Even in the very recent past Bangladesh was hailed as a great success story for achieving rapid economic growth and raising millions of people out of poverty. A World Bank (WB) report published in last October wrote, "From being one of the poorest nations at birth in 1971, Bangladesh reached lower-middle income status in 2015. It is on track to graduate from the UN's Least Developed Countries (LDC) list in 2026."

The report then further lauding Bangladesh's economic achievements said, "Bangladesh has an inspiring story of growth and development, aspiring to be an upper -middle income country by 2031." In fact, Bangladesh aspires to become a developed, prosperous and higher-income country by 2041. The IMF has assured its continuing support to achieve this aspiration.

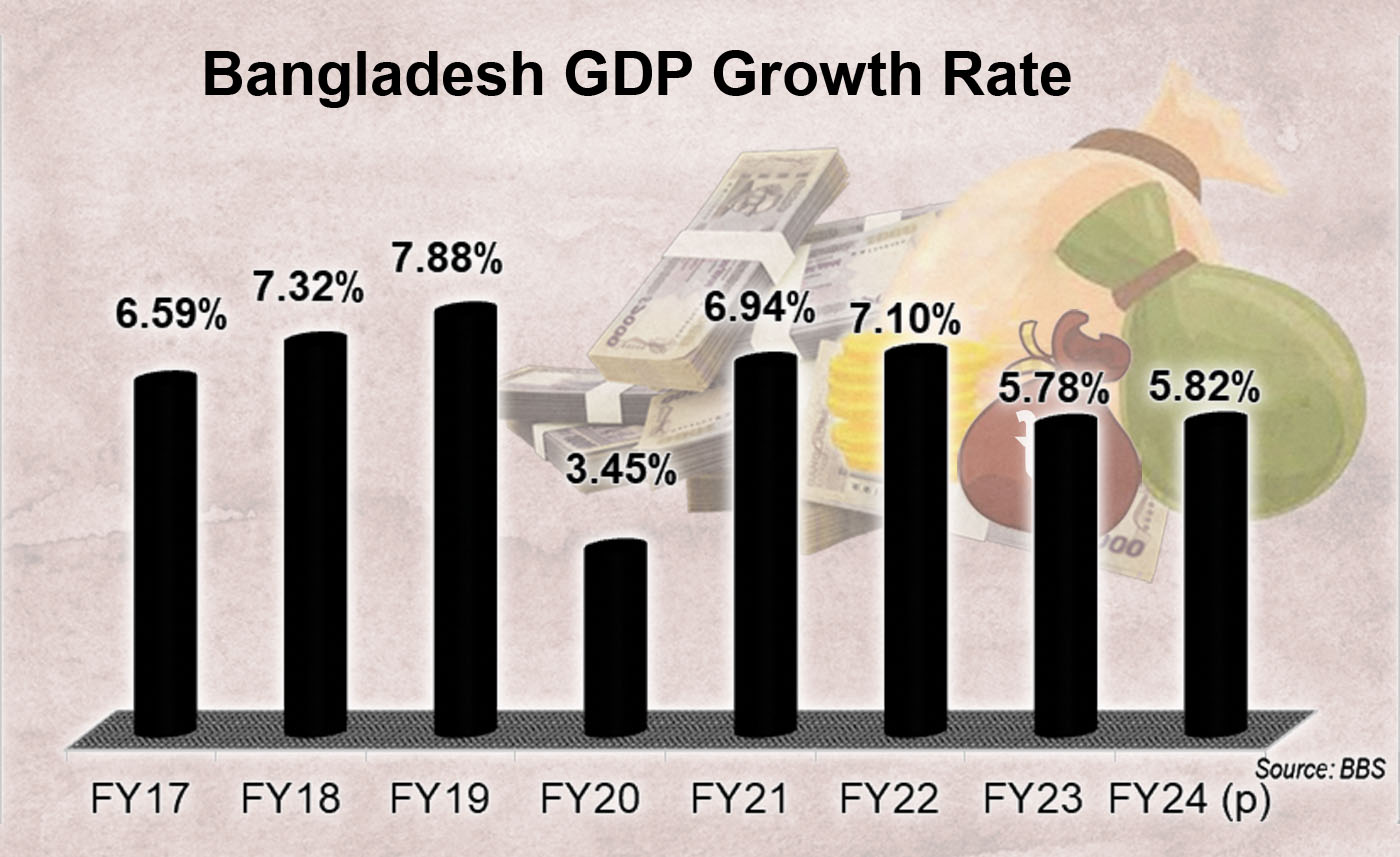

Recent data published by the Bangladesh Bureau of Statistics (BBS) reveal a bleak trajectory for the economy unravelling the country's hard earned economic gains. Bangladesh has gone from an economic miracle to needing help from the International Monetary Fund (IMF). The country's hard-won economic optimism is now being sorely tested.

The economy is faltering. Now there is a growing fear that the much-admired economic growth model of Bangladesh has got unstuck and falling short of expectations. But it just did not happen all on a sudden; it has been in the making for quite some time. The Economist on March 1 last year published an article titled "Bangladesh's economic miracle is in jeopardy" providing a critical analysis of what has gone wrong with the economy.

In fact, the economy is facing challenges at multiple fronts such as rising inflation, balance of payment deficit along with budget deficit, declining foreign exchange reserves, contraction in remittances, a depreciating currency, rising income inequality and the demand supply imbalance in the energy sector. Now added to these challenges is the fragile banking sector crippled by loan defaults. Above all, Bangladesh is particularly vulnerable to the effects of climate change.

