The monetary policy statement (MPS) of Bangladesh Bank (BB) for January-June 2018 was released late January. Although none of the monetary targets was changed significantly BB's policy was criticized for being overly cautious (or even contractionary). This was probably because the private sector credit growth was set at 16.8 per cent when the actual annualised growth as of December 2017 was 18.4 per cent. Obviously the target rate was regarded as a restraint on private credit.

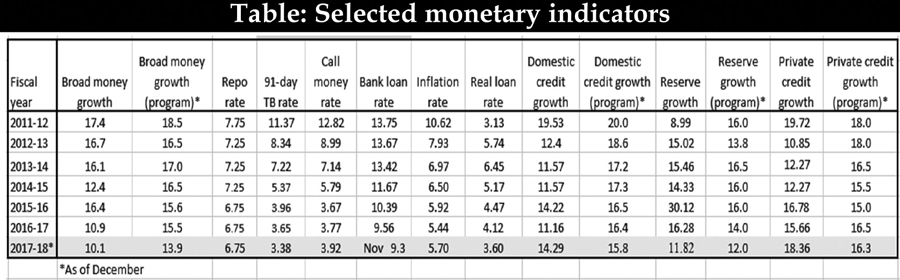

In order to understand the thrust of monetary policy it is not very useful to look at just one parameter, one should take a holistic view of changes in all the major monetary variables that BB influences through monetary policy. Some of these policy variables are presented in Table 1. It will be seen that BB has been steadily reducing the target (programme) growth rate of the most important monetary aggregate, viz. broad money, ever since fiscal year (FY) 2011-12 (from 18.5 per cent to 13.9 per cent). A similar reduction in the programme rates is also observed in the case of monetary reserves and domestic credit.

Interestingly, during this same period the principal monetary tool, REPO rate was reduced from 7.75 to 6.75 per cent. Other interest rates such as 91-day treasury bill rate, call money rate and loan rate all declined steadily from their very high rates in FY 2011-12. Normally a reduction in the money supply should be followed by an increase in the interest rate. The real question is then how a monetary contraction of such a large magnitude could lead to an equally large interest rate reduction across the whole spectrum.

The answer to the apparently puzzling outcome seems to lie in the large reduction in the inflation rate from 10.6 per cent in FY 2011-12 to 5.4 per cent in FY 2016-17. This must have also brought down the inflationary expectations, a major objective of monetary policy. Thus the inflation component of the nominal interest rate was reduced in equal measure. The real intent of monetary policy is to impact on the real interest rate, which alone affects the real economy. If we take the REPO rate to be an indicator of the monetary stance of BB, then the reduction in the rate did not have the desired effect immediately. This is expected as monetary policy changes take time to bite. As inflation continued its downward march, and the REPO rate was further reduced, the real interest (loan) rate finally started climbing down. By November 2017 the real loan rate was only slightly more than half of its value in FY 2013-14. Such a large reduction in the real interest rate was unlikely to have been achieved if the monetary policy was really tight.

With a fall in the actual inflation, and thereby in the inflationary expectations, the demand for nominal money must have also declined proportionately. Thus, the reduction in monetary growth could also be interpreted as market driven rather than policy induced. BB apparently set targets of monetary growth well above the market demand such that the actual growth was mostly less than the target. In FY 2016-17 the target money growth was 42 per cent higher than the actual growth. In other words BB's targets were unlikely to have constrained actual growth. In setting a lower target for monetary growth in recent years BB's objective was most likely geared to achieving a reduction in inflationary expectations. It seems to have been also mindful of the past movements of the monetary aggregates in setting the targets.

Some of the critics of the last MPS seem to be stock market stakeholders who usually canvass for an easy monetary policy for their own benefits. The stock market is just one enterprise of the economy, which incidentally is neither an important employer nor a significant contributor to real investment of the economy. This is generally true in almost all countries of the world for which data are available. Monetary policy should be based on the need of the entire economy. If BB has properly assessed that its programme rates are consistent with the inflation target and the forecasted gross domestic product (GDP) growth, it should not be swayed by some adverse criticisms from interested quarters. Only when it is convinced of a scope for significantly improving on the overall monetary performance should it consider changes to declared policies. BB would do well to keep in mind what its unbridled monetary expansion in FY 2009-10 and FY 2010-11 (partly due to pressures from the stock market) did to the stock market itself and the economy. When the economy faces a difficult situation and the policy responses are not evident, experts hesitate but dilettantes boldly offer populist solutions.

