coinciding with a period marked by persistent high domestic inflation and some instability in the foreign exchange market. The current monetary policy approach includes several significant reform measures aimed at addressing ongoing economic challenges. These reforms encompass the modernisation of the monetary policy framework, which involves adopting more market-oriented tools and techniques for policy implementation. Additionally, the deregulation of interest rate and exchange rate regimes is intended to enhance market efficiency and flexibility, allowing for a more responsive and adaptive monetary policy. These efforts require effective coordination with fiscal authorities and other relevant entities. The policy formulation process considers the actual economic outcomes of the second half (January-June) of FY24, as well as comprehensive macroeconomic conditions and forecasts for both the global and domestic economies.

coinciding with a period marked by persistent high domestic inflation and some instability in the foreign exchange market. The current monetary policy approach includes several significant reform measures aimed at addressing ongoing economic challenges. These reforms encompass the modernisation of the monetary policy framework, which involves adopting more market-oriented tools and techniques for policy implementation. Additionally, the deregulation of interest rate and exchange rate regimes is intended to enhance market efficiency and flexibility, allowing for a more responsive and adaptive monetary policy. These efforts require effective coordination with fiscal authorities and other relevant entities. The policy formulation process considers the actual economic outcomes of the second half (January-June) of FY24, as well as comprehensive macroeconomic conditions and forecasts for both the global and domestic economies.

This holistic approach ensures the monetary policy is well-aligned with the broader economic context. Furthermore, the policy formulation process incorporates detailed monetary and credit projections, which provide a quantitative foundation for the policy stance. Feedback, suggestions, and guidelines from a diverse range of stakeholders, including financial institutions, industry experts, and economic analysts, are also considered. These contributions are instrumental in refining the monetary policy stance and framing the monetary and credit projections for the first half of FY25.

Bangladesh Bank (BB) implemented several initiatives during the second half of FY24 to contain sustained high inflation. These initiatives included policy interest rate hikes amounting to 200 basis points during FY24 (a cumulative increase of 350 basis points since the start of the tightening cycle in May 2022). Additionally, the policy interest rate corridor was narrowed from ±200 basis points to ±150 basis points, and the practice of devolvement of T-bills and T-bonds on BB was discontinued, considering the multiplier effect of high-powered money on inflation. The SMART-based interest rate capping was scrapped to allow the market to play its due role in determining interest rates. Consequently, the weighted average call money rate rose to 9.08 per cent by June 2024 from 6.06 per cent in June 2023.

Similarly, the interbank average repo rate increased to 8.56 per cent by June 2024, up from 6.16 per cent in June 2023. Furthermore, lending and deposit rates for various financial transactions notably increased in H2FY24, while the interbank call money rate was effectively contained within the Interest Rate Corridor (IRC).

Moreover, consumer credit, a critical indicator of internal demand, saw slower growth of 12.52 per cent year-over-year (YoY) in March 2024, compared to a 21.19 per cent increase in the same month of the previous year. BB's regular foreign currency sales acted as an automatic quantitative tightening mechanism in the money market, significantly absorbing liquidity. The heighten of interest rates across the spectrum led to a softening of money supply and private sector credit growth between January and June 2024. As part of its supply-side intervention to support growth-enhancing activities, BB provided comprehensive support through refinancing and pre-financing lines, ensuring liberal access to low-cost credit for agriculture and rural non-farm sectors, CMSMEs (Cottage, Micro, Small, and Medium Enterprises), import substitution, and export-oriented industries.

During the second half of FY24, Bangladesh Bank (BB) implemented several measures to enhance foreign exchange supply and reduce demand to contain exchange rate pressure. These measures included:

(i) Liberalising NRB Investment Procedures: Simplifying and easing the process for Non Resident Bangladeshis (NRBs) to invest in the country.

(ii) Increasing Interest Rates on Foreign Bonds: To attract more investment, the interest rates for US Dollar Premium Bonds and US Dollar Investment Bonds should be raised.

