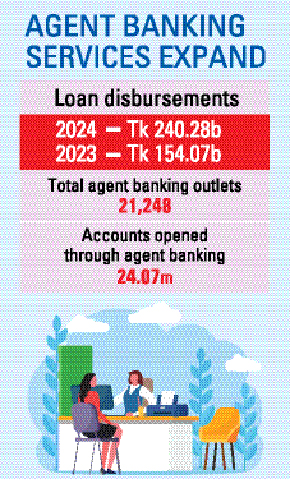

Loan disbursements through agent banking saw a significant year-on-year increase of 55.95 per cent in 2024 to Tk 240.28 billion by December 2024, according to data from Bangladesh Bank (BB).

This surge is attributed to improved access to financial services for rural people, reports BSS.

In December 2023, the amount disbursed stood at Tk 154.07 billion. The rapid growth reflects the ongoing expansion of agent banking services across the country.

Last year, a total of 31 banks offered agent banking services through 21,248 outlets, operated by 16,021 agents. The number of accounts opened through agent banking stood at 24.07 million, with women holding 11.98 million of these accounts and rural customers accounting for 20.61 million.

The deposits in agent banking accounts amounted to Tk 419.55 billion, while the cumulative amount of inward remittances disbursed through agents reached Tk 1.73 trillion.

Bankers observed that with the gradual expansion of agent banking, many people who were previously excluded from banking services at the rural level can now easily access the services, which is the key reason behind the increased flow of such loans.

Talking to BSS, a senior official of the central bank said agent banking is playing a pivotal role in providing adequate financial services, especially for rural women, small business entrepreneurs and the beneficiaries of remitters.

Considering the fact of loan-deposit ratio and the portion of lending to women or entrepreneurs, he said, Bangladesh Bank is constantly encouraging banks to facilitate CMSME, women entrepreneurship loan and some refinance schemes for marginal people through agent banking.

Overall, agent banking is having a significant positive impact on financial inclusion and, therefore, has the potential to fill the gaps left by the traditional branch banking, he added.

Abdul Quaium Chowdhury, Deputy Managing Director of Premier Bank PLC, said that the rising trend of agent banking, especially in rural areas, indicates a remarkable potential to bring unbanked rural people under the umbrella of formal banking services.

He attributed the rise in the number of customers in the banking system to the expansion of new services offered by banks.

Moreover, agent banking is flourishing due to the banks' efforts to provide services at the grassroots level through agent banking, he added.

In the future, he said, agent banking would become more popular.

Besides, he said, many banks have started offering small loans through agent banking, contributing to the growing number of loans.

Bangladesh Bank introduced agent banking in Bangladesh in 2013 with a view to providing a secure alternative channel of banking services. The targeted customers of this service were the underserved population who generally live in remote locations that are hard to reach by the formal banking networks.

Agent banking outlets enable customers to have access to various banking services, including deposits, loans, overseas and local remittances, payment services (such as utility bills, taxes), and receive social safety-net benefits provided by the government.

This model is thus gaining popularity as a cost-effective and convenient delivery channel among the mass people who would otherwise have remained beyond the reach of conventional banking services.

Banks are operating their agent banking activities in accordance with the Prudential Guidelines for Agent Banking Operations in Bangladesh, issued by Bangladesh Bank on September 18, 2017. These guidelines address various aspects, including the agent approval process, permissible activities, and the responsibilities of both banks and agents.

The guidelines also emphasise compliance with anti-money laundering (AML) and combating the financing of terrorism (CFT) measures, as well as customer protection and business continuity, ensuring the safe and effective expansion of agent banking across the country.

© 2026 - All Rights with The Financial Express