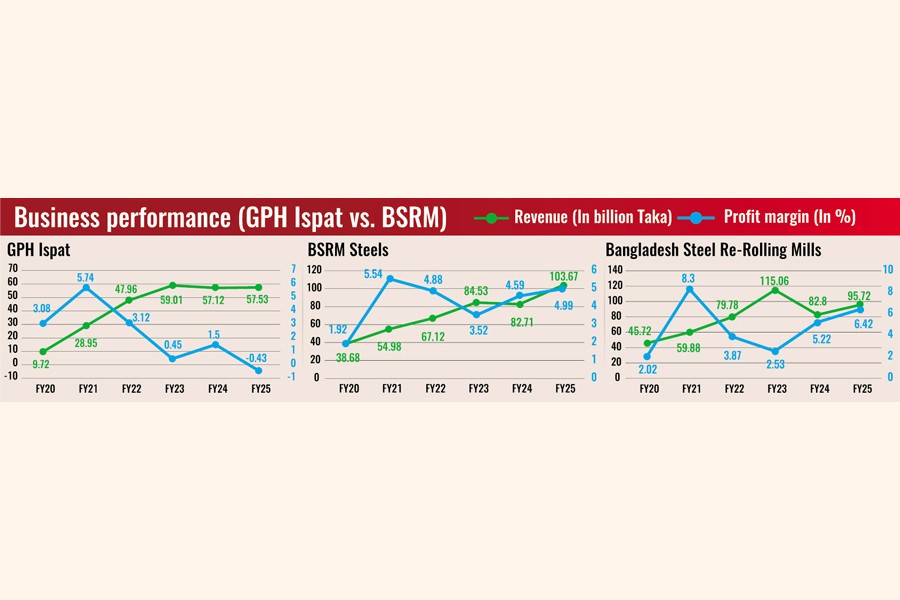

Economies of scale are helping Bangladesh Steel Re-Rolling Mills (BSRM) make profits during a tough period of sluggish market demand, while GPH Ispat has slipped into the red.

The steel industry navigated one of its toughest phases in FY25 as construction in both the public and private sectors faced a setback, energy costs escalated, interest rates increased, and the dollar-taka exchange rate came under further upward pressure. Moreover, the banking sector faced tighter liquidity.

Even with all the adversities, BSRM posted profits for FY25, but GPH Ispat Ltd recorded losses for the first time since its listing, indicating structural differences between the two steelmakers.

Industry insiders say BSRM could overcome the challenges as it took advantage of its cost structure, leverage, and product quality.

Its per-ton production cost is lower compared to GPH Ispat due to higher production and optimised use of induction furnaces and rolling mills. Even when BSRM could not use its full capacity, it managed to keep unit costs down, maintaining thin but positive operating margins.

"We have a large variety of products, and our products are mainly used in government projects…. Despite slow demand, our revenue grew since some government projects were running," said S M Nurul Karim, chief financial officer of BSRM Steels Limited.

In contrast, GPH Ispat's technologically advanced Quantum Electric Arc Furnace (EAF) involves significantly higher fixed and energy costs. With demand weakening, lower capacity utilisation sharply pushed up GPH's per-ton production cost, eroding margins.

"GPH Ispat has modern technology. That's why they are able to produce 600-grade BSTI-approved steel. They need a higher amount of raw materials in the production process due to higher purification, and they need more energy, which may increase their costs," said Dr M Shamim Z Bosunia, a structural engineering expert and president of the Bangladesh Association of Consulting Engineers (BACE).

"This brand positioning doesn't always work because in practice purchasers may not have a preference," he added.

GPH Ispat shifted its focus to premium-grade seismic-resistant steel in drawing a strategy to accelerate business growth, expecting higher demand, but time was not in its favour.

Demand for high-quality steel declined sharply as private sector developers cut costs and postponed projects amid economic and political vulnerabilities. The company struggled to pass on costs to customers due to intense price competition.

"We are the third-biggest market player with more than a 10 per cent market share after BSRM Group and Abul Khair Steel (AKS). Currently, we are facing a lower capacity utilisation problem due to demand shrinkage, but we will be able to generate more revenue when private sector demand rises," said Mohammed Jahangir Alam, managing director of GPH Ispat.

BSRM also produces high-quality products, including seismic steel, but its production has relied on demand from ongoing infrastructure and public sector projects. Its strong brand presence has also allowed limited price adjustments to offset cost pressure.

"We have been working in Bangladesh since 1952. We have a very good brand reputation," said Karim, adding that his company is the market leader with a 30 per cent share.

Another major factor is leverage.

BSRM entered FY25 with a relatively conservative debt profile, keeping finance costs manageable despite higher interest rates.

GPH Ispat, on the other hand, carried substantial credit linked to recent expansion and technology upgrades. Rising interest rates and foreign exchange losses significantly increased finance expenses, which ultimately wiped out operating profits and pushed the company into a net loss.

BSRM's disciplined inventory management also helped it avoid major losses from steel price corrections. GPH Ispat reportedly held costlier raw materials purchased earlier, leading to margin compression when market prices softened.

Market analysts note that BSRM operates with a defensive, volume-driven model designed to withstand downturns. GPH Ispat follows a growth-oriented, high-capex model, which delivers superior returns during boom cycles but becomes vulnerable when demand contracts.

While both companies faced the same macroeconomic headwinds, BSRM's cost efficiency, lower leverage, and volume-focused strategy enabled it to remain profitable, whereas GPH Ispat's high fixed costs, premium-product exposure, and heavy financial burden turned the sluggish business into losses.

farhan.fardaus@gmail.com

© 2026 - All Rights with The Financial Express