The World Bank (WB) recently downsised the GDP growth forecast for Bangladesh by 0.1 percentage point to 5.7 per cent for the next fiscal year, 2024-25. The global lender also said high inflation, food and fuel shortages, import restrictions, and financial sector vulnerabilities weighed on the economic outlook.

With inflation hovering around 10 per cent with food price inflation at around 10.5 per cent annually, the country is now in the grip of a cost-of-living crisis. But many consider that the figure is an underestimate, the real figure is much higher. It is not uncommon for governments to choose the method to estimate inflation that suits them well.

While inflation has put a squeeze on private consumption, public consumption continues to expand, now accounting for 13.02 per cent of GDP. Rising inflation is also contributing to the higher cost of production which is further fuelling inflation. The inflationary surge was largely driven by rising food and fuel prices and the depreciation of the taka.

Bangladesh Bank adopted a contractionary monetary policy to stem the rising inflationary pressure. However, monetary policy transmission mechanism is impaired by regulations on lending interest rates by commercial banks. Also, private sector credit growth remains sluggish making the policy rate less effective.

The banking industry in the country is currently undergoing intense instability due the massive accumulation of non-performing loans and continues to face tight liquidity conditions.The banking industry also suffered a major setback in 2022 when 11 banks faced a collective shortfall of US$ 3.1 billion. The recent bank merger proposals further added to the speculation about the stability of the banking sector. Any further increased instability in the banking sector can lead to a crisis of confidence and that rapidly will move to the broader financial system. This will have serious consequences for the economy.

Industrial output growth has slowed down due to stagnant private investment, import restrictions on inputs and higher energy costs. Over the last decade or so, the private investment/GDP ratio remained at around 20 per cent. This was caused by tight liquidity conditions, rising interest rates, import restrictions, and increased input costs stemming from rising energy prices.

Foreign direct investment (FDI) also remains at a very low level at around 2 per cent of GDP. The industrial sector experienced a decline of 3.7 per cent in output growth in 2023-24. The picture is not very different in the services sector. Together these two sectors account for 87 per cent of GDP.

Corruption, bureaucratic delays, often a confusing foreign exchange regime and a complex regulatory regime have created a negative perception among foreign investors. A report published by the United Nations Conference on Trade and Development (UNCTAD) in 2021 said, "Despite steady economic growth in the country over the past decade, FDI has been comparatively low in Bangladesh compared to regional peers. Bangladesh suffers from a negative image: The country is seen as being extremely poor, underdeveloped, subject to devastating natural disasters and sociopolitical instability."

Furthermore, the Industrial sector is marked by the high concentration risk from an over reliance on the readymade garments (RMG) industry accounting for about 10 per cent of GDP and 85 per cent of exports. Bangladesh is the third largest exporter of RMG in the world. While the government appears to be aware of the need for diversification of the export basket, nothing much seems to have happened.

Bangladesh is not only running a deficit on the current account but in the financial account as well in its balance of payments. If the financial account becomes negative, it creates further pressures on foreign exchange reserve. The very low level of FDI inflow is further adding to the problem. It is to be noted that a financial account measures the increase or decrease in a country's ownership of international assets.

As balance of payments difficulties intensify, the scope for monetary policy actions become increasingly constrained by the need to protect foreign currency reserves. Bangladesh Bank is tightening its grip on import flows as the reserves decline. In fact, trying to address the reserve problem via import controls can lead to problems somewhere else such as growth, inflation and revenue collection.

Furthermore, Bangladesh's imminent graduation from least developed country status in 2026 will affect its preferential market access for exports, especially RMG exports. With low trade diversification, this will create further problems for the country's exports.

The current foreign exchange reserve is estimated to be about US$20 billion. Continuing balance of payments difficulties and an overreliance on remittances have exposed the economy to external shocks.

Very early this month Bangladesh Bank detected "accounting anomalies" in exports data for the first ten month of fiscal year 2023-24 which resulted in US$13.8 billion reduction in exports revenue. According to the Financial Express (July 12), about US$20 billion shortfall in export revenue has been detected by the Export Promotion Bureau for the last two fiscal years.

This further highlights the long-standing concerns of the country's leading economists about the reliability of published data by various government institutions including the Bangladesh Bureau of Statistics (BBS). Reliance on unreliable data can lead to worrying distortions in governments' policy planning.

Bangladesh also runs a budget deficit which stands at 4.6 per cent of GDP for the fiscal year 2024-25. Almost two-thirds of public revenue is derived from indirect taxes and a third from direct taxes. Reliance on indirect taxes, especially consumption taxes, are viewed as regressive. Such taxes not only negatively affect income redistribution via the taxation system but also further erode consumer purchasing power in periods of high inflation as is the case now in Bangladesh.

Many economists believe that a budget deficit leads to current account deficit. In macroeconomics it is known as the twin deficit hypothesis. The twin deficit problem will make Bangladesh a debtor to the rest of the world and will weaken the value of the taka, thereby further aggravating external imbalances.

Overall, to address these economic challenges Bangladesh needs to build enhanced state capacity and reorient its economic policy approach by embarking on a new phase of structural transformation. This structural transformation will focus on innovation by harnessing the new technological frontiers using skilled labour with an increased emphasis on stimulating investment including FDI. Such a reorientation of economic policy will help the country to accelerate recovery and strengthen its capacity to withstand future shocks, therefore, enabling the country to achieve sustainable economic growth and development in the long run.

muhammad.mahmood47@gmail.com

© 2026 - All Rights with The Financial Express