Unavoidably, there is no other alternative than huge borrowing to fulfill higher growth target and to cope with the COVID-19 impacts. Managing public debt with insight and prudence is also much more critical than ever before. Public debt situation is challenging because we cannot stop borrowing on the one hand, and must repay debt on schedule, on the other. What is the scenario of our revenue collection and overall financing? Are we heading towards debt distress? How far practicable are the IMF-set thresholds or benchmarks for public debt sustainability in Bangladesh? Foregoing discussion aims to focus on such questions.

The government's debt obligations are created in terms of direct borrowing for public operations, and offering public guarantee for other organisations. However, a glimpse of some trends of our public borrowing, revenue collection, revenue surplus and indicators is first necessary for dealing with the questions raised above.

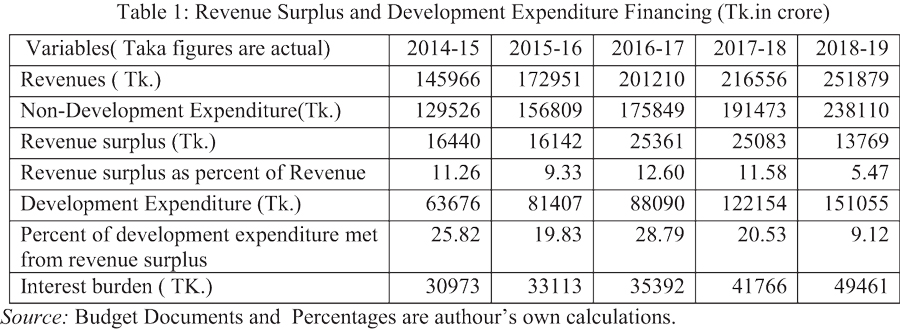

As indicated in Table 1, revenue surplus tends to diminish in both absolute and relative terms from FY2017 and it is just 5.47 per cent while non-development expenditure absorbs about 95 per cent of government revenues collected. It is to be noted that the period under review is before the onslaught of COVID-19. Revenue-generated or equity fund availability for development expenditure financing has on an average narrowed down gradually. During the fiscal year 2018-19, the average percentage of revenue surplus to meet development expenditure has halved as compared to those of previous years. This is the strategic area of our prudent fiscal management and also a focal point. The table suggests that more than 90 per cent of fund needed for development expenditure depends on borrowing. The position during FY20 could not be displayed owing to non-availability of actual data. It is observed from the table that interest burden has been rising every year.

As indicated in Table 1, revenue surplus tends to diminish in both absolute and relative terms from FY2017 and it is just 5.47 per cent while non-development expenditure absorbs about 95 per cent of government revenues collected. It is to be noted that the period under review is before the onslaught of COVID-19. Revenue-generated or equity fund availability for development expenditure financing has on an average narrowed down gradually. During the fiscal year 2018-19, the average percentage of revenue surplus to meet development expenditure has halved as compared to those of previous years. This is the strategic area of our prudent fiscal management and also a focal point. The table suggests that more than 90 per cent of fund needed for development expenditure depends on borrowing. The position during FY20 could not be displayed owing to non-availability of actual data. It is observed from the table that interest burden has been rising every year.

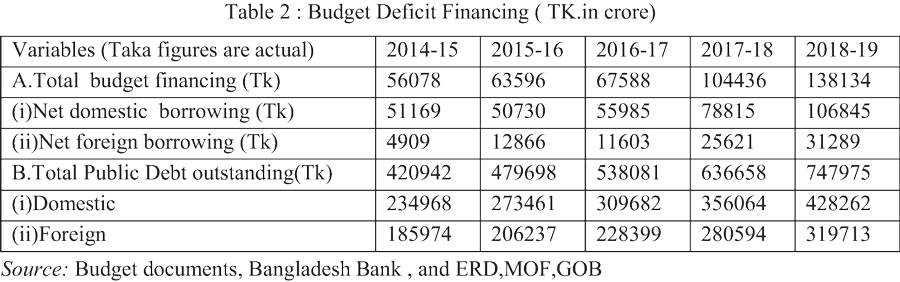

Table 2 shows that government borrowing has continued to increase every year from both domestic and foreign sources. The trend is usually normal as we have to accelerate the speed of the engine of growth. The immediate consequence is that investment in development infrastructure has become increasingly dependent upon debt, largely domestic one which is explicitly more expensive. Is there anything symptomatic of debt distress? This question cannot answered unless we compute some relative measures and compare them with some logical standards

Table 2 shows that government borrowing has continued to increase every year from both domestic and foreign sources. The trend is usually normal as we have to accelerate the speed of the engine of growth. The immediate consequence is that investment in development infrastructure has become increasingly dependent upon debt, largely domestic one which is explicitly more expensive. Is there anything symptomatic of debt distress? This question cannot answered unless we compute some relative measures and compare them with some logical standards

