Term deposits at banks recorded robust year-on-year growth in the January-March quarter of 2026 as depositors increasingly opted for fixed-income savings instruments to secure higher returns amid a high interest rate environment.

The latest Bangladesh Bank (BB) data suggests customers are locking in their savings for longer tenures, reflecting a growing preference for term deposit products as banks continue to offer attractive returns under the market-based interest rate regime.

The trend also indicates that households and businesses are favouring safer investment options over more liquid deposit accounts, with elevated inflation and economic uncertainty prompting savers to prioritise capital preservation and predictable returns.

The growing preference for term deposits has gradually reshaped banks' funding profiles and strengthened their long-term deposit base while reducing reliance on more volatile forms of deposits.

People familiar with the development say the continued rise in term deposits reflects the combined impact of high deposit rates, tighter monetary policy, and intensified competition among banks to attract stable funding.

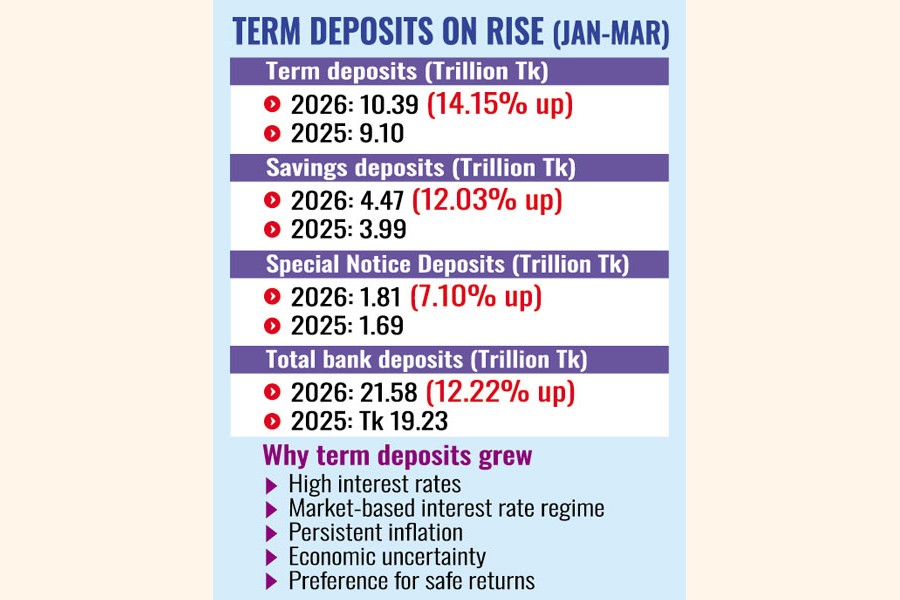

The central bank data shows term deposits accounted for 48.16 per cent of total deposits in the banking sector during the January-March quarter of 2026.

Outstanding fixed deposits rose to Tk 10.39 trillion at the end of March 2026 from Tk 9.10 trillion a year earlier, marking a 14.15 per cent increase.

Savings deposits accounted for 20.72 per cent of total deposits as of March 31, 2026.

The outstanding amount of savings deposits increased to Tk 4.47 trillion during the January-March period of 2026 from Tk 3.99 trillion in the same period a year earlier.

Special notice deposits (SND), which carry relatively low interest rates, rose to Tk 1.81 trillion in the period under review from Tk 1.69 trillion a year earlier.

Overall deposits in the banking system increased 12.22 per cent year-on-year to Tk 21.58 trillion at the end of March 2026 from Tk 19.23 trillion a year earlier, driven by robust growth in term deposits as savers sought higher returns on their investments.

Meanwhile, on June 29, 2026, the Bangladesh Bank directed all scheduled banks to keep the weighted average difference between lending and deposit rates - known as the intermediation spread - within 4.0 percentage points for all sectors, except credit cards and consumer finance.

People familiar with the development say the newly imposed 4.0-percentage-point cap on the interest rate spread is likely to reduce banks' ability to offer higher deposit rates, as they will have less room to adjust lending rates to offset the higher funding costs.

Syed Mahbubur Rahman, managing director and CEO of Mutual Trust Bank, says the strong growth in term deposits was mainly driven by competitive interest rates offered by banks.

"People are increasingly opting for fixed deposits as they are receiving better returns on their savings," he says.

He points out that overall deposits in the banking sector have grown by more than 10 per cent, reflecting improved confidence among depositors.

Fixed deposits remain a more attractive investment option due to their assured returns and competitive interest rates, he adds.

Dr Masrur Reaz, chairman and CEO of Policy Exchange

Bangladesh, says the strong growth in term deposits reflects depositors' response to high interest rates as households and businesses seek safer investment avenues amid persistent inflation and economic uncertainties.

He, however, cautions that the trend may not continue at the same pace after the Bangladesh Bank capped the intermediation spread at 4.0 percentage points.

"Banks are now likely to face greater pressure in balancing lending and deposit rates. If they reduce deposit rates to comply with the spread ceiling, the incentive for savers to keep money in term deposits could weaken", he says.

sajibur@gmail.com

© 2026 - All Rights with The Financial Express