Bangladesh's increased borrowing in recent years has augmented the country's exposure to rising interest rates and heightened market volatility. The problem has been further compounded by the depreciating currency. The country is also experiencing high inflation. Overall, the country's external finances have been under pressure since early 2022 owing to widening current account and fiscal deficits and falling foreign exchange reserves necessitating increased levels of borrowing.

According to the IMF data, the public debt/GDP ratio for Bangladesh was 28.7 per cent in 2014, that has shot up to 42.1 per cent in 2023. Now the combination of the pandemic, economic slowdown, high inflation (9.69 per cent in July) and higher commodity prices are creating stress on the external balance along with high debt levels evoking fears of a new economic crisis in Bangladesh. Also, the inflation problem has been made worse by a surging US dollar.

As both the current account and fiscal deficits have widened, inflation has risen creating pressures on Bangladesh's external economic profile. Also, according to the Bangladesh Bank (BB) data, Bangladesh's gross foreign exchange reserve declined to US$23.5 billion in July this year relative to the same month last year when foreign exchange reserves stood at US$39 billion.

But it is estimated that the usable foreign exchange reserve is about US$20 billion once non-liquid assert are excluded. This decline is attributed to the reduced flows of export earnings and remittances and rising import bills. Bangladesh also loses a huge amount through under- and- over invoicing of exports and imports or more precisely through money laundering.

However, Bangladesh's public foreign debt is mostly owned by the government to multilateral and bilateral creditors, at about 48 per cent and 30 per cent of outstanding foreign debt respectively. Bangladesh now faces reduced flow of foreign financing at a time of rising debt levels with rising interest payments along with principal payments.

This year alone Bangladesh will dish out US$1.19 billion in interest payments and such interest payments are likely to grow further in coming years. In fact, the latest available data (FY 2022-23) indicate that Bangladesh's balance of payments (BoP) continues to deteriorate as reflected in deficits both in the current and the financial accounts (see FE, August 4).

Rising debt levels are now also marked by high inflation in the country. The high inflation rate has a direct effect on poverty levels in the country. According to the Household Income and Expenditure Survey (HIES), 2022, the poverty rate in the country now stands at 18.7 per cent at the national level. Yet, considering the fall in the poverty rate, the actual number of poor people has not decreased. It is estimated that 35 million people in Bangladesh live below the poverty line according to the Bangladesh Poverty Watch Report, 2022.

Increasingly widening gap between the Consumer Price Index (CPI) and the Wage Rate Index (WRI) is eroding the real wage of working people in general and but far more severely impacting on working people belonging close to the poverty line. Close to 90 per cent of Bangladesh's working people are employed in the informal sector where most of them are employed as daily wage earners without any job guarantee.

Bangladesh is indeed now facing serious economic challenges. The country is the third South Asian country apart from Pakistan and Sri Lanka to ask for financial support from the IMF last year. Total funding by the IMF under its three facilities amounts to US$4.7 billion to enable Bangladesh to deal with its external balance and budget deficits. Bangladesh also sought loans from the World Bank and other multilateral agencies and donor countries including Japan. This has made some commentators to opine that Bangladesh has gone from an economic miracle to needing IMF help.

S&P Global Ratings last month (July 25) downgraded Bangladesh's long-term rating outlook from stable to negative without lowering the overall credit rating. The reasons cited for downgrading include weakened financial position and current political conditions which appear to be further deteriorating since the new credit rating was made.

Also, in May this year another credit rating agency Moody's downgraded Bangladesh's credit rating from B3 to B1. Standard & Poor's (S&P), Moody's and Fitch Ratings are the three largest and most prominent credit rating agencies in the world.

With the current political turmoil continuing, Bangladesh's external financial position may continue to further deteriorate. S&P Global Ratings also expressed concern that highly concentrated political environment is likely to limit the effectiveness of institutions and checks and balances on the government notwithstanding many other limitations including high levels of perceived corruption. This may result in the country's overall credit rating also being downgraded from the current level with implications for public and private sectors' borrowing ability and interest payments liabilities.

Total public debt in Bangladesh is now estimated to stand at US$169 billion. Most of the public debt is domestic and denominated in the local currency (US$95 billion) accounting for about 56 per cent total debt stock. About half of the outstanding domestic debt is composed of the National Saving Certificate, yield on which is higher than government bonds of similar maturity.

