Fahmida Khatun, Mustafizur Rahman, Khondaker Golam Moazzem, Towfiqul Islam Khan, Muntaseer Kamal and Syed Yusuf Saadat | January 03, 2023 00:00:00

Bangladesh's external sector has been a key pillar of the country's impressive development narrative. This is manifested in robust export performance and increasing amount of remittance flows, comfortable balance of payment position, high foreign exchange reserves, exchange rate stability, and import capacity that serviced both consumer demands and development needs.

However, in very recent times, the country's external sector has come under considerable pressure, and on all counts - depleting reserves with erosion of import payment capacity, significant weakening of the BDT, high rate of imported inflation, and subdued performance of exports earnings and remittance flows. Policymakers appear to have been caught off-guard by the emergent scenario and are having to resort to fire-fighting to deal with the emergent scenario.

Whilst global factors did accentuate the situation, it is argued here that the underlying reasons originate from a number of policy failures which accumulated over time. These concern several areas: exercise of autonomy and independence of the central bank, forex reserves management, exchange rate adjustment, dealing with capital flight, and overall external sector and financial sector management.

The recent challenges facing the country's external sector have been exacerbated by pent up post-covid demand, recent price hike of essential commodities in the global market and the consequent rise in imports payments, depreciation-induced imported inflation, recessionary fear-induced depressed demand for Bangladesh's exports, and capital flight originating from trade mispricing and diversion of a large part of remittance flows to informal channels.

As may be recalled, for some years now, experts and economists have been drawing attention of policymakers to some of the underlying structural and institutional issues that merit urgent attention and demand concrete actions. These related to enforcement of rules and regulations in the financial sector, maintenance of central bank independence and prudent exchange rate management, among others. For example, economists have been urging for aligning the exchange rate of BDT with market fundamentals. They argued that the managed-float exchange rate regime was undermining export competitiveness, disincentivising remittance flows through formal channels, and encouraging capital flights. Attention was also drawn to the management of forex reserves and lax enforcement of policies against trade mispricing. However, there was a lack of recognition of the gravity of the situation on the part of the policymakers.

Consequently, the external sector, a major mainstay of Bangladesh's robust economic performance, has experienced unprecedented levels of challenges, uncertainties, and volatility in recent period, resulting in the end in Bangladesh being forced to negotiate a USD 4.5 billion balance of payment support from the IMF. Many of the earlier-suggested initiatives are reappearing as stringent conditionalities.

Whilst the challenges faced by Bangladesh's external sector predate the Russia-Ukraine war, the war itself has exposed a number of fault lines and exacerbated the pre-existing weaknesses which characterised the country's external sector management.

This article deals with a number of issues that inform Bangladesh's external sector performance in the early months of FY2022-23. The next sections focus on the followings: (a) sheds light on the decreasing trends in nearly all components of the balance of payments and their impact on the forex reserves; (b) draws attention to the volume-driven nature of Bangladesh's RMG exports and the increased export concentration of recent times; (c) compares the overseas employment trends with incoming remittance flows to show the mismatch between the two indicators; (d) illustrates efforts to rein-in imports and anticipates how declining global prices could ease the pressure on import payments over the coming months; (e) shows the divergence between the Real Effective Exchange Rate (REER) and the Nominal Effective Exchange Rate (NEER), stressing the point that the BDT had remained overvalued in recent years and contributed to stifling the growth of exports and remittances; (f) recommendations as regards ways forward to address emergent challenges facing Bangladesh's external sector.

BALANCE OF PAYMENTS: The balance of payments for the first four months of FY2023 (July-October) shows the overall balance coming down from (-) USD 1.34 billion to (-) USD 4.87 billion (Table 1) and the drawdown on gross reserves from USD 46.5 billion to USD35.8 billion which in terms of equivalent months of imports came down from 6.2 months to 5.2 months. The amount of forex reserves that are not readily available to underwrite imports has been estimated to be worth about USD 8.4 billion. Thus, if the IMF definition of reserves is considered, the current forex reserve would be about USD 27.0 billion or equivalent to about four months of import payments. To recall, the reserve in June 2021 was about USD 46.0 billion or equivalent to about nine months of import payment.

In recent months, there has been a notable rise in import payments underpinned by the significant rise in prices of almost all items in the global market; this is also reflected in the very high growth of L/C settlement related payments. If previously the high flow of remittances helped keep the current account balance in a comfortable situation, this was no more the case, since there has been a significant slowdown in the growth of remittance flows.

