A new look at allocation of advances is of critical importance. Almost the entire sum of bank advances is, indeed, debt capital supplied to several categories of entrepreneurs (borrowers) in different sectors and subsectors of the economy. As per bank statistics on June 30, 2020, the borrowing customers can be divided into two main groups-- (i) more than 99 per cent of the customers with average size of advance Tk.2.58 lac, and (ii) less than 1 per cent of the customers with average size of advance Tk.7.50 crore. Extreme asymmetry is observed between the two groups (hereinafter termed as Bottom 99 per cent , and Top 1 per cent for ease of further references in the discussion). Allocative pattern of advances is indicative of capital concentration, the consequence of which is rise in economic inequality. Which of the two groups should be treated with more equity and justice? Is it wise to carry coal to Newcastle? Is equity maintained across regions?

Data on size-wise advances are available, but not distinctly comparable with classification of entrepreneurs ( cottage, micro, small, medium and large). Besides, the classifications involve unreasonable ranges of investment size. However, an explorative attempt has been made to address the questions raised.

Deposit mobilisation from all kinds of individuals and institutions is not only an important financial function of banks, but also one of the most leading economic responsibilities which have far-reaching effects upon distributional aspect of the economy. Can the pooled savings be lent out indiscriminately (i.e., with no consideration of distributive equity and justice? Savings are transformed into deposits. The banking industry has the opportunity to equitably allocate deposits among numerous entrepreneurs.

