Muhammad Shahadat Hossain Siddiquee | November 05, 2020 00:00:00

Financial inclusion is the degree and ease of access to financial services by individuals and firms within an economy. Ease of access to financial resources can act as a major tool for promoting economic growth and development. Realising this context, this article attempts to examine financial inclusion in the South Asian countries in comparison to the high-income economies, the Organisation for Economic Co-operation and Development (OECD) countries and the global average. This study uses the percentage of the population owning transactional accounts in an economy as a quantifiable indicator for the level of financial inclusion in that economy. The use of account ownership to be the primary indicator is justified in the intuitive sense that owning institutional accounts makes financial services more accessible. Therefore, a country with higher account ownerships has a greater degree of financial inclusion as the greater percentage of the country's population has the ability to facilitate transactions and avail various other financial services with relative ease.

Data on account ownership have been collected from the Global Findex database. Since 2011 the Global Findex database, a World Bank initiative funded by the Bill and Melinda Gates Foundation (in collaboration with Gallup, Inc), has been collecting data on how adults manage their financial resources. The underlying objective of the article is to compare levels of financial inclusion between

Data on account ownership have been collected from the Global Findex database. Since 2011 the Global Findex database, a World Bank initiative funded by the Bill and Melinda Gates Foundation (in collaboration with Gallup, Inc), has been collecting data on how adults manage their financial resources. The underlying objective of the article is to compare levels of financial inclusion between  developing and developed nations during the timeframe of

developing and developed nations during the timeframe of

2011-2017 using the percentage of account ownership as the quantifiable measure.

2011-2017 using the percentage of account ownership as the quantifiable measure.

GAP IN FINANCIAL INCLUSION IN SOUTH ASIAN ECONOMIES AND HIGH-INCOME ECONOMIES: Initial analysis showcased that, as of 2017, on average, the gap in account ownership between the South Asian economies and high-income countries is very wide. Maintaining 89 per cent account ownership since 2011, high-income countries in 2017 had a 41 percentage points greater account ownership than South Asian economies. However, two other interesting observations also arise. The first is that account ownership in the South Asian economies has been steadily growing at approximately 3 percentage points every year whereas no growth has been observed in high-income countries. The second is that growth in account ownership has been disproportionate amongst the six individual South Asian economies. For instance, from 2014-2017, account ownership grew from 10 per cent to 15 per cent in Afghanistan whereas in India growth has been from 53 per cent to 80 per cent. To understand the reason behind such glaring variations the study examined six South Asian economies individually. Upon closer examination, it is evident that the account ownership itself varies throughout the South Asian economies across various socio-economic and demographic characteristics. The unique characteristics studied are disparities in gender, income, age demographics, level of education and labour force participation.

