The financial sector in Bangladesh is poised for a significant transformation aimed at enhancing and strengthening good governance. Recent legislative amendments and Bangladesh Bank (BB)’s strategic initiatives reflect a comprehensive approach to ensuring robust financial governance. The enactment of the Bank Company (Amendment) Act 2023 and the Finance Company Act 2023 are pivotal steps towards integrating good governance within the financial sector. These acts provide a robust framework for financial institutions’ operational and governance standards, delineating clear roles and responsibilities for board members, independent directors, and CEOs to instil discipline and accountability.

The financial sector in Bangladesh is poised for a significant transformation aimed at enhancing and strengthening good governance. Recent legislative amendments and Bangladesh Bank (BB)’s strategic initiatives reflect a comprehensive approach to ensuring robust financial governance. The enactment of the Bank Company (Amendment) Act 2023 and the Finance Company Act 2023 are pivotal steps towards integrating good governance within the financial sector. These acts provide a robust framework for financial institutions’ operational and governance standards, delineating clear roles and responsibilities for board members, independent directors, and CEOs to instil discipline and accountability.

BB’s guidelines on the formation and responsibilities of boards of directors set a high standard for governance in banks and financial institutions. By specifying qualifications, requiring a minimum number of independent directors, and imposing restrictions on familial and representative directors, BB ensures that boards are composed of competent, experienced, and impartial individuals. The introduction of age and experience requirements for directors further guarantees that only seasoned professionals with proven track records will oversee the strategic direction of financial institutions.

The focus on independent directors is a significant move towards safeguarding depositor interests and ensuring unbiased oversight of bank operations. BB’s guidelines clearly define independent directors’ qualifications, responsibilities, and remuneration, ensuring their effectiveness and independence. This fosters an environment where independent directors can contribute significantly to financial institutions’ sound governance and operational integrity.

The guidelines for appointing and reappointing MDs and CEOs are designed to attract and retain top#tier leadership talent. By setting clear eligibility criteria, age limits, and approval processes, BB ensures that financial institutions’ leadership is capable and accountable. Establishing a dedicated committee for evaluating MDs and CEOs underscores BB’s commitment to maintaining high standards in executive leadership.

BB’s strategic measures and regulatory enhancements signal a strong commitment to upholding good governance within Bangladesh’s financial sector. By fostering a culture of accountability, professionalism, and risk management, these initiatives will help build a more resilient and trustworthy financial system. As these reforms take effect, they are expected to enhance depositor confidence, attract investment, and contribute to sustainable economic growth.

Risk Management and Recovery Plans. BB’s proactive approach to risk management is evident in its phased implementation of risk-based supervision (RBS) by 2025, incorporating a meticulously structured pilot program and expert-reviewed guidance notes. This strategic initiative aims to enhance the accuracy, credibility, and consistency of risk assessments using qualitative indicators, thereby fortifying the stability and resilience of Bangladesh’s financial sector.

Having completed the first phase of its pilot program, which involved assessing three banks, BB’s team has developed 16 draft guidance notes. These notes are pivotal in evaluating various components of a customised risk matrix aligned with international standards. Supervisors at BB will utilise these approved guidance notes to assess 20 banks selected for the second phase of the pilot program. Expert input will further refine these guidance notes before final approval by BB’s competent authority. Since 24 February 2022, BB has actively guided the development of recovery plans to equip banks in handling severe stress events affecting their financial and operational stability. These plans empower banks to respond promptly and effectively to potential shocks, ensuring proactive management of stress situations.

Furthermore, BB has established the prompt corrective action (PCA) framework, effective from 31 March 2025, as a pivotal tool for early detection and rectification of banking issues. Monitoring key indicators such as capital adequacy, liquidity, non-performing loans (NPLs), and governance standards enables BB to intervene swiftly to mitigate risks. The framework’s provision for mergers and amalgamations as corrective measures ensures the strengthening of weaker institutions. BB has introduced guidelines for bank-company amalgamation in support of these efforts, encompassing mutually agreed/negotiated and compulsory amalgamation policies. These initiatives aim to bolster the nation’s financial services by enhancing the operational efficiency of banks, thereby fostering a resilient financial sector that delivers enhanced service to the public.

