Most people face the temptation to borrow money to meet their basic needs. They dream of living in a comfortable house, driving a nice car, or pursuing a higher education. As such, debt financing has become a common practice. Islam does permit debt; however, the repayment must be without interest. Zakat banking deploys the two fundamental Islamic economic teachings, Zakat on the depositors’ side and Qard Hasana on the borrowers’ side, as reform to interest-based debt financing. This concept entails Zakat taking precedence over riba in the monetary system.

Thus, the current paper aims to offer an alternative solution to riba in Islamic banking. Riba entails depositors gaining at the expense of the borrowers. The author proposes a solution to combat this process, which Islam prohibits under its ethical-legal norms. The main idea of the proposed Zakat banking approach is that depositors would pay Zakat while borrowers would enjoy Qarda Hasana. As a bank, Zakat Banking provides similar banking services to account holders, such as transfer and withdrawal at minimal fees. Such a fee would replace the interest income spread practised in typical banking systems to make profits.

The author defines trade and riba by relating them to the concepts in the Holy Quran. Sura Al-Baqarah, verse 275 of the Holy Quran, expresses a significant contrast separating trade and riba: “Those who devour usury will not stand except as stand one whom the Evil One by his touch hath driven to madness. That is because they say: ‘Trade is like usury,’ but Allah hath permitted trade and forbidden usury. Those who, after receiving direction from their Lord, desist shall be pardoned for the past; their case is for Allah (to judge); but those who repeat (The offense) are Companions of the Fire: They will abide therein (forever).” (Al-Quran [2:275])

This verse explains that Islam permits trade since it promotes well-being but forbids riba, or usury, since it constitutes elements of inequitable gain.

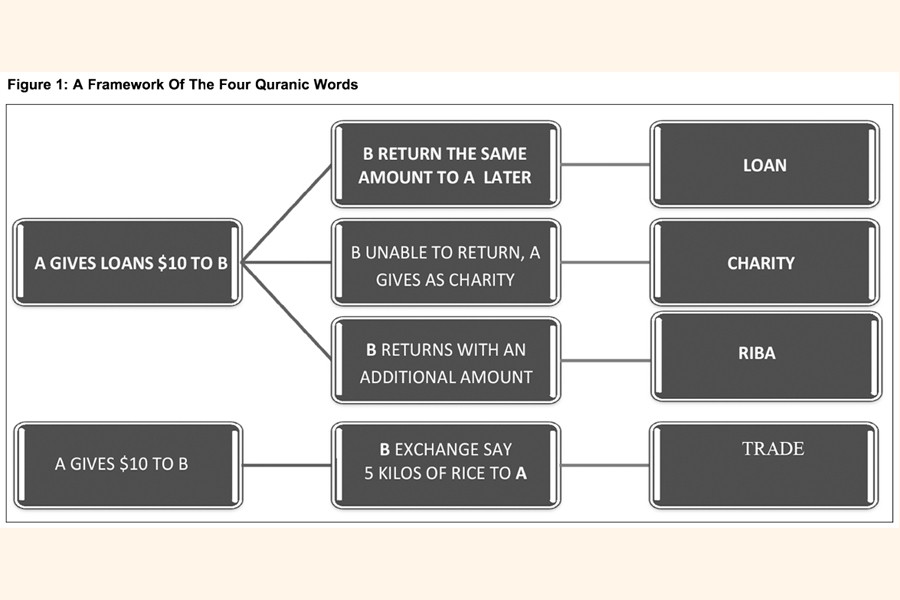

Banks offer various types of loans, such as mortgages, student loans, and car loans. Under the conventional banking system, loan repayment includes interest or riba, which defies Islamic social norms. Islam only permits loans without interest or Qardan Hasana.

Charity, defined as a good deed (i.e., Zakat and Sadaqah), is the opposite of riba since Allah will reward charity with His blessings: “That which you give for Riba to increase through the property of (other) people will have no increase with God. But that which you give as a charity (zakah), seeking the Countenance of God (will increase); it is these who will get a recompense multiplied”. (Al-Quran [30:39])

The four concepts above, loan, charity, riba, and trade, are illustrated in Figure-1 below.

There are three types of riba:

Ribafadhlu – also knownas Buyu’, is defined as the exchange of similar goods but in different quality or quantity

Riba An-Nasi’ah–also known as Riba Duyun, is defined as additional money paid to the lender for his waiting period.

Riba Jahiliyyah –is the extra money spent when the borrower cannot repay the loan after it is due.

Listed below are ten narratives of riba described from various Ayat found in the text of the Holy Quran:

1) Riba means an increase in a loan.

2) Consume riba is considered ruthless to the borrower.

3) Denying the lender of ra’s al-mal is also ruthless

4) Riba includes doubling and redoubling the loan.

5) Charity is the opposite of riba.

6) Riba and trade are different.

7) Riba brings downfall, and Sadaqah brings growth.

