After decades of price stability, notably in advanced economies, prices of food and non-food commodities are on the rise globally. The annual inflation rate in the United States (US) soared to a four-decade high of 8.5 per cent in March, widely missing the Federal Reserve's inflation target of 2 per cent. Not far below the US rate, the overall price level in the eurozone registered a 7.5 per cent increase in the same period. The 10-year breakeven rate, derived from the difference between conventional and inflation-adjusted Treasury yields, is hovering around 3 per cent, surpassing the previous high reached in 2005.

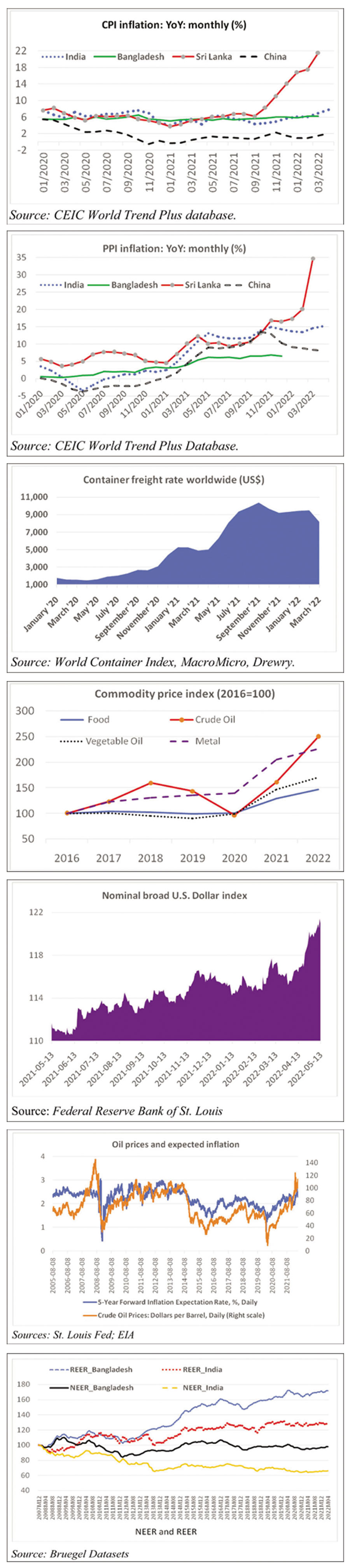

In emerging markets and developing economies (EMDE) consumer prices are spiking fast. In almost all the countries is South Asia Consumer Price Index (CPI), which measures the total value of goods and services consumers purchase over a specified period, is rising steadily. In Bangladesh, year-on-year (YOY) consumer prices surpassed 6 per cent level in the first quarter of 2022, which is higher than the Bangladesh Bank's inflation target set at 5.3 per cent for the year. There are concerns that the official inflation figure of Bangladesh underestimates the actual consumer prices. In Sri Lanka and India, CPI inflation shoot up 21 per cent and 8 per cent, respectively in March.

In emerging markets and developing economies (EMDE) consumer prices are spiking fast. In almost all the countries is South Asia Consumer Price Index (CPI), which measures the total value of goods and services consumers purchase over a specified period, is rising steadily. In Bangladesh, year-on-year (YOY) consumer prices surpassed 6 per cent level in the first quarter of 2022, which is higher than the Bangladesh Bank's inflation target set at 5.3 per cent for the year. There are concerns that the official inflation figure of Bangladesh underestimates the actual consumer prices. In Sri Lanka and India, CPI inflation shoot up 21 per cent and 8 per cent, respectively in March.

The Producer Price Index (PPI) measures price changes before goods reach consumers, it is seen as an earlier predictor of inflation than the CPI. The YOY growth of monthly PPI, which was close to zero for Bangladesh, low in Sri Lanka, and negative for both China and India at the beginning of the Covid-19 pandemic, increased sharply in recent months reaching 7 per cent, 22 per cent, 8 per cent, and 15 per cent, respectively. This relatively higher input inflation is initially passed through to retailers and eventually to consumers.