Roadmap to Managing Non-Performing Loans (NPLs). BB is dedicated to addressing the challenge of non-performing loans (NPLs) to stabilise the banking sector and bolster economic resilience. By 2026, BB aims to reduce NPL ratios for state-owned commercial banks (SOCBs) by 10 per cent and private commercial banks (PCBs) by 5 per cent, targeting an overall gross NPL ratio of 8 per cent. This strategy includes legislative reforms, rigorous identification of wilful defaulters, revised loan write-off policies, and enhanced recovery processes.

The Bank Company (Amendment) Act 2023 signifies a stringent approach towards wilful defaulters, defining clear penalties and establishing ‘wilful defaulter identification units’ within banks for systematic identification. Revised loan write-off policies, effective from 18 February 2024, streamline operations while maintaining full provisions for ‘bad and loss’ loans up to Tk 5 lakh without court cases. Enhanced recovery efforts through dedicated units and incentives will drive proactive loan recovery. Aligning with global standards, BB reduced the grace period for overdue fixed-term loans from six to three months, effective 30 September 2024. Starting 31 March 2025, any unpaid instalment will be considered past due immediately after its due date, promoting credit discipline.

BB’s introduction of Alternative Dispute Resolution (ADR) guidelines prioritizes mediation over lengthy legal processes for swifter settlements. The upcoming private asset management company (AMC) will manage non-performing assets, improving bank balance sheets and overall sector health. This comprehensive strategy, backed by continuous monitoring and transparent reporting, aims to enhance asset quality, revenue, profits, and liquidity. BB’s proactive measures ensure a resilient financial system, fostering sustained economic growth and stability.

Enhancing Financial Inclusion and Cashless Society. In alignment with the Government’s ‘Smart Bangladesh Vision,’ BB aims to make 75 per cent of all transactions cashless by 2027 through the ‘Cashless Bangladesh’ program. This initiative underscores BB’s commitment to leveraging technology to enhance financial inclusion and economic stability. Over the past decade, agent banking and mobile financial services (MFS) have significantly expanded access to formal financial services for micro-entrepreneurs and the unbanked population in Bangladesh.

Innovations such as QR code transactions, digital banks, the interoperable transaction platform (Binimoy), and TakaPay are poised to revolutionise the financial landscape by making cashless transactions more affordable and convenient. BB has drafted the ‘E-Money Regulations’ and prepared user guidelines for ‘Bangla QR,’ both pending approval to support these advancements. The draft ‘Escrow’ model, also awaiting approval, aims to promote online e-commerce payments and enhance customer protection. These regulatory measures will ensure digital financial transactions’ safety, security, and efficiency, fostering the growth of cashless services.

Towards Market-oriented Exchange Rate and Build-up of Foreign Exchange Reserves. Given the challenges in the external sector, the Taka-Dollar exchange rates have faced sustained depreciation pressure since mid-2022. In response, BB adopted a gradual approach, allowing market forces to have a greater influence on the exchange rate. This strategy eliminated the complexities associated with multiple exchange rates for exports, imports, and remittances, promoting transparency and efficiency.

BB implemented a crawling peg system on 8 May 2024 to transition towards a free-floating exchange rate system. This interim arrangement is anchored to a currency basket with a mid-rate aligned with the Real Effective Exchange Rate (REER) Index. Allowing market participants to trade around this mid-rate introduces greater flexibility in exchange rate determination while minimizing excessive fluctuations. BB plans to continuously review and adjust the parameters of this regime as needed, paving the way for a fully flexible, market-based system in the near future.

BB has taken adequate measures to bolster foreign currency inflows and stabilise the exchange rate, including securing foreign funds from development partners. Establishing a coherent foreign exchange intervention strategy is crucial for modernising the monetary and exchange rate policy framework. This strategy enhances BB’s operational efficiency and ensures the smooth functioning of the foreign exchange market. The primary objective is to align exchange rate developments with the crawling peg exchange rate arrangement, thereby maintaining stability and predictability.

BB has drafted a comprehensive foreign exchange intervention strategy to support the effective functioning of the newly introduced crawling peg exchange rate regime. BB aims to create a resilient and adaptive foreign exchange market capable of withstanding external shocks by facilitating smoother transitions and maintaining stability. This strategic approach mitigates short-term volatility and lays the

foundation for sustainable long-term economic growth and stability. The theoretical underpinning of this approach lies in the balance between market-determined exchange rates and managed interventions.

