Fahmida Khatun, Mustafizur Rahman, Khondaker Golam Moazzem, and Towfiqul Islam Khan | February 17, 2021 00:00:00

Halfway through the fiscal year 2020-21 (FY21), the Bangladesh economy is still reeling from the adverse consequences of the ongoing Covid-19 pandemic as manifested by key macroeconomic and sectoral performance indicators. Although, in terms of Gross Domestic Product (GDP), Bangladesh was an outlier as one of the very few countries which posted positive growth rates in 2020, there are reasons for concern as one examines the underlying factors that informed economic performance as the country moves towards the end of FY21. The key question here is: whether the economy has been able to overcome the initial stress, make a turnaround and is set on the course for rebound and recovery.

The objectives of the present review carried out under the Centre for Policy Dialogue (CPD)'s flagship Independent Review of Bangladesh's Development (IRBD) are threefold. First, to have a conceptual understanding about how to define economic recovery in the backdrop of adverse impacts on an economy. Second, taking cue from the above, to analyse the performance of Bangladesh economy, as it crosses the midway mark of FY2021, to assess to what extent macro and key sectoral performance indicators have fared from the vantage point of turnaround, rebound and sustainable recovery. Third, to offer suggestions to address some of the important attendant concerns associated with the selected areas of analysis.

The objectives of the present review carried out under the Centre for Policy Dialogue (CPD)'s flagship Independent Review of Bangladesh's Development (IRBD) are threefold. First, to have a conceptual understanding about how to define economic recovery in the backdrop of adverse impacts on an economy. Second, taking cue from the above, to analyse the performance of Bangladesh economy, as it crosses the midway mark of FY2021, to assess to what extent macro and key sectoral performance indicators have fared from the vantage point of turnaround, rebound and sustainable recovery. Third, to offer suggestions to address some of the important attendant concerns associated with the selected areas of analysis.

CONTEXT: The global economy has been gravely affected by the Covid-19 pandemic. Nearly a year after the pandemic had first made its presence known, the global economy is perhaps showing some signs of economic recovery. Global economic output is projected to increase by 4.0 per cent in 2021 even though the growth rate is 5.0 per cent below pre-pandemic estimates, according to the World Bank. However, the recovery is expected to be uneven across the world as some economies will regain output faster than others depending on the extent of the loss and their capacity to recover. Developed countries (3.1 per cent) are expected to experience a slower pace of recovery compared to developing countries (5.7 per cent). This has significant implications for many economies including Bangladesh. The growth outcomes in China, the European Union and the United States directly affect the South Asian countries through impacts on export demand, remittances and access to foreign financing. For example, nearly 62 per cent of the ready-made garments (RMG) exports from Bangladesh go to European markets. Consequently, recovery of any particular country is not only dependent on the strength of its domestic economy, but also on how the other economies recover.

Moreover, within the country, economic recovery may not follow the same pace and pattern across sectors. Several factors have implications for the recovery of economic sectors including: (i) extent of loss due to the pandemic; (ii) size of the business/firm in terms of investment and returns; (iii) type of policy measures put in place by the concerned government; and (iv) support received from the government. Despite some positive signs, the sustainable recovery route for majority of countries and most sectors is dependent on many factors and remain uncertain. In the course of the recovery, the need for appropriate policy measures is thus of critical importance. Indeed, appropriate policies can expedite recovery in a sustainable manner. Moreover, much of it also depend on the scale and timing of policy responses.

SHAPES OF ECONOMIC RECOVERY FROM RECESSIONS: Currently, there is a lively debate involving experts regarding the shape of economic recovery from recession: K, L, U, V, W and "shoosh" shaped recovery curves. These are discussed in brief.

K-shaped recovery occurs when a segment of the economy pulls out of a recession, while others stagnate. L-shaped crisis represents a permanent loss of output. U-shaped recovery refers to an initial drop, followed by sluggish recovery in output. V-shaped recovery is when an initial drop is followed by a sharp increase in the growth rate. W-shaped or Double-dip recession is defined as "a second decline of real gross domestic product (GDP) after a trough of the economic cycle but prior to the reversion point or the previous peak level of real GDP". In case of a "swoosh" shaped recovery, the output experiences a rapid drop followed by an excruciatingly slow recovery.

