Abdullah A Dewan and Dewan Tahmid | October 04, 2023 12:00:00

The main news article on September 30 in FE stated: “Inflation in Bangladesh seems inexplicable with prices stubbornly staying manifold over production costs while it eases worldwide, a situation which some economists describe as ‘greedflation’ created by profiteers.” An alternative term for “greedflation” is known as “market failure” – one that arises due to supply and demand mismatch brought about by non-market forces. Greedflation – if it exists –is nonetheless ephemeral and cannot steer a country wide inflation pressure on all goods and services. This article explores an alternative explanation – an adverse supply shock driven stagflation – one in which the economy experiences increasing inflation accompanied by slowing real GDP growth and increasing unemployment rate.

Annual inflation rate in Bangladesh rose to 9.9 per cent in August 2023, from 9.7 per cent in the previous month. The US Inflation Rate is at 3.67 per cent compared to 3.18 per cent last month and 8.26 per cent last year. Inflations in the Eurozone came down to a two year low of 4.3 per cent. The free market dynamics in these countries are not comparable to the macroeconomic governance of Bangladesh. The central Bank’s monetary policy independence plays a big role in inflation management. Since 2012, the U.S. Federal Reserve has set a 2.0 per cent inflation target rate for the US economy and resorted to monetary policy activism, if inflation exceeded the target rate.

Annual inflation rate in Bangladesh rose to 9.9 per cent in August 2023, from 9.7 per cent in the previous month. The US Inflation Rate is at 3.67 per cent compared to 3.18 per cent last month and 8.26 per cent last year. Inflations in the Eurozone came down to a two year low of 4.3 per cent. The free market dynamics in these countries are not comparable to the macroeconomic governance of Bangladesh. The central Bank’s monetary policy independence plays a big role in inflation management. Since 2012, the U.S. Federal Reserve has set a 2.0 per cent inflation target rate for the US economy and resorted to monetary policy activism, if inflation exceeded the target rate.

To tame inflation and reverse its upward trend, the Bangladesh Bank (BB) adopted a hawkish policy to increase interest rate based on a moving average rate on 6 months Treasury bill plus 3.0 per cent premium. For example, if the average yield on Treasury bill is say, 6.0 per cent, then the landing rate by commercial banks cannot increase more than 9. The rate is subject to revision at the end of every month. One wonders what inflation target BB wants to hit – if there is one - that will convince BB to end its hawkish policy and may even begin slashing interest rate downward.

We next wonder— what is the basis of BB’s aggressive rate hike policy? If inflation is demand-driven, then hiking interest rate is traditionally the right course of activism. If the sources of inflation, on the other hand, are predominantly supply factors driven, then successive interest rate hikes may potentially worsen both inflation and employment – a calamitous outcome of stagflation.

With the Covid-19 pandemic-driven supply chain disruptions and post pandemic slow recovery of the global economy muddle through supply chain bottlenecks, inflation became an economic pandemic globally. Then came the throttling sanctions on the Russian economy which added additional momentum to the already brewing inflation. Developing economies’ currencies and foreign exchange reserves were hit hard. The confluence of factors further worsened domestic inflation due to higher prices of imported factors of production (such as industrial machinery and parts, chemicals, energy products and so on). In economic jargons these factors are called supply side factors which collectively affect the Aggregate Supply (AS) curve. A country’s monetary authority has little or no control over the supply side of the economy.

The economy’s health gets worse compounded if capital flight intrudes into the inflation equation. For any developing country, capital flight is an opportunity lost for foreign currencies to work for domestic economic expansion through imports of capital goods such as machinery and parts etc. Capital flight can dry up a country’s ability to finance both public and private investments. Other adverse outcomes of capital flight include the erosion of a country’s tax base creating a distorted income dilemma, and the dissuasion of foreign direct investment. All these adversities affect the AS function to shift leftward causing cost push inflation.

If the sources of inflation are diagnosed as supply factors steered, then higher interest rate policy will act counter to inflation taming/reversing policy. Businesses are already paying higher prices for imports and now at home are borrowing domestic funds at a higher interest cost. Therefore, a hawkish interest rate policy will only exacerbate the menace of inflation. What if the source of inflation is in part due to capital flight causing a dwindling state of foreign currency reserves and domestic currency losing its value against the USD, and other hard currencies, the policy may turn out to be an abject blunder. Therefore, knowing the sources of inflation is paramount for an effective policy outcome. No wonder, the Federal Reserve runs two super computers non-stop and employs an army of 400 plus Ph.D. economists who are analysing a myriad of economic issues by inputting data from the global economy.