The crawling peg system provides a structured path toward flexibility, offering stability while allowing gradual adjustments based on market conditions.

Streamlining Open Market Operation. BB has adopted an interest rate targeting framework, replacing the monetary targeting framework for formulating and implementing monetary policy since July 2023. This shift enables BB to engage more effectively in the money market through various open market operations (OMOs) instruments. To enhance the functionality and efficiency of OMOs under the new monetary policy framework, BB has undertaken several initiatives: (i) Since August 2023, BB has provided unrestricted access to the Standing Deposit Facility (SDF) and Standing Lending Facility (SLF) along with the full allotment of the repo facility for all banks and non-bank financial institutions based on their demand.(ii) In July 2024, BB introduced a repo auction twice a week, replacing the daily repo auction. This change encourages commercial banks to improve their liquidity management capacity and fosters a more active and vibrant money market. (iii) Looking ahead, BB intends to conduct the main OMOs once a week to align the 7-day OMOs with the bi-weekly reserve maintenance period. Additionally, BB plans to introduce overnight OMOs for fine#tuning toward the end of the reserve maintenance period as needed. These measures will help streamline the implementation of monetary policy with efficient liquidity management to foster an active money market.

Monetary Policy Stance: The global economic outlook for 2024 and 2025 appears positive, as major economies have managed to avoid a severe downturn and have successfully reduced inflation without increasing unemployment. In the absence of further significant shocks to food and energy prices, headline CPI inflation is projected to return to levels aligned with central bank targets in most major economies in the coming months.

However, the geopolitical situation remains fragile, with new fears of supply chain disruptions. As global inflation is projected to continue falling, central banks in many economies are expected to begin lowering policy rates this year.

Domestically, recent trends in inflation, monetary aggregates, liquidity, interest rates, foreign exchange reserves, and exchange rates were reviewed following three major policy changes: introducing a crawling peg system, removing the interest rate cap under SMART, and increasing policy rates. The MPS noted that Bangladesh’s economy is rebounding, with inflation moderating but still high. The crawling peg system has stabilized the exchange rate and helped build foreign exchange reserves. Amid tight liquidity, all interest rates have increased significantly, indicating effective policy transmission. Most monetary aggregates have followed projected paths. The Monetary Policy Committee (MPC) concluded that the current monetary policy tightening should continue until inflation reaches a comfortable level. BB will also continue providing comprehensive credit support to agriculture and CMSMEs as part of its supply#side intervention policy to enhance production and support employment generation.

Bangladesh Bank places utmost priority on controlling inflation, which has been persistently high for some time. To manage continued inflationary pressure, in addition to supply-side interventions, BB has pursued a contractionary monetary policy stance for over a year. The policy rate has been significantly increased, with no new high-powered money issued by BB to finance government spending. In line with BB’s policy initiatives, the Government has also taken several measures to control inflation, particularly food inflation, including reducing tariff rates for selected commodities, broadening social protection schemes such as Open Market Sales (OMS), and introducing the Family Card. Moreover, to stabilize the prices of essential high-demand products (edible oil, chickpeas, pulses, peas, onions, spices, sugar, and dates) and ensure adequate supply, BB has instructed authorised dealer branches of banks to maintain the cash margin rate on import LC at the minimum level based on the bank-customer relationship.

Although recent CPI inflation has moderated, it remained above 9.0 per cent throughout H2FY24. With the coordinated and concerted policy initiatives mentioned above, CPI inflation is expected to continue declining in the coming months amid global commodity price temperance. In light of these complex realities, BB is announcing its half-yearly monetary policy stance through this Monetary Policy Statement (MPS) for H1FY25. The policies align with the Government’s budgetary target of reducing inflation to around 6.5 per cent by the end of FY25, which is consistent with BB’s internal forecasts.

By closely monitoring prices and other domestic and international macroeconomic developments, BB has decided to maintain its cautiously tight monetary policy stance for the first half of FY25. BB’s Monetary Policy Committee (MPC) has resolved to keep the policy (Repo) rate unchanged at 8.50 per cent, with the SDF rate at 7.0 per cent and the SLF rate at 10.0 per cent. Additionally, BB will continue its quantitative tightening bias by streamlining Open Market Operations, ceasing currency swaps among banks and BB, and refraining from creating new money to finance government spending. However, BB remains ready to take any necessary policy actions should the situation demand it.