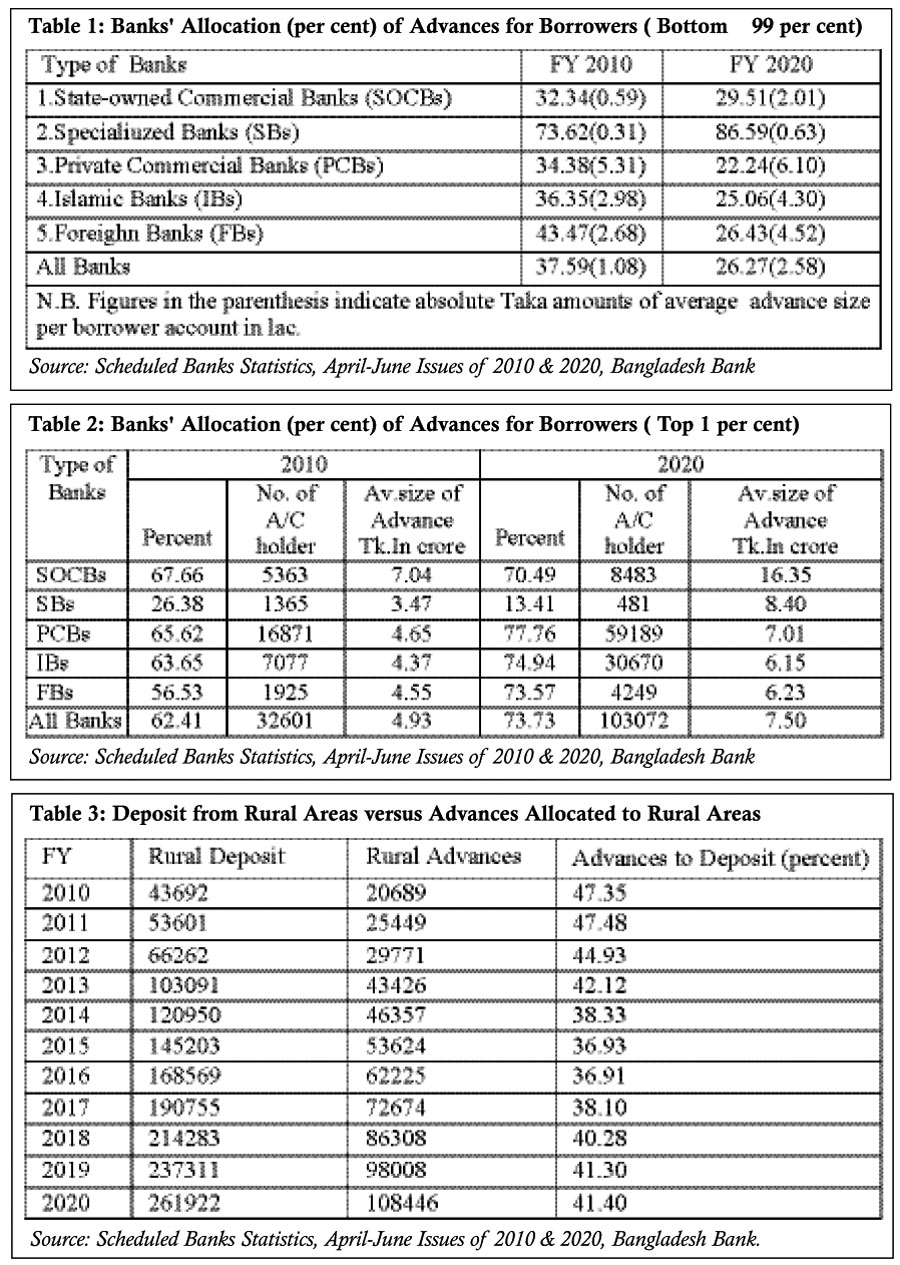

Table 1 shows that in FY 2010, all banks allocated only 37.59 per cent of their total advances (average size per account Tk. 1.08 lac) to the borrowers who fall within the range of advances worth Tk.5000 to Tk.1.00 crore. Even this allocation percentage substantially decreased to 26.27 per cent. Only specialised banks have kept on raising their allocation for the smallest borrowers. Allocation percentages of advances of all other banks have fallen down over the decade and these banks have aligned more to the smaller number of big-size borrowers. State-owned Commercial Banks can accomplish neither desired level of commercial profitability nor social profitability in terms of serving the smallest size of borrowers in larger number.

Table 1 shows that in FY 2010, all banks allocated only 37.59 per cent of their total advances (average size per account Tk. 1.08 lac) to the borrowers who fall within the range of advances worth Tk.5000 to Tk.1.00 crore. Even this allocation percentage substantially decreased to 26.27 per cent. Only specialised banks have kept on raising their allocation for the smallest borrowers. Allocation percentages of advances of all other banks have fallen down over the decade and these banks have aligned more to the smaller number of big-size borrowers. State-owned Commercial Banks can accomplish neither desired level of commercial profitability nor social profitability in terms of serving the smallest size of borrowers in larger number.

Table 2 suggests the real preference of the banks' lending. Except the SBs, all other banks allocate lion's share of their loanable fund for those borrowers who are few in number. These borrower groups fall within 1 per cent of total number of borrowers. Lending seems to be concentrated among less than 1 per cent of total number of borrowers' accounts. In FY 2010, the banks lent 62.41 per cent of their allocated fund to 32601 account holders (Top 1 per cent) representing only 0.36 per cent of total borrowers accounts. The same allocation ratio has increased to 73.73 per cent from 62.41 per cent in favour of 103072 account holders ( i.e. 0.96 per cent ) out of total 10781238.

Table 3 reveals regional disparity over lending allocation. The amount of rural advances in proportion to rural deposits tends to decline on an average over the decade. This is discriminatory for the rural economy. One may argue that the credit requirements of the rural areas are not above the level of fund actually given. This is not acceptable as the rural economy is yet to reach the point of desirable and diversified growth .

Can we hold the lending banks liable for asymmetric allocation of advances? The answer is certainly 'no'. They usually and traditionally assign priority to financial considerations while lending but it is the responsibility of the government to specify the economic direction and to instruct the banks to pursue that. It may, however, be hypothesised that widely diffused lending is less risky than highly concentrated one. Different banks' experiences may vary in this regard. Surprisingly, little research is carried out on banking operations in our country.

Millions of entrepreneurs are required. The majority of them should be developed to launch their activities at small, micro, and cottage categories so that investment is sufficiently spread among the entire productive population of potential entrepreneurs. The role of medium and large entrepreneurs would be naturally determined according to the type of industry or economic activity.

Medium and large entrepreneurs should look for the lion's share of their business fund in the capital market, preferably through share issue. Classifications of entrepreneurs need to be revised to lower the range of investment size. Lending allocation among several sizes and types of borrowers and across regions ought to be backed by the government policy directives. National policy should aim to maximise investment diffusion as much as possible. Accordingly, compatible principles should be framed for entrepreneurship development.

Haradhan Sarker, PhD, is ex-Financial Analyst, Sonali Bank & retired Professor of Management. sarker19582018@gmail.com

© 2026 - All Rights with The Financial Express