Despite the discussion on various shapes of recovery, there is a gap in the literature regarding the definition of economic recoveries. Most of the existing studies have explored the resilience of economies while the recovery aspect as the central focus of research has received little attention. In relevant literature, the most commonly used indicators are quarterly GDP and employment scenario.

Martin and Sunley (2015) suggested that "recovery could mean a return to the peak level of employment, a return to the original growth path, a return to the original growth rate, or the adoption of a new, favourable growth path". Instead of defining recovery as a certain level of employment to be achieved or a return back to a pre-shock trend, Han and Goetz (2015) identified recovery as the rate of employment change in the six months following a region's trough, the rate of employment changes in the six months following the trough of a region. For assessing the resilience of various counties in the USA during and after global financial crisis (GFC), Ringwood, Watson and Lewin (2018) tracked the total employment behaviour during the months from a county's local peak, associated with the beginning of the shock response, to six months after the trough, to include both the magnitude of the impact of the recession locally and the beginning of recovery.

INDICATORS FOR ASSESSING ECONOMIC RECOVERY: A survey of literature reveals that the analysis of economic recovery has incorporated several variables beyond GDP and employment. Barthelemey and Binet (2020) analysed economic recoveries from financial crises using a dataset of 104 emerging and advanced countries covering the period from 1973 to 2017. The authors found that credit growth, real currency appreciation, a declining share of government spending in the GDP and, to a lesser extent, rising liquidity, resurgent inflation or greater trade openness following the crisis were more likely to facilitate substantial recoveries that were V, S or U shaped. Caro (2015) used employment series instead of GDP or other economic measures to analyse economic resilience. Although employment data can be affected by labour market dynamics, the choice of variable was justified on two grounds: (i) employment data are more "articulated" at the regional level and does not require to be deflated, and (ii) they offer interesting insights into the evolution of the geographic context.

Based on a review of a large body of literature, Rose and Krausmann (2013) cited the following indicators for assessing economic and community resilience indices: business size income; equality; avoidance of losses; redundant capacity; stabilising measures; recovery time; household income; property value; employment investments; excess capacity; inventories; input/import substitution; diversity of economic resources; equity of resource; distribution; percent employed; household income; business size; inventories; excess capacity; input substitution; business relocation. The authors concluded that most of the indicators are only applicable to major disasters.

In their analysis of the impact of the great financial crisis (GFC) on the European region, Antoshin et al. (2017) found that a 10 per cent rise in bank credit to the private sector is associated with a 0.6-1 per cent increase in real GDP and 2-2.5 per cent growth in real private investment. Economic recovery in the United States following the GFC showed a rise in household net worth, stock market, investment spending, and a fall in personal savings rate in 2012 (Elwell, 2012). Roberts' (2004) review of post-collapse experiences of Cameroon, Cambodia, Ethiopia, Mozambique, Nicaragua, Rwanda, Uganda and Zambia found that in all but two cases, the first three years of recovery saw positive per capita income growth. The post-collapse rate of recovery is the growth of real final demand - government consumption expenditure, investment expenditure and exports. Due to their inherited macroeconomic and external financial condition, and the need to constrain government spending, Nicaragua and Zambia could not raise their per capita incomes in the immediate post-collapse period.