A caveat though, import payments for some items such as capital machineries show very high figures, which is also reinforced by L/C settlement figures. This demands a closer scrutiny. This could be only partially explained by the one-time bulk imports of capital machineries for the mega projects. There is a need for an indepth look to check against the likelihood of over-invoicing in this connection. This is particularly because, in general, the customs duties on capital machineries are zero and consequently the possibility of over-invoicing in case of imports of these items is that much higher. Bangladesh Bank has also unearthed incidences of under-invoicing in case of imports to avoid customs duties; the gap amount is settled through payments abroad by transferring money from Bangladesh via hundi/howla informal channels. The import categorisation for these items made by Bangladesh Bank should also be made in a more transparent manner, and the respective HS codes should be made public to ensure greater scrutiny. On the other hand, the significant fall in L/C opening for capital machineries in Q1 also merit closer investigation particularly since these items are associated with performance of export-oriented and import-substituting industries and, as a result, to production and employment.

It is not enough to stop payments when over- and under-invoicings are detected by Bangladesh Bank, as has been the case in recent years. Legal measures must be taken, relevant laws enforced and violators brought to justice to transmit stern signals and forestall such activities in future.

EXPORT EARNINGS: Over the July-November period of FY2023 export earnings have registered a decent 10.9 per cent growth over the corresponding period of FY2022. As expected, performance of RMG had led the way while many of the non-RMG items have posted negative growth over the corresponding correlates of the previous fiscal year. This has led to further concentration of exports favouring the apparels.

However, the impressive performance of apparels is informed by some structural factors that need to be looked at more closely.

The estimations presented in Table 2 clearly reveal the primarily volume-driven nature of export earnings as against exclusively price-driven. As is known, the prices of all inputs for production of apparels (cotton, yarn and fabrics) have risen significantly during March-June, 2022 period. However, brands, retailers and buyers have been able to pass on a large part of this on to producers and exporters in Bangladesh. This once again reinforces the argument for taking steps to raise bargaining power of Bangladesh's concerned stakeholders and strengthen the forward linkage of export-oriented RMG industry of the country.

REMITTANCE FLOWS: The growth of remittance flows during the July-November period of FY2023 was only 2.6 per cent (over the corresponding period of FY2022) which does not match the significantly high number of migrant workers who left for overseas jobs in the recent past months. Bangladesh Bank's supportive policies (higher exchange rate, 2.5 per cent cash incentives, waiver of bank charges, allowing higher forex retention, etc.) did not produce the expected results.

Between January 2021 and October 2022 more than 1.56 million people have left Bangladesh for overseas job markets. There has also been no sign of unusually large number of returnee migrants. Thus, this outflow has no doubt led to an increase in the size of stock of migrant workers in concerned destination countries. A large part of these workers (about 1.3 million or more than four-fifths) went to countries in the Middle-East. Surprisingly, in spite of high migrant flows, remittances came down significantly from some Middle-East countries in the first five months of FY2023 compared to the corresponding period of FY2021-22. For example, although more than a million people have gone to Saudi Arabia over the last 18 months, remittances from the country came down by about USD 462.0 million in the first five months of FY2023 compared to the corresponding period of FY2022. On the other hand, remittance from Kuwait rose by USD 448.7 million over the same period although the corresponding number of migrant workers was only about 17 thousand (Table 3).

There is a need for a deeper investigation as regards the factors driving the fall in remittance flows from particular countries in the Middle East (e.g. Saudi Arabia, UAE) while this was not the case for other countries in the region (e.g. Kuwait). In all likelihood, the significant difference between formal and informal (hundi/howla) exchange rates may have created an added incentive for the diversion of remittance flows from formal to informal channels which indicates that in certain countries hundi/howla syndicates remain very active and they are taking advantage of the exchange rate differences.

It is to be noted that the recent changes in the exchange rate for remittances (BDT 107 per USD plus the 2.5 per cent cash incentive) have significantly reduced the margin between formal exchange rate and the curb market rate in Bangladesh. To what extent the difference in the rates between the formal and informal hundi/howla market rates still persists remains an issue for speculation, although the margin must have reduced significantly in recent times.

Bangladesh Bank will need to keep the emergent scenario under constant monitoring and vigilance and both exchange rate management and enforcement of relevant laws particularly against hundi/howla syndicates will be critically important in this regard.

