'Forensic accounting' utilises accounting, auditing, and investigative skills to conduct an examination into a company's financial statements. Thus, it provides an accounting analysis that is suitable for decision-making by a court or the management. Forensic accountants are trained to look beyond the numbers and deal with the business reality of a situation. They are frequently used in fraud cases.

There are two big pillars of forensic accounting:

LITIGATION SUPPORT: It provides assistance of an accounting nature in a matter involving existing or pending litigation. It deals primarily with issues related to the quantification of economic damages. A typical litigation support assignment would be calculating the economic loss resulting from a breach of contract.

INVESTIGATIVE ACCOUNTING: It is often associated with investigations of financial frauds. A typical investigative accounting assignment would be an investigation of occupational fraud. Other examples include securities fraud, insurance fraud etc.

FORENSIC ACCOUNTANT: He is someone who is applying financial skills and an investigative mentality to unresolved issues, conducted within the context of the rules of evidence.

Forensic accountant needs to be the bloodhounds of accounting and not the watchdogs. Forensic accountants should be cautious of obvious things and wary of persons who are quick to provide alibis and identification. Forensic accountants should demand verification whenever possible as the evidence that a forensic accountants require is required to be conclusive.

Forensic accountants should develop their own curiosity and follow up on it. They should have the desire to learn the truth. An inquisitive mind is essential to the forensic accounting professionals.

Forensic accountant should respect the confidentiality of information acquired as a result of professional and business relationships and should not disclose any such information to third party without proper authority.

The ability to recall accurately the facts, events and the physical characteristics of a suspect is a valuable skill every time everything can not be documented unlike the auditors.

A fraudster can cause harm during investigations. Forensic accountants should not form opinions about any one unless there is conclusive evidence. Bias and prejudice will result in a poor investigation, unfairness to suspects, and clouding of facts that need to be uncovered objectively. Do not let personal likes or dislikes interfere with investigations.

A forensic accountant is often retained to analyse, interpret, summarise and present complex financial and business related issues in a manner which is both understandable and properly supported. He can be engaged in public practice or employed by insurance companies, banks, police forces, government agencies and other organisations.

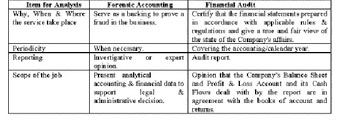

COMPARISON OF FORENSIC ACCOUNTING AND FINANCIAL AUDIT:

The writer is a chartered accountant is chief financial officer of a private life insurance company. chandrashekhar_cfo@pragatilife.com.

© 2026 - All Rights with The Financial Express