Since mid-2022, the Taka-Dollar exchange rates have experienced sustained depreciation pressures driven by challenges in the external sector. In response, Bangladesh Bank (BB) has taken a gradual approach, allowing market forces to exert greater influence over the exchange rate. This strategy aimed to simplify the exchange rate framework by eliminating multiple rates for exports, imports, and remittances, enhancing transparency and efficiency in currency transactions.

To further stabilise the exchange rate and move towards a more flexible system, BB introduced a crawling peg system on 8 May 2024. This interim arrangement links Taka’s value to a currency basket, with a mid-rate aligned with the Real Effective Exchange Rate (REER) Index, reflecting market equilibrium. Implementing this system has notably reduced foreign exchange market volatility and narrowed the gap between formal and informal market exchange rates to a reasonable level. Additionally, recent liberalisation initiatives in Bangladesh’s foreign exchange policy, such as the RFCD, NFCD, and Offshore Banking Act 2024, are expected to bolster foreign exchange inflows. These measures aim to alleviate pressure on the exchange rate and support rebuilding foreign exchange reserves, contributing to overall stability in the currency market.

As the Forex market is showing reasonable stability and transactions are taking place within predefined bands, BB decides to keep the crawling peg mid-rate unchanged at Tk. 117.00 per USD. BB will also enhance import liberalisation by removing LC margin requirements for all products except luxury goods like cars, fruits, flowers, cosmetics, and similar items, with margins determined based on bank-customer relationships. The crawling peg system is a transitional measure towards a fully flexible, market-based exchange rate system, aiming to stabilise exchange rate movements while preparing for broader market liberalisation.

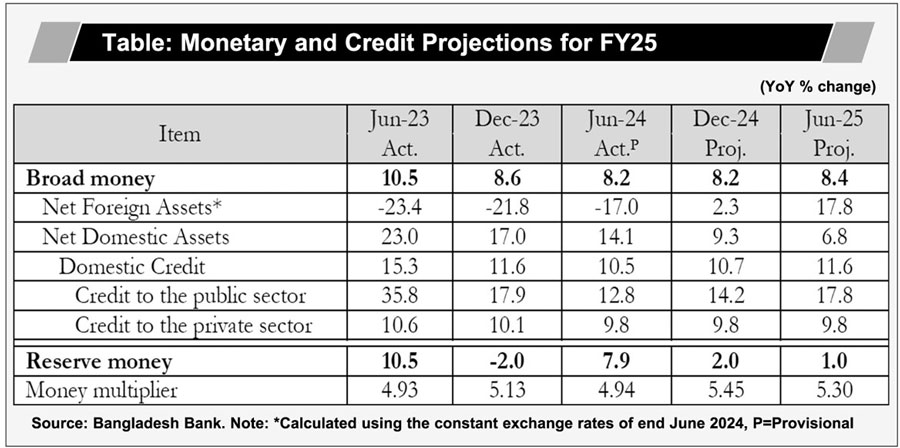

Monetary and Credit Projections for H1FY25. Table shows the half-yearly movements of major monetary and credit aggregates, along with their projection set for FY25. BB adopted an interest rate targeting framework in July 2023, where monetary aggregates such as broad and reserve money are indicative monetary policy targets. Although monetary and credit projections do not get explicit focus in this framework, aligning the interest rate target to uphold price stability, ensure financial stability, and foster desired economic growth is essential.

Moreover, under this framework, BB controls reserve money and broad money by adjusting the policy rate and managing liquidity through cash reserve ratio (CRR), statutory liquidity ratio (SLR), open market operation (repo operation, SLF, SDF, BB bill), assured liquidity support, special liquidity support, advance-deposit ratio, refinance/pre-finance facilities, Mudarabah liquidity support (MLS), and Islamic bank liquidity facility (IBLF).