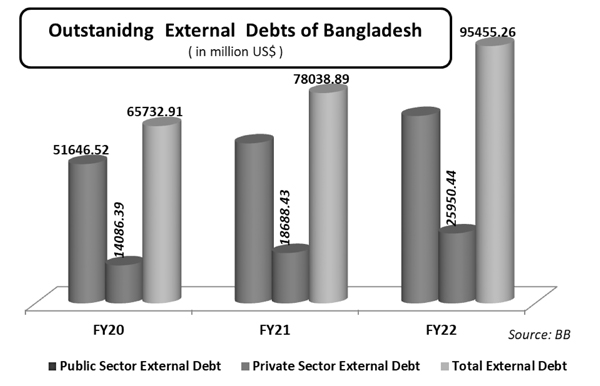

Over the last two years Bangladesh's foreign debt has increased by more the US$27 billion. This represents 227 per cent increase in foreign debt over the last one decade. Between July 2022 and April this year, according to the Bangladesh Bank (BB) data, the government borrowed a total of TK 82,057 crore from the banking system, of which the BB provided around 80 per cent. In April this year alone, the government borrowed a record amount of Tk 29,697 crore from the banking system.

Furthermore, the budget for the current financial year (2023-24) is running a deficit of Tk 2,45.064 crore and that amounts to 36 per cent the total budget outlay. The government announced that the deficit will largely be financed by borrowings from the country's banking system. It is widely considered that commercial banks are unlikely to meet the demand, therefore, the BB remains the main source of deficit finance.

It is to be noted that commercial banks in Bangladesh are saddled with very high levels of loan defaults which have significantly constrained these banks' ability to extend loans to the government. Bangladesh's Non Performing Loans (NPL) ratio stood at 8.8 per cent in March 2023 compared to the ratio of 8.2 per cent in the previous quarter. Bangladesh ranks second only after Sri-Lanka in terms of the NPL among countries in South Asia.

Such high levels of borrowing from the banking system can strain the banking system hindering its ability to support private sector lending, thus further straining economic activity. Equally worrisome is the government's borrowing from the BB. This further expands the size of the central bank's balance sheet and injects new cash into the economy and money supply grows adding to the inflationary pressure. Rising inflation can hinder economic growth and stability and discourage FDI which has already remained persistently low.

Such borrowing by the government from the central bank also creates further problems as it entails holding of a more "neutral asset", like government debt, and leads the central bank towards financing governments fiscal deficit. Therefore, calling into question the central bank's independence notwithstanding the creation of new money resulting in further inflationary pressures.

Bangladesh's foreign debt has increased by about US$27 billion in just over the past two years, now accounting for close to 44 per cent of total debt burden. This escalating debt levels pose serious risks to economic stability and growth prospects. In fact, public debts as indicated by the recent borrowing sprees from the domestic sources could become unmanageable, especially if interest rates remain high. More importantly, every step in borrowing will hamper the government's ability to respond to the next crisis.

Meanwhile, the World Economic Forum's latest Global Risk Report identified the top five risks for Bangladesh for the next two years. They include rapid inflation, debt crisis, price shocks, human-made environmental damage and geopolitical contestation for resources.

However, the Bank of International Settlement (BIS)-- the global umbrella organisation of the World's central banks in its Annual Report 2023 noted that the "rather unique combination of high inflation and widespread financial vulnerabilities is not simply a bolt from the blue" and not just a product of the Covid-19 pandemic and the war in Ukraine. The roots of the problem go deeper and "debt and financial fragilities do not appear overnight; they grow over time".

The fear is public debt can become unmanageable if interest rates continue to rise and remain high. Furthermore, debt-fuelled economic growth is unlikely to generate sustainable growth. To mitigate the risk of a financial crisis which will lead to recession, trade-offs between spending and saving may be needed along with the priority for fiscal consolidation. Fiscal consolidation would provide critical support in the inflation fight.

Bangladesh's tax to GDP ratio now stands at 9 per cent, one of the lowest in the world and the proportion of direct taxes (i.e., income and corporate taxes) account for only 35 per cent of total tax revenue. All these make necessary for taxation reform to raise increased revenue by increasing direct forms of taxation which remain very low in Bangladesh relative to most countries in the world.

muhammad.mahmood47@gmail.com

© 2026 - All Rights with The Financial Express