Fahmida Khatun, Mustafizur Rahman, Khondaker Golam Moazzem, Towfiqul Islam Khan, Muntaseer Kamal, and Syed Yusuf Saadat | March 19, 2024 00:00:00

The national budget for FY2024-25 (FY25) will be the first budget prepared by the incumbent government. It will also be prepared under new leadership at the Ministry of Finance. The budget for FY25 is going to be placed before the National Parliament in the backdrop of a number of persistent macroeconomic challenges, manifested in, inter alia, subdued revenue collection, slow budget implementation, high inflation, liquidity crunch in the banking sector, lower momentum of export earnings and remittance inflow, declining forex reserves. In general, the macroeconomic stability has come under considerable pressure owing to both domestic and external factors. The FY25 budget will need to address the attendant challenges as also the medium-term reform issues with a view to restore macroeconomic stability.

Fiscal space was rather limited during the first half of FY24. Revenue mobilisation growth was subdued during the first half (Jul-Dec) of FY24. If the annual growth target of 36.3 per cent is to be met, then total revenue collection will need to grow by a whopping 54.4 per cent during the remainder of FY24 which is an unlikely prospect. If the current revenue mobilisation growth is carried over, then revenue shortfall (i.e., the gap between revenue collection target and actual attainment) at the end of FY24 could reach Tk 820.0 billion.

Restrained approach in the area of public expenditure was observed. During Jul-Dec of FY24, overall budget utilisation was 25.5 per cent (27.2 per cent in Jul-Dec FY23). ADP implementation was low as well. Perhaps this is a consequence of the austerity measures taken by the government, both on its own and as per the IMF conditionalities.

During the first half of the current fiscal year, budget deficit was Tk 78.85 billion. It was Tk 204.0 billion in the same period of FY23. While the budget deficit narrowed, the composition of deficit financing emerged as a more problematic issue. High reliance on scheduled banks for deficit financing have affected private sector credit growth amid liquidity crunch.

Inflationary pressures persisted. During the first eight months of FY24, general inflation remained over 9 per cent at national, rural, and urban levels. Recent increase in electricity prices is likely to make matters worse. Food inflation, both at urban and rural areas, was higher than non-food inflation. Inflation in rural areas was, on average, higher compared to urban areas.

Bangladesh Bank has taken a number of monetary policy measures including increase in policy rates throughout FY24 to restrain inflation. The policy rate increased from 6.0 per cent in March last year to 8.0 per cent in January this year (also applicable for March this year). The pre-existent interest rate caps were removed, replacing them with competitive market-based reference rate (SMART) accompanied by a margin. The SMART rate increased from 7.10 per cent in July last year to 9.61 per cent in Feb this year. The practice of lending to the government by creating money was also halted. The central bank also infused US Dollar into the local market and mopped up liquidity. Projections concerning monetary aggregates were revised, mostly downward, in view of the measures taken.

External sector performance exhibited mixed trends. Export performance has been rather muted, with adverse implications for net export earnings. Import payments decreased both owing to policy interventions and falling global commodity prices. Tightening of imports is hurting the small players in the market as larger players are gaining ground in the commodity market. These trends will have negative implications for future investment.

The trends in remittance flows do not match the growing number of migrant workers leaving for overseas jobs. Trade and current account balances are showing some improvement, but financial account balance continues to be a major concern.

Foreign exchange reserves are yet to stabilise, albeit at lower levels. Slide in exchange rates is likely to continue under the crawling peg system pursued by Bangladesh Bank, which was adopted instead of a fully market-based exchange rate regime. The oft-cited reason is to decrease inflationary pressure. However, as has been reported, importers are already paying considerably higher than the official rate.

The crawling peg system, perhaps, was adopted to reduce the expenditure owing to government’s own imports, or to provide some relief in terms of private sector external debt repayment. However, this is hurting the cause of quick recovery in terms of remittance inflow and export earnings. This is also helping to incentivise transactions through informal channel (hundi/hawala) and encouraging people to not bring back foreign currency and defer foreign exchange repatriation. The measure is also creating additional fiscal burden for the government in the form of export subsidies and remittance incentive, ultimately limiting fiscal space. The government could have resorted to monetary policy tools (exchange rate) instead of fiscal policy tools (cash incentives). The prevailing policy is raising costs for both the government and the banking sector, which importers are passing on to the consumers,

