With enhanced access to digital financial products and services, the Mobile Financial Services (MFS) industry in Bangladesh is expanding every year. In July 2022, there were over 181 million accounts held with 13 MFS providers in Bangladesh, a 16 per cent increase over the previous year. MFS-enhanced financial inclusion and transactions has had a substantial impact on Bangladesh's economy and financial activities, particularly during and after the COVID-19 Pandemic.

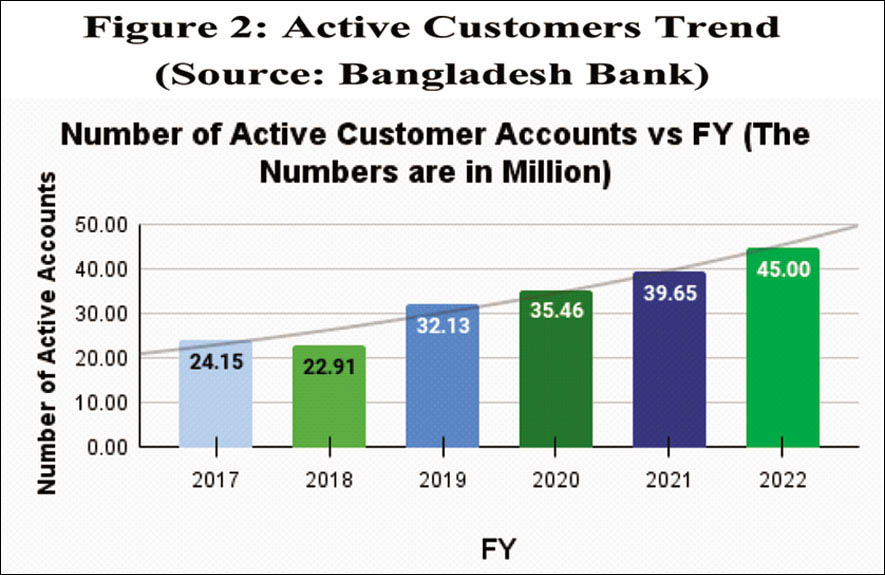

The Bangladesh Bank has been awarding licences for MFS in an effort to integrate those who do not have bank accounts with the formal financial system. MFS is appealing to government bodies due to its multi-dimensional impacts as well as revenue-generating methods. Since the industry's inception, the growth of the MFS sector has been positively influenced by a number of factors, including the tech-savvy population, mobile connectivity, and internet penetration.  Figure 2). This dramatic growth in clientele has allowed MFS to expand its product offerings and better meet the needs of its customers. Given the bright picture, one could presume that the firms in this industry are flourishing generating a sustainable profit.

Figure 2). This dramatic growth in clientele has allowed MFS to expand its product offerings and better meet the needs of its customers. Given the bright picture, one could presume that the firms in this industry are flourishing generating a sustainable profit.

However, considering their recent financial performances, the question is whether all these companies will be able to sustain themselves over the long term. If we take a look at the recent past performance of the country's largest MFS provider bKash, we can see that the company has been operating at loss for the past three years, with losses of BDT 625 million in 2019, BDT 814 million in 2020, and BDT 1,234.2 million in 2021. The question is, after incurring losses, spending a lot on customer acquisition, and making heavy investments in technology, will the company survive or not? When questioned why the companies have been incurring losses, they try to defend themselves by mentioning they are investing in new technology and solutions to meet rising demand, affecting their profitability. In their annual reports and press briefing, bKash officials said that the problems the customers are facing, such as fraudulence, server issues, cyber-crime, account hacks etc., have become a major concern of bKash, and they are trying to solve these issues. They are establishing strong AML/CFT so that the customers can feel safer and get more secure service. With a few notable exceptions, most of the other MFS show a picture that is similar to this one.

Without doubt, the two most significant players in the MFS sector are bKash and Nagad. Both of these firms provide a wide range of services to their clientele. When looking at their position in the market, it should be noted that more than 60 per cent of all MFS transactions in the country have been performed through bKash and that more than 70 per cent of all active clients have accounts with bKash. Even the revenue statistics of the industry highlights that bkash has more than70 per cent of sector revenue. Hence, it is clearly apparent that other MFS like Rocket, SureCash, MCash, and Upay, amongst others, are still struggling to maintain an important position in the sector. If the situation continues in this manner, some small players will soon be out of business. More importantly, it makes you ask why others are not succeeding and where the problem is.

The current competitive environment of the MFS industry seems to be monopolistic or oligopolistic. This type of competitive environment is never advantageous to the industry players and creates obstacles for both existing players and newcomers. It is important to highlight the powerful influence that bKash has in the market. Is it right time to induce "Significant Market Power" guideline for the MFS industry? We have seen a precedent in Bangladesh before, where SMP was imposed on Grameen Phone in the year 2020 by the government agency that regulates telecom companies. Hence, the situation needs Central Bank's attention. Furthermore, the adoption of SMP guidelines for MFS industry could prove to be beneficial in ensuring that no one or two players monopolise the entire market. The implementation of SMP will not only assist in the continuation of small players' operations but will also open up prospects for newcomers. The main intention of SMP guidelines is to enhance market competition. A merger could be the best option in the event SMP is not the optimal solution or if government authorities want oligopolistic competition in the MFS market. Again, businesses that are falling behind the competition may need a diagnostic to determine why this is the case, including what customers have come to anticipate from them.

Rubaba Tahasin, MBA graduate, Brac Business School, Brac University,rubaba.

tahasin.tammi@g.bracu.ac.bd

Dr. Mohammad Enamul Hoque, Assistant Professor at Brac Business School, Brac University.

enamul.hoque@bracu.ac.bd