Mohammad Mufazzal

The long-anticipated trading of the treasury bonds (T-Bonds) is not getting momentum because of a clash between the roles and rules of two regulatory bodies.

Bangladesh Bank is the regulator of T-bonds, and they are usually traded through beneficiary participant identification (BPID) accounts. But when they are traded on the secondary platform, the sell-buy activities should take place through investors' BO (beneficiary owner's) accounts.

The transfer of T-bonds from BPID accounts to BO accounts is not smooth as bond holders need permission of the central bank before selling such securities, insiders say.

Asked about any uniform system to ease the trading, DSE Managing Director M Shaifur Rahman Mazumdar said, "More initiatives should be taken by both the regulators [the central bank and the Bangladesh Securities and Exchange Commission] to ease the transactions of the bonds."

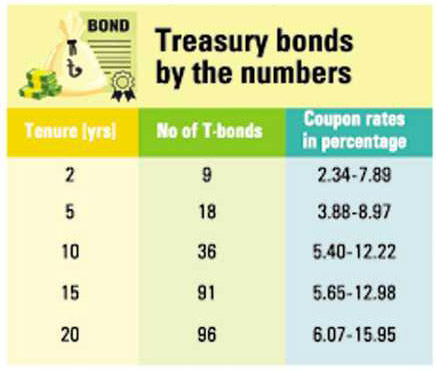

T-Bonds are tradable government securities that mature in between two and 20 years.

Presently, there are 250 T-bonds listed with both the stock exchanges.

The face value of the T-Bonds is Tk 100 per unit and the market lot consists of 1,000 bonds, meaning an investor will have to invest at least Tk 100,000 to take part in transactions.

As per the existing provisions, a seller will get the selling price along with the accrued interest while the buyer will get the coupon money that is deposited into his/her bank account through Bangladesh Electronic Funds Transfer Network.

The trading of the T-bonds began on October 11. Two bonds worth Tk 1,004,390 were executed on the Dhaka Stock Exchange (DSE) while the Chittagong Stock Exchange (CSE) witnessed trades of units worth Tk 105,190.

Since then, no more trades have taken place on the bourses though there are buyers available in the secondary market, traders say.

Another issue is the circuit breaker imposed on the trading in the stock market.

There is no circuit breaker when trading is executed under the system of the central bank.

On the other hand, the securities regulator has imposed 2.0 per cent circuit breaker to prevent the stocks from a further decline, a policy that applies to T-bonds when traded in the secondary market.

In a recent meeting, treasury heads of the banks have told the securities regulator that bond holders were not happy with the circuit breaker imposed in the secondary market. But the securities regulator is not willing to lift it at this moment, considering the interest of general investors, to whom T-bonds are a new product.

Beyond these barriers, a senior official of LankaBangla Securities said, "T-Bonds are a new product for general investors having no literacy on it. That's the reality and it will take some time to popularise the product."

He executed two trades on the day of debut trading.

The objective behind the introduction of T-bonds in the stock market is to diversify it and investors' portfolios through risk-free and fixed-coupon bearing debt instruments.

Officials of the Bangladesh Bank and the BSEC said more moves would be undertaken to enhance the transaction volumes of the T-Bonds in the secondary market.

"The awareness of public and investors regarding T-bonds is yet to be enough," said Abul Kalam Azad, spokesperson of the central bank.

Representing the securities regulator, Mohammad Rezaul Karim said it had asked the market operators to create awareness among traders and investors.

The BSEC itself has been engaging in creating awareness among traders and investors alongside boosting liquidity through market intermediaries and institutions.

Meanwhile, the Lankabangla Securities held a training programme on October 22, participated virtually by officials of the organisation's 21 branches.

mufazzal.fe@gmail.com

© 2026 - All Rights with The Financial Express