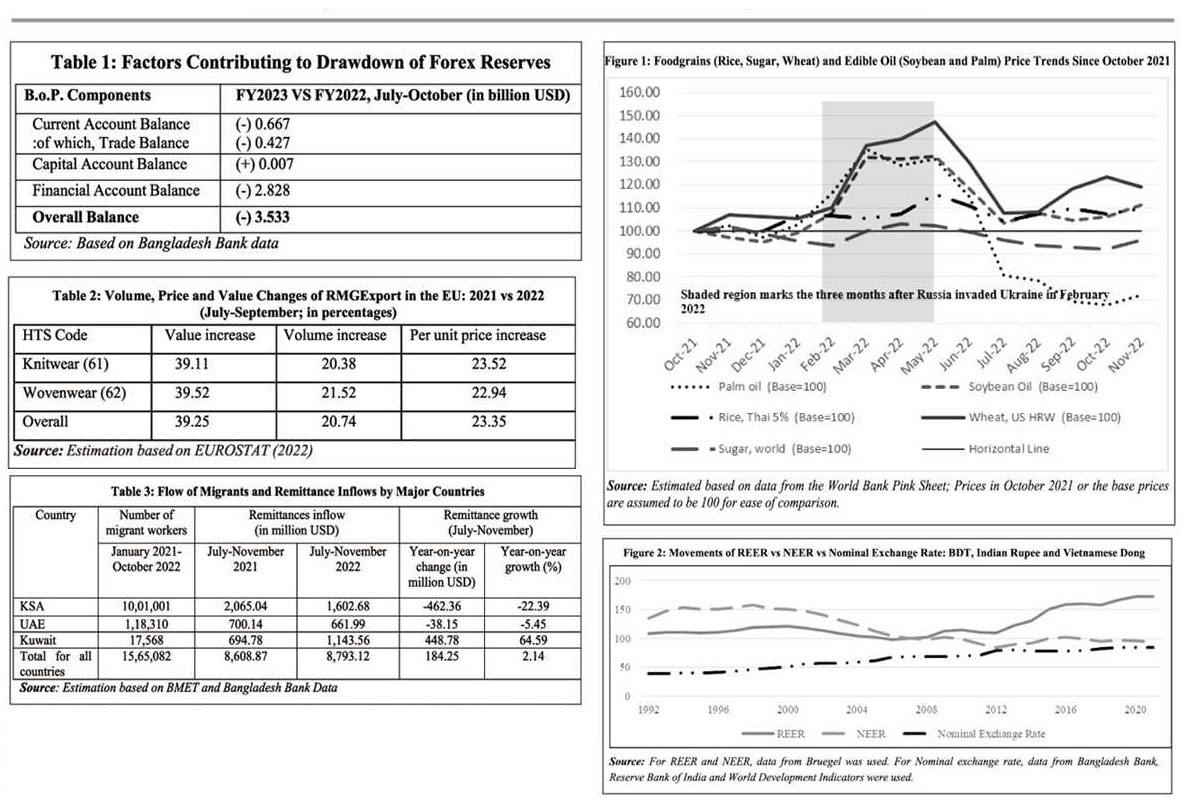

MIXED SIGNALS AND A SILVER LINING--Reduced Import Payments: The recent policy of reining-in imports through various tools, pursued by the GoB and the Bangladesh Bank, appears to be paying off. While L/C settlement during Q1 (July-September) of FY2023 rose by 31.6 per cent (an increase of about USD5.39 billion), compared to the corresponding period of FY2022, L/C opening had come down by (-) 8.6 per cent (a drop of USD1.72 billion) compared to the corresponding period of the previous year. One can infer from this that L/C settlement in Q2 of FY2023 is likely to come down significantly, with lower import payments and consequently an easing of the pressure on forex reserves may be expected. Demand-side impact on imports, induced by higher global price and depreciation-induced price rise, are some of the other reasons. However, lower import will have adverse implications for domestic production and export-oriented activities as a part of this is driven by lack of access to foreign currency to underwrite import L/Cs. On the other hand, exports are likely to be negatively impacted by recessionary trends in major destination countries, although remittances are expected to rise in the backdrop of recent refixation of exchange rate for remittance flows.

The silver lining is that the global prices appear to have peaked already, and are now coming down from the high of April-June, 2022 (Figure 1). This is evidenced by global price trends of some of the key commodities such as fuel, fertiliser, edible oil and sugar and important inputs such as cotton for which Bangladesh is highly dependent on imports. It is anticipated that thanks to this the pressure on import payments is likely to ease in the near-term future. The exchange rate depreciation-induced high prices will also have a demand-side impact resulting in lower import payments depending on the nature of the particular item and respective demand elasticity. However, it should also be kept in mind that import restrictions and lower imports will have adverse implications for production-related activities in the economy and for near-term economic growth prospects.