8) Taking riba is consuming other people’s wealth.

9) Riba was prohibited to the Jews and Christians as well.

10) Consuming riba is a major sin.

Islamic banking derives profits from trade transactions. Many critics believe the Islamic banking system adapts conventional banking, where banks profit from interest or riba. Conventional bank charges interest rates to borrowers as a payment for the use of borrowed money from the depositors. There are many interest rates, such as interest on a loan, deposit rate, treasury bill, and money security. As explained previously, the interest rate charged by the bank to the borrowers is higher than the rate the bank pays their depositors; such differences are known as interest spread, mainly to cover operating costs and profit.

Critics of Islamic banking believe that the system is not genuinely Shariah-compliant since the Islamic banking system sharesa similar framework with conventional banking that lets depositors gain at the borrowers’ expense. Islamic banking products include murabaha, a sale-based instrument; istinaa, the financing of commissioned manufacturing or construction; and salam, a forward sale. Other products include ijara, a lease-based mechanism similar to traditional leasing with particular distinctions, and mudaraba, an equity-based financial intermediation that takes place through profit-and-loss arrangements. Some may argue that Islamic banking is indirectly involved in riba. They say that it is a mere change of label. For competitive reasons, Islamic banks must ensure that their “profit rate” is equivalent to the conventional “interest rate.”This assurance averts the potential of arbitraging between the two banking operations. This criticism motivates this paper as the author seeks to propose an alternative solution to living in a riba-free environment.

The third Islamic pillar, Zakat, is the required payment prescribed by Shariah to be paid annually on zakatable assets to be utilised for charitable and religious purposes among the eight recipients. Zakat is used as an instrument to assist Muslims that fall under the recipient categories. As gold and silver, paper money is also subject to Zakat. The authors re-evaluate this concept in developing their proposed solution to riba. They suggest that Muslims pay Zakat more regularly on a monthly subject to the availability of the “nisab”. In other words, Zakat should be deducted from the accounts monthly by converting the 2.5 per cent annual rate into a monthly rate. The justification for this proposed strategy is that Muslims would fulfil their duty of Zakat, which would also benefit the economy.

If implemented, Zakat banking would namely have three roles:

To provide financial services to account holders. Zakat banking would charge account holders nominal fees for the various value-added services such as money withdrawal and transfer. Thesefees would produce a marginal profit for the bank instead of relying on the riba-based interest spread between borrowers and depositorsin the conventional banking system.

To act as Amil, which the bank is entitled to 1/8 of the zakat contribution. The time depositors do not receive any return from their depositedmoney, which is considered riba. Instead, they would consider it an opportunity to pay their annual religious duty, but on a monthly or daily basis, a concept that the author proposes and compares to a Muslim’s duty to perform salat regularly.

To offer Qardan Hasana. Zakat Bank will provide loans without interest known as Qardan Hasana. However, Qardan Hasana is not Sadaqah (charity) because it has to be repaid to the bank. Zakat banking would offer interest-free loans where the borrower specifies the time of repayment. It is reported from the Prophet (s.a.w.) that the reward by Allah s.w.t. for Sadaqat is ten times, whereas Qardan Hasana is eighteen times, which shows that Qardan Hasana has more significant value. In essence, Zakat banking would prevent depositors from making gains at the borrowers’ expense, as practiced in conventional banking.

In conclusion, the authors proposes a new framework to combat riba in banking by synthesising Zakat obligation into Qardan Hasana. They suggests the logic behind Saidina Uthman’s well story to apply and implement this strategy.

The story is: “In Medina, water was scarce. A well was owned by a Jew who charged a high price for his water. Saidina Uthman R.A. offered to buy the well, but the Jew declined. Because he was a skillful trader and negotiator, he negotiated a price for half the well; he would have control one day and the owner the alternate days. Saidina Uthman R.A. gave out his water to the Muslims freely, leaving the Jews with no customers on alternate days. The original owner of the well had no choice but to sell his half to Uthman, who nevertheless paid a fair price for it.”

The need is to develop an institution to play the role of Saidina Uthman in this story. This institution would give out loans at zero interest. Soon after, conventional banks would lose their customer base, and people would become uninterested in borrowing money that charges interest. When conventional banks begin losing customers for borrowing, these banks will not have interest income to compensate depositors and will soon lose their depositors. Conventional banks then will have no alternative but to convert to Zakat banking. When that happened, Zakat collection and distribution played an essential role in the mainstream of the economy.

The benefits are two folds; it opens the door of goodness by deploying Zakat, and by the same token, it closes the door of evil by rejecting riba, possibly very much in line with the hadith narrated by Anas bin Malik (Sunan Ibn Majah 237).

Dr M Kabir Hassan is Professor of Finance at the University of New Orleans, Louisiana, USA. KabirHassan63@gmail.com

Abdul Malek Talib is a Ph.D. researcher at the IIiBF, International Islamic University, Malaysia

© 2026 - All Rights with The Financial Express