The growth projection of broad money for FY25 is set at 8.4 per cent, considering the nominal GDP growth target of 10.9 percent, along with the positive change in the velocity of money. Public sector credit growth is projected to be 17.8 percent, considering lower credit demand from the government, as the government has been selectively spending on priority projects in the process of austerity policy measures. Moreover, the government’s FY25 budgetary target is to borrow Tk. 1,37,500 crore from the banking system is also duly considered in projecting the public sector credit growth limit. Private sector credit is projected to grow 9.8 per cent, considering the contractionary nature of the monetary policy to contain persistent high inflation while confirming the BB’s supply interventions to support necessary credit flows to productive and employment-generating sectors through refinance and pre-finance schemes.

Considering the moderate growth in the public sector and private sector, domestic credit growth is projected to be 11.6 per cent for FY25. The net foreign assets (NFA) projection of the banking system is expected to show a positive growth of 17.8 per cent in FY25. The projection of positive growth of NFA is in the overall balance of payment while predicting moderate growth in exports and imports and substantial growth in remittances. Moreover, the supply of foreign funds from the development partners is also considered for the projection of positive growth in NFA.

The projection of Reserve Money (RM) growth is set at positive growth of 1.0 per cent, considering the economic realities and the stable movement of the money multiplier, which is influenced by currency deposit and reserve deposit ratios.

Near-term Macroeconomic Issues and Challenges. Bangladesh faces several near-term macroeconomic issues and challenges that could impact its economic stability and growth prospects. These challenges stem from both domestic and international factors, creating a complex environment for policymakers. Inflation and exchange rate pressures have been major challenges over the past two years. The ongoing unrest in the Middle East and the Russia-Ukraine conflict could impact energy and commodity prices, affecting the domestic economy through import and exchange rate channels. The following are the major macroeconomic challenges for Bangladesh economy:

Bangladesh has been experiencing persistent inflationary pressures, with recent CPI inflation rates remaining above 9 percent. High inflation erodes purchasing power, reduces real incomes, and can lead to an increase in income and consumption inequalities. Global supply chain disruptions, exacerbated by geopolitical tensions such as the Russia-Ukraine conflict and Middle Eastern unrest, have led to higher prices for essential commodities, including food and energy. Bangladesh Bank has been implementing a contractionary monetary policy to manage inflation, but balancing inflation control with economic growth remains a delicate task.

The Taka has been under pressure from external sector difficulties and high import bills, leading to a significant depreciation. This volatility not only increases import costs but also risks imported inflation. In response, Bangladesh Bank (BB) implemented a crawling peg system to stabilise the exchange rate.

While this approach has shown initial success, ongoing monitoring and adjustments are crucial to sustain stability. Moreover, potential policy rate cuts by major central banks such as the ECB and the US Fed could offer some relief from these exchange rate pressures.

Frequent interventions in the foreign exchange market to stabilise the Taka have led to a depletion of foreign exchange reserves. Maintaining adequate reserves is crucial for economic stability and investor confidence. Remittances from exports and wage earners are significant sources of foreign exchange for Bangladesh, and ensuring a steady flow of remittances from these sources is essential for maintaining and building reserve levels. The recent foreign exchange policy liberalisation initiatives like RFCD, NFCD, and Offshore Banking Act 2024 will provide necessary inflows of forex to reduce the pressure on the exchange rate and help rebuild the foreign exchange reserves.

The global economic outlook is positive, but uncertainties persist due to ongoing geopolitical tensions threatening economic stability. Policy rate cuts in advanced economies could influence reverse capital flows and exchange rates. Fluctuations in global commodity prices, especially for food and energy, pose a significant risk to Bangladesh’s economy due to its dependence on imports.

High levels of Non-Performing Loans (NPLs) in the banking sector undermine financial stability and limit credit availability for productive investments. BB is taking measures to reduce NPLs and improve bank governance. Implementing reforms to enhance transparency, governance, and operational efficiency in the banking sector is crucial for financial stability and growth.

Bangladesh faces many near-term macroeconomic challenges, from inflationary pressures and exchange rate volatility to fiscal constraints and financial sector stability. Addressing these challenges requires a multifaceted approach, including prudent monetary policy, effective fiscal management, and structural reforms. By navigating these issues carefully, Bangladesh can sustain its economic growth trajectory and enhance resilience against external shocks.

www.bb.org.bd

© 2026 - All Rights with The Financial Express