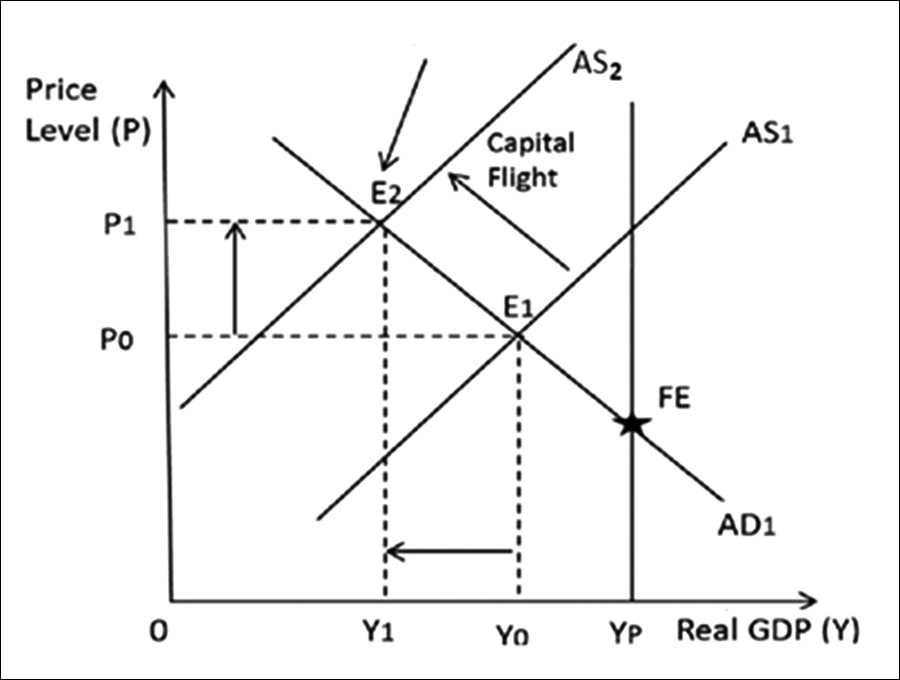

Every government knows the mechanism how capital flight occurs. Anti-capital flight laws are in place in every country. But the enforcement of the laws in most countries is relaxed and lacking. Everyday departing flight from Dhaka airport not only carries passengers and their luggage, but the plane also carries a hefty amount of USD. There is no check at the airport on the limit of how much foreign currency can a person legally carry. The effect of such capital flight is analysed here using the Aggregate Demand (AD) and Aggregate Supply (AS) model.

The macroeconomic equilibrium is determined by the interactions of both AD and AS. While AD can be influenced by monetary and fiscal policies, AS is a function of the factors of production such as prices of inputs (labor, capital, energy etc.), availability of labour and capital and their corresponding productivities, the level of technology, and so on. Any large change in any of the supply factors, referred to as supply shock, shifts the AS function leftward or rightward, depending on the shock being negative (unfavorable) or positive (favourable).

AD = f(C, I, G, X – M)

where C = Consumption spending, I = Investment spending, G= Government spending, (X - M) = exports - imports (net export).

AS = f(L, K, T, energy products, and other inputs)

Where L= Labor, K = Physical Capital, T = Technology

For faster economic growth and poverty reduction, a country must attract multinational corporations to invest in building factories and enterprises (foreign direct investment, FDI). Unfortunately though, factors that encourage capital flight are some of the same factors often deter FDI. Under such a manifestation of double jeopardy, the country’s production capacity is likely to be impacted negatively by lack of equipment and parts and the replacement of depreciated capital goods because of potential foreign currency constraints. This will take a toll on the productivity of labour (through a lower capital-labor ratio – implied by the famous Cobb-Douglas Production Function. If the double jeopardy persists, and assuming AD remains virtually unchanged, one expects a leftward shift of the AS function, derailing the economy into a new equilibrium with stagflation, which is a phenomenon of the simultaneous occurrence of declining output (higher unemployment) and high inflation, as shown in the figure.

Referring to the Figure: YP = Potential real GDP when all available resources are fully and efficiently employed. Y0 = equilibrium real GDP below full employment equilibrium (some resources are laying idle).

For Bangladesh economy, the output at Y0 (corresponding to equilibrium at E1) implies that the economy is producing at less than its full potential (YP) because of political instability (strikes and lockouts), endemic corruption, weak enforcement of rule of law (ill governance), and so on. With unabated capital flight added to these factors, the AS function shifts to AS2 with a new equilibrium at E2 (stagflation). By striving hard to ameliorate the factors of capital flight alone, Bangladesh can achieve output growth at or close to the potential level YP, with the AS function shifting rightward to full employment equilibrium at FE. This will allow output growth well beyond the 4.5 per cent average growth of yesteryears, and inflation well below the average annual rate of 5.5 percent.

An episode of stagflation is a policy makers’ worst nightmare since attempts to ameliorate one - controlling inflation - by using monetary and fiscal policies worsens unemployment and GDP growth and vice versa.

Dr Abdullah A Dewan, formerly a physicist and a nuclear engineer at BAEC, is Professor of Economics at Eastern Michigan University, USA.adewan@emich.edu. Dewan Tahmid is an

economist (M.S.S), and a fellow of Teach for Bangladesh, doing M.Ed., at BRAC University, Dhaka. dtahmid71@gmail.com.

We thank Dr. Habibur Rahman, Chief Economist, Bangladesh Bank, for giving his insights about the macroeconomic issues of Bangladesh.

© 2026 - All Rights with The Financial Express