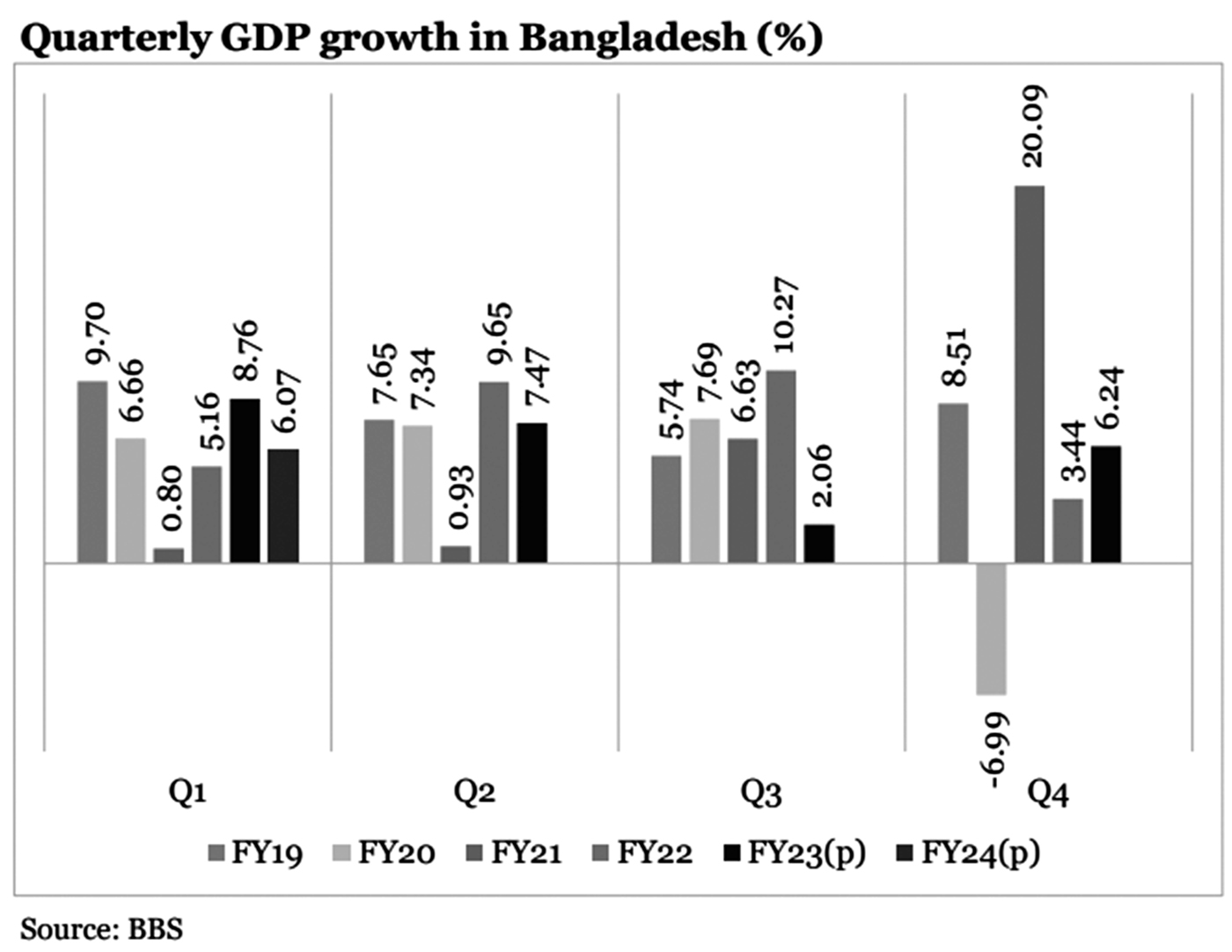

GDP growth declined in the first quarter of FY24. It is encouraging to see that the Bangladesh Bureau of Statistics (BBS) has started to publish quarterly GDP data on a regular basis. During the Jul-Sep period of FY24, estimated GDP growth was 6.07 per cent against the annual target of 7.50 per cent.

Growth of industrial production was lower for all categories of industries (large; small, medium and micro; and cottage) during the second quarter (Oct-Dec) of the current fiscal year. This implies that a slow GDP growth momentum may continue in the second quarter of FY24 as well.

GDP growth in FY24 is more likely to be affected by the macroeconomic policy adjustments. The key macroeconomic management stance ought to be restoring macroeconomic stability, by curtailing the rate of inflation and stabilising exchange rate, even if this comes at the cost of lower GDP growth.

End note: The national budget for FY25 will be placed at a time when the country is facing formidable challenges in a number of areas.

Restoring macroeconomic stability is the main challenge facing the policymakers, who must be cognisant of the present economic realities and identify concrete measures to address the attendant challenges.

The macro-budgetary framework for FY25 must focus on curtailing the rate of inflation and stabilising the exchange rate. Instead of GDP growth, protecting the interests of vulnerable and disadvantaged groups should take the central stage.

Complementarity between the fiscal and monetary policies will need to be ensured by the Ministry of Finance and Bangladesh Bank. The government will also need to focus on deep rooted structural issues given improvement in macroeconomic performance is contingent upon the solution of these issues.

While being cognisant of current realities and designing commensurate measures are important initial steps, implementing the said measures and carrying out the necessary reforms usually turn out to be bigger challenges.

For the policies to produce the intended effects, good governance and discipline are keys. Some hard choices will have to be made on the part of the policymakers. For a political government, the first year of a five-year tenure can be the best time to make some rather unpopular but necessary choices.

Dr Fahmida Khatun is Executive Director, Centre for Policy Dialogue (CPD); Professor Mustafizur Rahman, Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem, Research Director, CPD; Mr Towfiqul Islam Khan, Senior Research Fellow, CPD (towfiq@cpd.org.bd); Mr Muntaseer Kamal, Research Fellow, CPD (muntaseer@cpd.org.bd); and Mr Syed Yusuf Saadat, Research Fellow, CPD. The piece is based on the CPD’s Recommendations for the National Budget FY2024-25, unveiled on March 16, 2024, in Dhaka

© 2026 - All Rights with The Financial Express