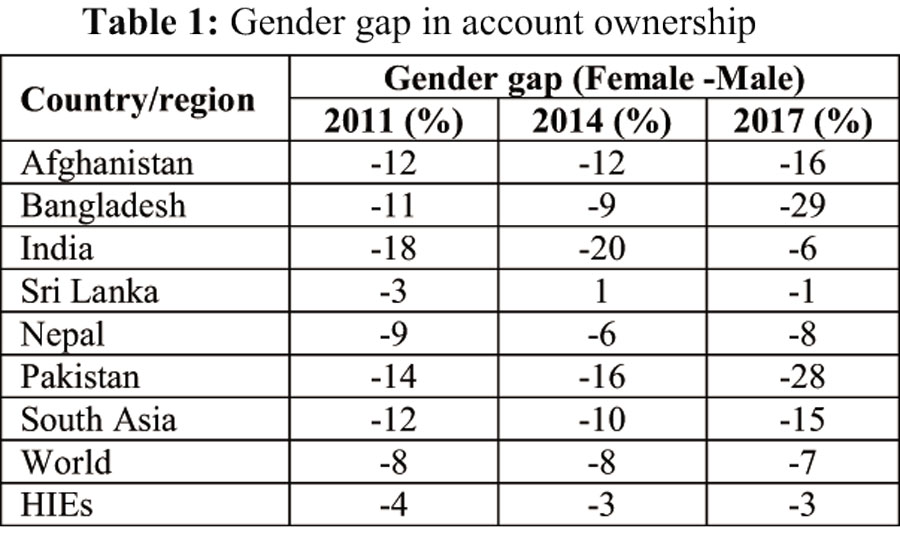

GENDER DISPARITY IN FINANCIAL INCLUSION ACROSS THE SOUTH ASIAN REGIONS: Statistical analysis revealed that disparities in gender are more persistent across South Asian economies than high-income economies. Male and females have not benefited equally from the overall growth in account ownership since 2011 and the common denominator remains across the South Asian economies that women are less likely to own an account as compared to males. As of 2017, the gender gap in account ownership is higher in Bangladesh, Pakistan and Afghanistan (29 per cent, 28 per cent and 16 per cent respectively). What is more alarming is that between 2011 and 2017 gender gaps in South Asian economies have increased in comparison to the high-income economies and the global average.

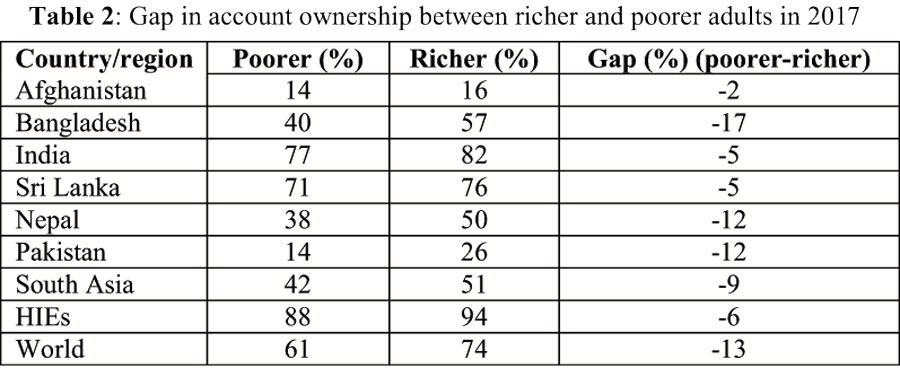

FINANCIAL INCLUSION GAP ACROSS INCOME GROUPS IN SOUTH ASIA: Findings show that people belonging to higher income brackets are more likely to own accounts than people in lower-income brackets. In South Asia, 51 per cent of the richest 60 per cent of households owned accounts while 41 per cent of the poorest 40 per cent of households owned accounts. This gap of nine percentage points (between account ownership of richer and poorer) in 2017 has reduced from 15 percentage points in 2011 for South Asian economies on average whereas the gap for high-income economies has reduced to 6 percentage points in 2017 from 7 percentage points in 2011. This indicates that in accordance with this specific metric, South Asian economies tend to converge towards the high-income economies. However, this conclusion cannot be drawn for all South Asian countries because the gap has increased for Pakistan to 12 per cent in 2017 from 9 per cent in 2011 and the gaps for Bangladesh and Nepal still remain at double digits.

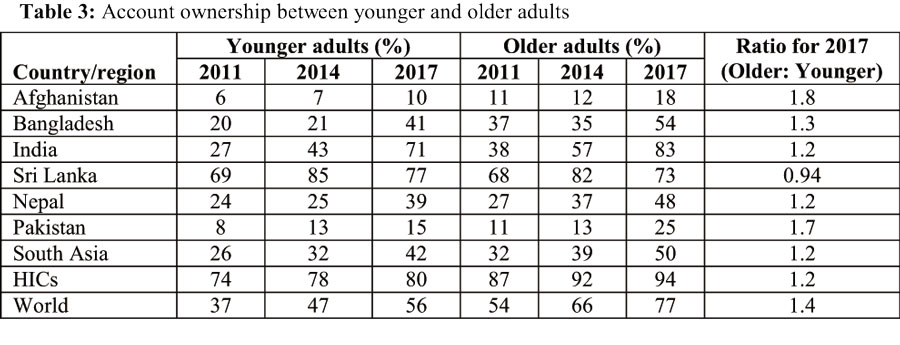

FINANCIAL INCLUSION GAP ACROSS AGE GROUPS IN SOUTH ASIA: Analysis of age demographics indicates that older adults (above 25 years) are more likely to be account owners than younger adults (between 15-24 years). The gap in ownership between older and younger adults in South Asian economies ranged from 6 percentage points in 2011 to 8 percentage points in 2017. This is much lower compared to global average gaps and gaps in high-income economies. However, the gap varies greatly across the individual South Asian economies as Bangladesh, India and Nepal all have a higher age demographic gap in account ownership than the South Asian average. In spite of this fact, the observation that these gaps have been reducing since 2014 provides a positive outlook on the performance of South Asian economies based on the metric of account ownership across age demographics.