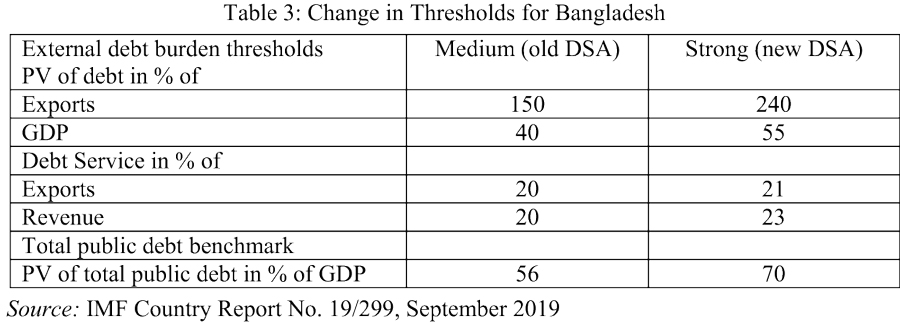

As a member country of IMF, we have to comply with their guidelines and recommendations. It should be borne in mind that IMF itself extends credit to member countries subject to many conditionalities which seem to intervene in a sovereign country's economic decision making. IMF rates a country based on the degree of implementing the conditionalities. We have, in this regard, made considerable progress as desired by the IMF. Bangladesh has been classified as 'Strong' in terms of debt carrying capacity. So, IMF brought about changes in debt thresholds and benchmarks as depicted in Table 3.

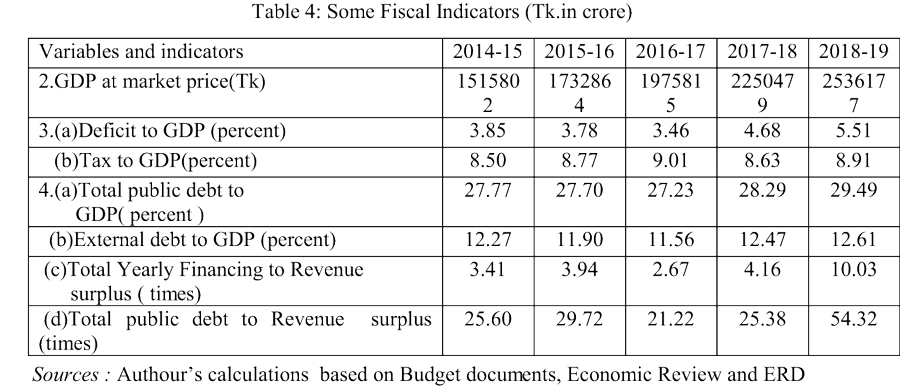

As per Table 3, the benchmark for total public debt is now 70 per cent of GDP instead of 56 per cent. Besides this, external debt (calculated present value) may be 240 per cent and 55 per cent of exports and GDP respectively. Now we need to look at Table 4 to compare our debt position.

As per Table 3, the benchmark for total public debt is now 70 per cent of GDP instead of 56 per cent. Besides this, external debt (calculated present value) may be 240 per cent and 55 per cent of exports and GDP respectively. Now we need to look at Table 4 to compare our debt position.

Against IMF thresholds / benchmarks, external and overall debt ratios to GDP ( 4a and 4b in Table 4) lie far below 55 per cent and 70 per cent. If discounted, the debt scenario would be much better, but the concept of present value with a discounting factor is not considered here in order to allow simplicity of understanding. However, GDP (or exports) used by IMF and each country as basis for computing relative debt status may be questioned

Against IMF thresholds / benchmarks, external and overall debt ratios to GDP ( 4a and 4b in Table 4) lie far below 55 per cent and 70 per cent. If discounted, the debt scenario would be much better, but the concept of present value with a discounting factor is not considered here in order to allow simplicity of understanding. However, GDP (or exports) used by IMF and each country as basis for computing relative debt status may be questioned

How does a country repay her debt? What is the source of fund? Repayment capacity is basically generated by revenue surplus, not directly by GDP. Fund for debt repayment is thus directly related to the size of excess of revenues collection over non-development expenditure. GDP is owned by the private sector owners in a free market economy. As our economy is run by the private sector, the government owns a certain portion of GDP in terms of tax revenue. Quantitatively, debt ratios based on revenue surplus yield direct relationships and relevant comparisons

It appears from the Table 4 that debt ratios in 4(c) and (d) expressed in times exhibit alarming situation of public borrowing. In FY19, we borrowed to meet the yearly budget deficit of every Tk.10.03 against which we generated a revenue surplus of Tk.1.00 only. Accordingly, we had a revenue surplus of Tk.1.00 only against the outstanding debt of every Tk.54.32. Thus it is obvious that debt carrying capacity based on IMF measures and that based on revenue surplus are in sharp contradictions.

Public debt management seems to be very poor as we are unable to diagnose any problem of debt level. We are guided by debt thresholds and benchmarks set by IMF. It is essential to develop our own standards for proper assessment of public debt trends and dynamics. The purpose of public debt management would be to increase tax to GDP ratio, minimise non-development expenditure, and to reduce debt dependence with a time-based strategic plan.

Haradhan Sarker, PhD, is ex-Financial Analyst, Sonali Bank & retired Professor of Management. sarker19582018@gmail.com

© 2026 - All Rights with The Financial Express