Apart from the good work done by BB officials, a major contributor to the good performance of the monetary sector was the generally stable macroeconomic environment over the last several years. The situation is, however, changing; the economy is becoming more restive. The signs of stress are already apparent in the external sector, which is often the first to respond to emerging difficulties in developing countries.

Since the early years of the new century the balance of payments of Bangladesh has been mostly in surplus, which helped to build up a sizeable stock of international reserves. A major source of foreign exchange earnings, viz. wage earners' remittances, did not perform well. During the last two fiscal years remittances declined considerably from $15.3 billion to $12.8 billion. Remittances showed some improvement in the next eight months of FY 2017-18, but it will probably take a couple of years to recover to the level of FY 2014-15.

After a dull year in FY 2016-17 export showed some increase; but it was overshadowed by import that soared by 25.8 per cent during July-December 2017. This has opened up a large current account deficit of $4.8 billion during this half-year period. To put the deficit in perspective it may be noted that never in the history of the country did it ever run an annual deficit of much more than a billion dollar.

Even more alarming is the fact that import LC openings have registered a massive 75 per cent increase during the same half-year period. The large increase is reportedly due to import LCs for Rooppur Nuclear Power Plant, Padma Bridge, cereals and petroleum products, and according to some people, over-invoicing of import. If many of these LCs are settled during this fiscal year, then the actual import of goods and services could very well approach $65 billion mark. We are then staring at a current account deficit of $15 billion or so.

To what extent the overall balance will also be in deficit depends very much on the magnitude of inflow of foreign capital in the form of foreign direct investment and debt. If the country does receive sufficient foreign capital the stock of international reserves need not decline. But it is doubtful that the market will fail to note the unusually high current account deficit and the consequent increase in foreign debt of the country. If it is unnerved by the deficit it might show up in a depreciating taka and higher interest rate on foreign loans. Despite a slight increase in the international reserves the taka/dollar exchange rate had depreciated by 4.8 per cent between January 2017 and January 2018. Imagine what a few billion dollar decrease in reserves, which is not improbable, could do to the exchange rate.

Any large depreciation of the taka could throw the monetary policy in a spin. Since the country imports many consumer goods, the depreciation will show up more or less immediately in rising market prices of these goods pushing up the consumer price index. This will threaten the BB inflation target. If the export industry can exploit the depreciation to their advantage total export could rise. However, if domestic prices, especially wages, respond to the depreciation the real exchange rate may not improve much, and hence export may not increase. Interest parity suggests that the interest rates could also rise accentuating the recent trend of rising interest rates. All these would be contrary to the monetary policy objectives. BB will need to muster all its expertise, and some more, to steer the economy in the emerging turbulent environment.

These difficulties could compound if the government becomes generous with public money ahead of the general election. Such a government policy will lead to an increase in the budget deficit, which BB might not be able to fully sterilise. There could be a large increase in aggregate demand which would push up both the interest rate and the inflation rate. It will be tough to maintain the monetary policy restraints, especially if the inflation genie gets out of the bottle.

Perhaps the most important change in monetary policy made in the recent past was the reduction in the advance-deposit ratio of the commercial banks from 85 to 83.5 per cent (with effect from July 01, 2018). The odd thing about it is that the reduction was announced shortly after the release of the last MPS. Since MPS is intended to inform the public about the monetary stance of BB, it is not clear why this important change was not included in MPS. Worse still, the date of enforcement the ADR was promptly changed to the end of the year when it came under widespread criticism. The credibility of the MPS will be harmed if such important changes are made without any reference to MPS and people start to believe that policy decisions can be changed by making sufficient noise. Monetary policy could lose its effectiveness and relevance.

The writer is Professor, Department of Economics, University of Dhaka. m_a_taslim@yahoo.com

© 2026 - All Rights with The Financial Express