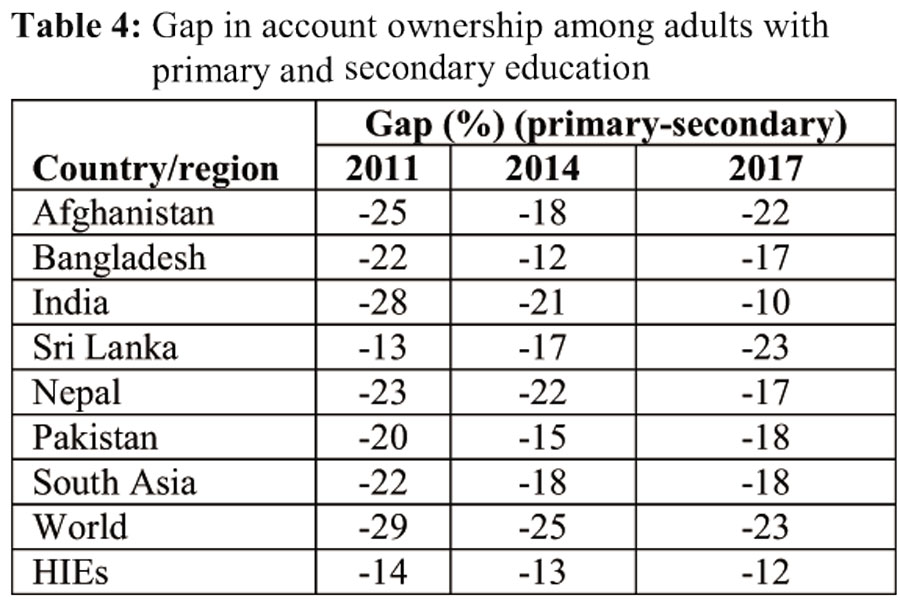

FINANCIAL INCLUSION GAP ACROSS THE LEVEL OF EDUCATION IN SOUTH ASIA: Evidence also indicates that level of education leads to a persistent bias in account ownership as adults with only primary education has been observed to be less likely to own accounts compared to adults who have had secondary education and/or higher. In South Asia, adults with minimal formal education are 18 percentage points less likely to own accounts than adults with secondary or more education. This gap in South Asia between the education groups is the same in Pakistan, Nepal, and Bangladesh. However, Sri Lanka and Afghanistan have relatively larger gaps, while India has the most impressive smallest gap. In comparison to the global average, South Asia collectively is doing better. The global average gap in account ownership across disparity in education level stood at 23 percentage points (18 percentage points for South Asia) in 2017.

FINANCIAL INCLUSION GAP AND LABOUR FORCE PARTICIPATION IN SOUTH ASIA: Finally, studying the relationship between labour force participation and account ownership has resulted in the conclusion that adults who are active in the labour force are more likely to be account owners compared to adults who are absent from the labour force. As of 2017, South Asian economies on average have a 16 percentage points account ownership gap between labour force participants and non-participants. This is worse than that of high-income economies and the world average. It is very alarming to note that except for Nepal and India, this gap has risen greatly from 2011 to 2017.

The findings of this study are indicative of two major conclusions. Firstly, on average, while financial inclusion is still lacking in developing South Asian economies compared to high-income economies - South Asia is not falling behind but rather catching up. The heightened global interest to incorporate accessibility to financial resources as a tool for economic growth and development has led many South Asian countries to adopt policies targeting the promotion of inclusive finance. However, it is evident that such policy projects cannot be based on a one-size-fits-all model. The study clearly showcases how growth in financial inclusion is not uniform but rather disproportionate throughout different South Asian countries across multiple distinct characteristics. Each country has unique challenges to overcome and thus will require a unique policy design accordingly. Ultimately, the underlying framework to promoting the growth of financial inclusion in South Asia lies within the institutional effort to make financial services available for vulnerable groups like younger adults, adults with minimal education, adults out of the labour force, adults living in poorer households and adults victimised by patriarchal gender bias.

Dr Muhammad Shahadat Hossain Siddiquee is a professor at the Department of Economics, University of Dhaka.

shahadat.siddiquee@du.ac.bd

© 2026 - All Rights with The Financial Express