(iii) Restricting Fund Transfers: Abolishing the fund transfer facility from domestic banking units to offshore banking units.

iv) Allowing BDT Depreciation: Allowing the BDT exchange rate against the USD to depreciate significantly in line with the Real Effective Exchange Rate (REER) Index.

v) Exempting CRR for OBUs: Exempting banks from maintaining the Cash Reserve Ratio (CRR) with BB for their Offshore Banking Units (OBUs).

vi) Permitting Fund Allocation by OBOs: Permitting Offshore Banking Operations (OBOs) to allocate funds to their Domestic Banking Units (DBUs) without restrictions.

vii) Facilitating Foreign Currency Accounts: Facilitating the operations of Private Foreign Currency accounts and Non-Resident Foreign Currency Deposit (NFCD) accounts.

viii) Allowing Private Foreign Currency Accounts: Authorised Dealer (AD) branches of respective banks to open Private Foreign Currency accounts and NFCD accounts in any approved foreign currency.

ix) Implementing a Crawling Peg Exchange Rate System: Introducing a crawling peg exchange rate system to manage abrupt fluctuations in the exchange rate and mitigate inflationary pressure stemming from exchange rate pass-through to inflation.

Furthermore, to enhance the country's foreign exchange reserves and attract foreign investment, the Offshore Banking Act 2024 was enacted to provide a more robust framework for offshore banking activities. These comprehensive measures aimed to stabilise the exchange rate and maintain economic stability amidst challenging global and domestic economic conditions.

Analysing the external sector reveals that export (fob) earnings, a crucial indicator of external demand, declined by 5.9 per cent year-on-year (y-o-y) as per revised data for July-May of FY24. This reduction is mainly due to decreased demand from export destination countries facing high inflation and financial tightening. Meanwhile, customs-based imports (fob), a vital measure of internal demand, dropped significantly by 12.6 per cent y-o-y in the same period. This decline in imports can be attributed to efforts to discourage the import of non-essential and luxury goods, enhanced monitoring mechanisms by Bangladesh Bank (BB) to ensure justified prices for opening Letters of Credit (LCs) and a notable depreciation of the Bangladesh Taka. These factors collectively contributed to the observed negative import growth. These export earnings and import payment trends highlight the broader economic challenges and adjustments within the external sector, influenced by both global economic conditions and domestic policy measures.

During the July-May period of FY24, recent revisions to export data resulted in notable shifts in the balances of the current and financial accounts. The current account recorded a deficit of USD 5.98 billion, down from USD 12.02 billion last year, while the financial account showed a surplus of USD 2.08 billion, lower than the USD 5.52 billion surplus from the previous year. However, the overall balance remained unchanged at a deficit of USD 5.88 billion for July-May FY24, a notable improvement from USD 8.80 billion in the same period last year.

Despite various fiscal and monetary policy measures to contain inflation, it remained persistently above 9.0 per cent for an extended period. Based on Consumer Price Index (CPI) data, the point-to-point inflation rate marginally decreased to 9.72 per cent in June 2024 from 9.74 per cent in June 2023. However, the CPI-based average headline inflation increased to 9.73 per cent in June 2024, up from 9.02 percent in June 2023. During this period, food inflation played a more significant role than non-food inflation in contributing to headline inflation. Furthermore, core inflation (excluding food and fuel) also declined, averaging 7.36 per cent in June 2024 compared to 8.53 per cent in June 2023. This inflationary episode was initially triggered by high inflation expectations, significant depreciation of the BDT against the USD, and disruptions in the domestic supply chain due to some non-economic factors. Over time, inflation became more entrenched due to second-round effects from domestic fuel and energy price adjustments.