THEORETICAL PERSPECTIVE: The quantity theory of money, one of the oldest economic theories, postulates that "the general price level of goods and services is proportional to the money supply in an economy." If the money supply grows higher than the relative size of the economy, then prices rise eroding purchasing power of consumers. In other words, expansionary monetary policy causes higher inflation.

Aggregate demand fuelled by fiscal stimulus and lower interest rates, among other factors, and supply shocks such as energy shortage can cause inflation-- the former and latter known as "demand-pull" and "cost-push" inflation. The macroeconomic theory of the 1960s on the trade-off between inflation and unemployment, known as the Phillips curve, ended in the stagflation of the 1970s.

Lately, following the advent of rational expectation theory in the 1970s numerous studies found that households' and firms' expectations of future inflation are a key determinant of actual inflation. The mechanism in which it works is that "expectations determine households' savings and consumption through the relationship between perceived real interest rates and consumption." The New Keynesian Phillips curve which explains the determination of realised inflation attributes an important role to inflation expectations.

RECENT DRIVERS OF INFLATION: Several factors drive the current global inflation. These are discussed below.

Massive fiscal stimulus amid the pandemic. Governments notably in advanced countries allocated US$10 trillion for economic stimulus in just two months after World Health Organisation (WHO) declared the Covid-19 a pandemic in March 2020. According to McKinsey, the size of the stimulus is three times more than the response to the 2008-09 financial crisis. In Bangladesh, the stimulus package of Tk 1.24 trillion might have contributed to inflationary pressure.

Some economists, notably former US Treasury Secretary and Harvard Professor Larry Summers cautioned as early as 2020 that "macroeconomic stimulus on a scale closer to World War II levels than normal recession will set off inflation pressures of a kind we have not seen in a generation." He has been proven to be right.

Disruption in the global supply chain: The initial large-scale lockdown measures and the prolonged pandemic owing to the Delta and Omicron variants have had damaging effects on supply chains and the labour market. The supply of numerous commodities and goods has been unresponsive to higher demand reflected in, among other factors, bottlenecks, rising shipping costs, delivery delays, and shortages of key production inputs such as computer chips. There was a dramatic rise in container freight rates between January 2019 and March 2022, reaching a record price of nearly $10400 in September 2021 from as low as $1446 in April 2020, a 600 per cent increase.

China's zero Covid policy and its impact on supply chain. China's status as the factory of the world and its critical role in the global supply chain markedly affected the prices of manufacturing goods owing to the country's zero-Covid policy. The recent lockdown in Shanghai is likely to exacerbate global supply-chain problems and inflation concerns as the city accounts for around a fifth of China's port volume.

Relatively higher spending on goods than services: Before the pandemic, consumer spending on goods had been declining relative to services for several decades. However, given the travel ban and other restrictions during the pandemic coupled with the rise in online platforms, the demand for goods outpaced services.

War in Ukraine and elevated energy and commodity prices. According to World Bank, energy prices were more than four times higher in March 2022 than their April 2020 lows-the largest 23-month increase since the oil shock of 1973. Fertiliser prices rose by 220 per cent during the same period. Similarly, prices of food of which Russia and Ukraine are large producers supplying over a quarter of global wheat exports rose by 84 per cent. As a result, there has been a big jump in fuel and non-fuel commodity price indices in the past five quarters.

INFLATION OUTLOOK FOR 2022 AND BEYOND: Now the big question is whether the current bout of inflation is transitory or elevated prices are here to stay. Amid the lockdown, Besides, China's zero-Covid policy, the war in Ukraine and associated geopolitical risks, the export ban of commodities by several countries, and the strong US dollar are driving near and mid-term inflation expectations.

Bull run of fuel and non-fuel commodity. A World Bank estimate shows that energy prices could rise more than 50 per cent in 2022 before easing in 2023 and 2024. Industry experts offer plenty of scenarios where oil could hit $150 per barrel."Non-energy prices, including agriculture and metals, are projected to increase by almost 20 per cent in 2022. Export ban on several commodities by numerous countries including India will only exacerbate price hikes.