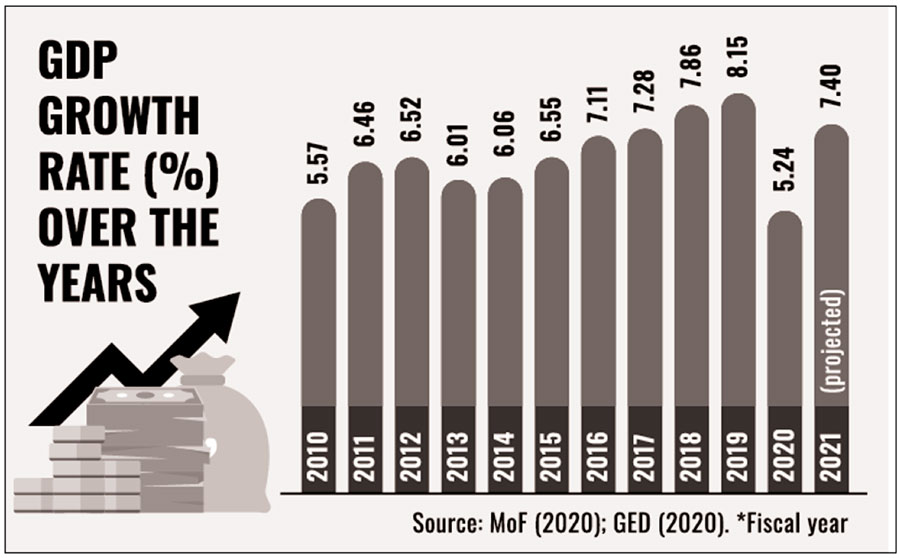

BANGLADESH'S ECONOMIC RECOVERY PATH: According to the official estimates of the government of Bangladesh (GoB), Bangladesh's growth of gross domestic product (GDP) in FY20 was 5.2 per cent. Though this is lower than the projected 8.2 per cent for FY20 and lowest in the last decade (Figure 2.1), Bangladesh's growth during the pandemic is way above all other countries. The economy remained resilient thanks to its domestic strength. High agricultural production, remittances and exports, particularly that of the readymade garments (RMG) have played a crucial role in achieving the growth.

In the current FY21, the government has projected a growth rate of 7.4 per cent. This is very promising and, if achieved, Bangladesh will be an outlier in terms of the pace of recovery of economy, which will be much faster than other countries. However, official estimates of GDP provided by the government have created debates in the country due to its disjuncture with fundamental macroeconomic variables including private sector credit, revenue mobilisation, import payments for capital machineries, energy consumption, export receipts, and employment generation. In fact, the GDP estimates for FY20 have also come under scrutiny mainly due to the significant discrepancy between the GoB numbers and the estimates provided by a number of international organisaitons including the World Bank and International Monetary Fund (IMF). Indeed, the provisional growth figures may as well be revised when the final numbers come out.

The other issue is that even if this growth is achieved, all sectors may not be able to recover in the same way. Globally, the possibility of a K-shaped recovery is being discussed widely. This implies that stimulus packages and liquidity support will help large industries and public organsiaitons recover at a faster pace while the small and medium enterprises (SMEs) will lag behind. Bangladesh is likely to follow a similar shape as smaller firms, people belonging to the low income category and the poor in general have been affected disproportionately and have not received adequate government support. Given that SMEs are important sources of employment, the slow recovery of this sector could lead to further rise in inequality. This could jeopardise the sustainability of the recovery. Therefore, policymakers need to chart out the recovery path in a manner that does not leave out the weaker but critically important sectors of the economy.

However, in the absence of quarterly and disaggregated data on GDP and employment, it is not possible to diagnose economic performance and predict future outcomes in a pragmatic manner. In Bangladesh, quarterly GDP data are not prepared and the publication of the quarterly Labour Force Survey has been suspended for quite some time. Therefore, how the Covid-19 pandemic has affected the economy and how the economy would recover from the pandemic have to be analysed on the basis of macroeconomic variables and proxy indicators. In this backdrop, CPD has made an attempt to assess the current growth trajectory of the economy based on an analysis of performance, trends, levels and pace of growth of key macroeconomic and sectoral indicators. The summary of the analysis will appear in the FE.

Dr Fahmida Khatun is Executive Director, Centre for Policy Dialogue (CPD); Professor Mustafizur Rahman is Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem is Research Director, CPD; and Towfiqul Islam Khan is Senior Research Fellow, CPD.

[Research support was received from: Muntaseer Kamal, Syed Yusuf Saadat, Md. Al-Hasan and Kamruzzaman (Senior Research Associates, CPD); Mr Abu Saleh Md. Shamim Alam Shibly, Mr Tamim Ahmed, Ms Nawshin Nawar and Mr Adib Yaser Ahmed (Research Associates, CPD); and Helen Mashiyat Preoty and S. M. Muhit Chowdhury (Research Interns, CPD)]

© 2026 - All Rights with The Financial Express