EXCHANGE RATE MOVEMENTS: Following the depreciation of the BDT vis-à-vis major currencies, the Real Effective Exchange Rate (REER) and Nominal Effective Exchange Rate (NEER) of the BDT is likely to have changed in recent times. As can be seen from Figure 2, the REER of BDT has appreciated significantly over the past few years, particularly between 2012 and 2021. This resulted in the undermining of Bangladesh's export competitiveness compared to key competitors and had created a disincentive for remittance senders. For example, BDT's REER was significantly higher relative to those of the currencies of India and Vietnam (compared to the base year of 2010).

Thanks to recent significant depreciation of the BDT, the difference between BDT's NEER has come down with some of the competitor countries such as Vietnam and India. The exchange rate movement indicates that the rising and substantial discrepancy between the REER, NEER, and NER of BDT appears to have narrowed down in recent times. It appears that BDT's NER is closing the gap with what the exchange rate would be had it been market-determined (Figure 2).

It is reckoned that time has come for Bangladesh to shift from managed float to a free float regime. This will necessitate dealing with the issue of imported inflation through better coordination of monetary and fiscal policies, strengthening of social safety net programmes, extension of open market operations and, if required, through introduction of targeted rationing.

As is known, after more than a decade, Bangladesh has asked for a balance of payment support of USD 4.5 billion from the IMF. As was noted earlier, whilst global factors, particularly rising prices were key reasons driving the current B.o.P. anxieties, these should be seen more of as 'accentuating drivers' and not as much as exclusively 'explanatory factors'. One of the key underlying causes was associated with exchange rate management that ignored calls for gradual depreciation of the BDT which was recommended by experts for the past several years. Bangladesh's policymakers will need to learn from the recent experience and draw necessary lessons for future policymaking.

GOING FORWARD: Bangladesh Bank will need to fully exercise its rights and responsibilities as an institution mandated to oversee management of the monetary sector of the country. The erosion of its autonomy and authority in this regard, seen in recent past years, must be reversed. The demands on the quality of macroeconomic and monetary management will need to be raised considerably over the near-term future.

No doubt, the key to robust external sector performance lies in the efficacy and good governance in overall macroeconomic management. Particularly in view of Bangladesh's upcoming graduation from the Least Developed Country (LDC) status, with consequent significant preference erosion, the transition from preferential market access-induced competitiveness to skills and productivity-induced competitiveness must be given highest importance. Concrete steps towards export and market diversification, greater regional integration and triangulation of trade, investment and transport connectivities and development of value chains and production networks must be given priority in policymaking. The state of the country's external sector performance and B.o.P. position will critically hinge on this.

Middle-income transition and the consequent rise in costs of borrowings should also be an important consideration in view of external sector management. Servicing of foreign debt, till now comfortably managed, could add new dimensions to the emerging challenges in connection with reserves management, particularly in the backdrop of maturing of some of the hard term loans of the recent past. The growing private sector foreign loan, currently standing at about USD 25.0 billion and about 70.0 per cent of which will be maturing in about a year, while not backed by sovereign national guarantee but by the banks, has added a new dimension to the debt discourse. In this backdrop, the demand for foreign currency in the market will rise, with ramifications for exchange rate movements. These newly emerging concerns should be factored into the country's exchange rate management, particularly also because the share of non-concessional loans is set to rise in the loans portfolio of Bangladesh because of the country's middle income graduation.

The depreciation of BDT will also have important implications for debt servicing, both in case of public and private debts, more specifically for loans taken to underwrite projects that generate revenue in local currency (e.g. energy projects). Foreign exchange liabilities as also economic, internal and financial rates of returns should be re-estimated in view of this, and business plans revisited, to ensure proper debt servicing.

As is known, the IMF has come up with a number of suggestions as regards management of exchange rate, forex reserves and overall monetary sector; it has also underscored the need for data transparency. These call for serious attention and urgent decision by policymakers. As was noted, the need for many of these policy initiatives and actions were pointed out by experts for quite some time now. Reforms and measures in view of these must be subject to open and participatory debate and discussion, keeping in the perspective both short-term needs of the economy and the medium to long-term strategic interests of the country, keeping in the perspective the attendant trade-offs.

Dr Fahmida Khatun is Executive Director, Centre for Policy Dialogue (CPD); Professor Mustafizur Rahman, Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem, Research Director, CPD; Towfiqul Islam Khan, Senior Research Fellow, CPD; Muntaseer Kamal and Mr Syed Yusuf Saadat, Research Fellows, CPD. towfiq.khan@gmail.com, muntaseer@cpd.org.bd.

© 2026 - All Rights with The Financial Express