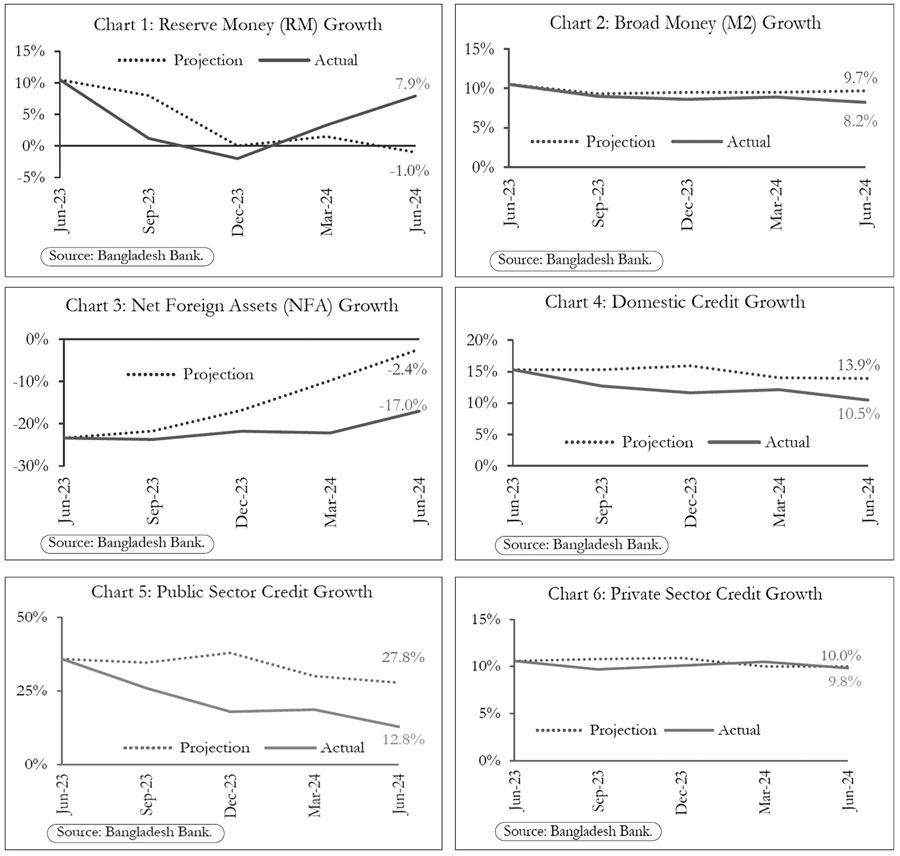

Regarding the monetary landscape, Broad Money (M2), an indicative target of monetary policy, experienced a year-on-year growth of 8.2 percent in June 2024, falling short of the projected 9.7 per cent growth for June 2024. This subdued growth in M2 is primarily attributed to a decline in the net foreign assets (NFA) of the banking system during H2FY24. Specifically, the NFA declined by 17.0 percent in June 2024, a much sharper drop than the projected negative growth of 2.4 per cent for June 2024. This significant decline in NFA was driven by a substantial deficit in the overall balance of payments (BoP).

Reserve Money (RM), another key information variable of monetary policy, increased by 7.9 per cent year-on-year by the end of June 2024, slightly exceeding the projected trajectory for H2FY24. This increase was due to the positive growth in net domestic assets (NDA), which partially offset the substantial negative growth in Bangladesh Bank's NFA. The negative growth in BB's NFA was primarily due to significant foreign currency sales to banks to meet the high demand for USD. In summary, most monetary and credit aggregates followed the expected trajectory during H2FY24. Table 1 and Charts 1-6 illustrate the actual growth paths of key monetary and credit aggregates compared to the projections announced in January 2024 for H2FY24.

During the second half of FY24, the credit growth in both private and public sectors, which reflects the national investment landscape, showed divergent trends. Private sector credit expanded by 9.8 per cent by the end of June 2024, closely aligning with the projected growth rate of 10.0 per cent for June 2024 (Chart 6), despite facing higher borrowing costs due to implementation of contractionary monetary policy as well as tight liquidity conditions. In contrast, public sector credit grew by 12.8 per cent in June 2024, significantly below the projected growth rate of 27.8 per cent for June 2024 (Chart 5). This subdued growth in public sector credit indicates reduced demand from the government, which has been selectively allocating funds to priority projects as part of austerity measures. Overall, domestic credit dynamics in FY24 remained below projections, largely driven by robust growth in private sector credit and moderated expansion in public sector credit (Chart 4).

According to the latest data, the Government's net credit from the banking system in FY24 amounted to Tk. 94,281.8 crore, which is 71.2 per cent of the bank borrowing target of Tk. 1,32,395 crore. During this period, the Government borrowed a net amount of Tk. 1,00,738.5 crore from scheduled banks, while it made a net repayment of Tk. 6,456.7 crore to Bangladesh Bank (BB). With BB ceasing devolvement, the Government's net credit now predominantly relies on scheduled banks. At the end of June 2023, the outstanding amount of the devolved facility stood at Tk. 133,895.85 crore, with around Tk. 52,000 crore already adjusted since the discontinuation of devolvement, indicating that no new money was created by BB to finance government spending.

From July to May of FY24, the outstanding value of National Savings Certificates (NSCs) fell by Tk. -17,743 crore, a significant decline compared to the Tk. 3,029 crore decrease was recorded during the same period in FY23. This drop indicates that repayments outpaced sales, suggesting that some NSCs were redeemed through alternative sources. Meanwhile, net foreign financing totalled Tk. 57,133 crore during July-May of FY24, up from Tk. 53,294crore in the same period of the previous fiscal year.

www.bb.org.bd