, compared to the previous year.

The depressed market dragged down the stocks of NBFIs. Eight institutions-Bangladesh Industrial Finance, Fareast Finance, FAS Finance, First Finance, International Leasing, Peoples Leasing, Premier Leasing and Union Capita-are being traded in the capital market below their face value of Tk 10.

babulfexpress@gmail.com

© 2026 - All Rights with The Financial Express