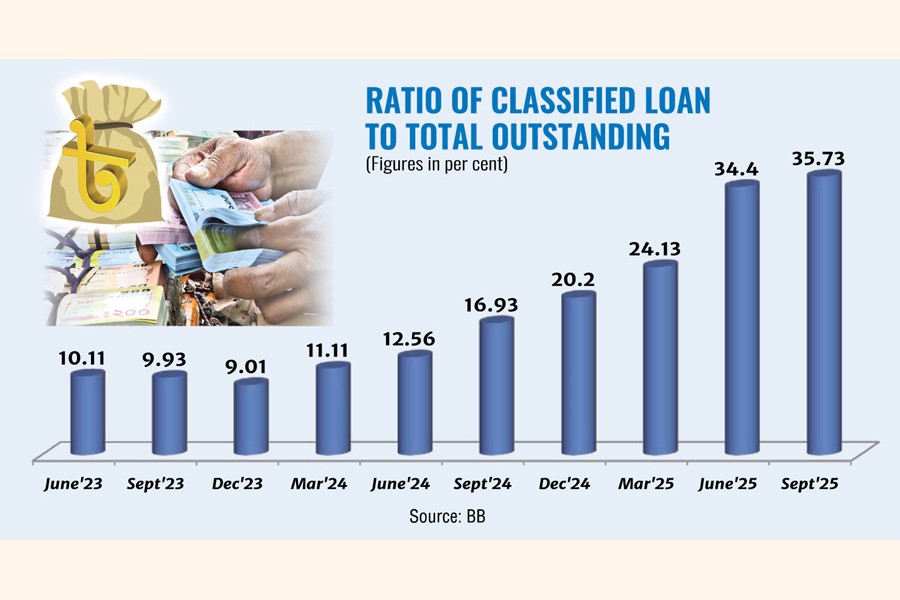

The banking sector in Bangladesh is currently grappling with a critical challenge that poses a significant threat to its stability and future growth: the alarming rise in Non-Performing Loans (NPLs). The factors contributing to this crisis are complex and multifaceted, and it is essential to confront these issues proactively to safeguard both the financial institutions and the broader economy.

At the core of the escalating NPL issue is a weak credit risk assessment process. In many instances, loans are approved without thorough evaluations of borrowers' capacities or the viability of their projects. This lack of diligent scrutiny significantly compromises lending integrity, raising concerns about the sustainability of projects being financed and the banks' responsibilities to their stakeholders. As economic resilience becomes increasingly vital, it is imperative that banks implement rigorous standards for credit evaluation to prevent avoidable defaults.

Additionally, political influences in lending decisions cannot be ignored. The practice of directed lending-where loans are awarded based on personal connections rather than merit-creates an accommodating environment for inefficiency and higher risk. Borrowers who obtain funds through such means often feel less accountable contributing to raise in default rates. This trend not only undermines public trust in financial institutions but also erodes the principles of fairness and responsibility on which these institutions are built.

Compounding the problem is the slow legal recovery process in the judicial system, particularly within the specialised financial courts. Lengthy legal proceedings enable defaulters to exploit delays, thereby hampering banks' recovery efforts. An efficient judicial system should facilitate timely loan recoveries, yet existing inefficiencies disincentivise prompt repayments and foster a culture where rescheduling or writing off loans is normalised. While these practices may temporarily reduce reported NPL figures, they create a false sense of security that ultimately exacerbates long-term risks.

Weak corporate governance within banks further intensifies the NPL crisis. Inadequate oversight regarding loan approvals allows for irregular lending practices, enabling unnecessary risks to flourish within the sector. Moreover, concentrating significant loans among a select group of borrowers increases vulnerability; when these borrowers default, the repercussions can destabilise not only the institution in question but the economy as a whole.

Despite the establishment of committees aimed at tackling the NPL issue, their impact has been limited. While recommendations may be made, the lack of enforcement power often leads to limited genuine progress. Addressing this crisis requires more than discussions; it demands structural reforms that can tackle the root causes of NPLs. Constructive dialogue is essential, but without actionable steps and a commitment to reform, such efforts may dissipate into mere rhetoric.

Given these challenges, the question arises: can Bangladesh realistically adopt international best practices to manage its NPL crisis? While there is potential for progress, several obstacles remain. Regulatory frameworks are improving but have not yet reached international standards. The inefficiencies within the judicial system continue to hinder timely loan recoveries, while political interference obstructs the implementation of stricter global lending practices. These issues call for urgent attention from policymakers, regulators, and banking authorities who must collaborate to strengthen institutional frameworks and enhance compliance.

To pave the way for effective reform, the government must prioritize initiatives that address the inefficiencies ingrained in our legal and banking systems. Streamlining legal processes for expediting loan recoveries will restore confidence among banks and borrowers alike. Reducing political meddling in the lending process will further reinforce credit operations' integrity, ensuring that financial decisions are based on objective criteria rather than personal connections.

A forensic audit is a critical tool that can significantly aid in pinpointing key individuals responsible for the alarming rates of loan defaults. By systematically investigating the factors that contribute to these defaults, forensic audits can uncover the underlying reasons, providing invaluable insights into the incompetencies or misconduct involved. It is essential that forensic auditing be institutionalised across all banks, guided by the stringent prudence required by the Bangladesh Bank, particularly amidst the ongoing reforms within the banking sector. This proactive approach will not only clarify who is accountable and the rationale behind the financial mismanagement but will also gather substantial evidence to support any necessary legal actions. By adopting such measures, we can foster a culture of accountability and transparency, ultimately restoring confidence in our banking system.

Ultimately, it is crucial to acknowledge that the foundations for adopting international best practices are already present in Bangladesh. However, the necessary institutional capacity to act on these frameworks effectively is still lacking. A concerted commitment to enhancing transparency, employing robust credit evaluation methods, and enforcing sound governance practices will position the banking sector for greater resilience.

In conclusion, the increasing prevalence of NPLs in Bangladesh represents a significant challenge that requires immediate and comprehensive reform. The need for a cohesive and proactive approach to address existing weaknesses within the system is clearer than ever. By fostering an environment of accountability, transparency, and adherence to established standards, Bangladesh can navigate the turbulent waters of financial challenges and strengthen the integrity of its banking sector for the future. The time for action is now-economic stability depends on it.

Dr. Md. Touhidul Alam Khan is Managing Director & CEO of NRBC Bank PLC and a Fellow Cost & Management Accountant from ICMAB.

touhid1969@gmail.com

© 2026 - All Rights with The Financial Express