Ascend of US dollar and imported inflation. Amid Fed's monetary tightening by raising interest rates to fight inflation, capital is flocking to the US in search of higher yields. The US Dollar Index, which tracks the dollar against six other important currencies reached the highest level since 2002. There is a growing demand for safe-haven assets like the U.S. Treasury (10-year Treasury yields 3.1 per cent return) which is more attractive compared to the bond issued by other central banks, including the Bundesbank (1.1 per cent) and Bank of Japan (0.25 per cent).

Amidst a strong dollar, currencies in developing countries have weakened significantly. Most South Asian currencies, including the Bangladesh Taka, have lost significant value in recent weeks which could further fuel imported inflation (food and energy), increase debt servicing costs, and rise in financial instability. The volatility in the exchange rate market makes Bangladesh's hard-earned macroeconomic stability at stake. Nevertheless, compared to most South Asian economies, Bangladesh's natural gas which comprised 69 per cent of the country's primary energy mix, takes some pressure off the dwindling foreign exchange reserves.

INFLATION EXPECTATIONS: A few points to ponder on households' inflation expectations. The ongoing high inflation regime is largely manifested in the goods sector. A study indicates goods inflation is predominantly transitory. However, as pandemic restrictions ease, the demand for services backed by pent-up savings rises keeping pressure on prices. However, the elephant in the room is the oil price. Academic studies suggest that "oil shocks are historically known to fuel inflation expectations and dis-anchor the expectations of both consumers and price setters."

A study by World Bank shows that in both advanced economies and EMDEs, long-term (five-year-ahead) inflation expectations fell during the past three decades. However, in recent times, among EMDEs, there has been a marked increase in inflation expectations, notably in Central Asia, Latin America, and South Asia, largely perpetuated by the effects of higher food and energy prices and currency depreciation. The Bangladesh Capital Market Sentiment Survey 2022 by LankaBangla Securities shows that inflation would be the biggest risk to the Bangladesh economy, with 83 per cent of respondents seeing elevated inflation. Bangladesh Bank's inflation expectation survey shows around 77 per cent of the respondents expect one-year-ahead average inflation to be above 6 per cent in 2022.

Both in Europe and in the US inflation expectations have increased. The April 2022 Survey of Consumer Expectations in the U.S. shows that inflation expectations are 6.3 per cent at the one-year horizon and 3.9 per cent at the three-year horizon.

The fear of inflation overshooting is gaining ground among top economists. Nobel laureate economist Paul Krugman has discarded his earlier stance that inflation would be transitory. He now believes that "rising prices will get worse before they get better. There's still a lot of inflation in the pipeline."

Risk of wage-price spiral. Both in advanced countries and EMDEs, households' and firms' near-term expectations of inflation have increased, while long-term expectations are at best mixed. Agusti?n Carstens of the Bank for International Settlements (BIS) observed that "while the message is more mixed regarding longer-term inflation expectations, it is not a source of much comfort. When inflation starts affecting the cost of living, it is more likely to take centre stage in price- and wage-setting decisions, triggering a dangerous wage-price spiral."

SOFT OR HARD LANDING: There is little consensus among central bankers and economists as to how the ongoing inflation will eventually come down. There is a fear of stagflation, a cruel mix of high prices and low growth. The International Monetary Fund (IMF) slashes global growth to 3.3 per cent for 2022, down from 4.1 per cent, while foresees elevated inflation of 6.2 per cent, a 2.25 percentage points higher.

Amidst over hitting of the US economy with a tight labour market (below 4 per cent unemployment) and 8 per cent inflation, Alex Domash and Larry Summers of Harvard University foresee a very substantial likelihood of recession over the next 12 to 24 months. They cite that since 1955, there has never been a quarter with average inflation above 4 per cent and unemployment below 5 per cent that was not followed by a recession within the next two years. Another Harvard Professor Jason Furman added that "there are very few examples in history that so-called soft landings (through interest rate hike) rarely helped to bring down inflation, and in cases where the inflation rate came down a lot, they're almost all hard landings (recessions). As far as Europe is concerned, the possibility of recession largely hinges on energy supply-- experts warn that a ban (or major disruption) on Russian gas would trigger one of the deepest recessions of recent decades in the eurozone.

The Head of IMF does not expect a recession for the world's major economies but also does not rule it out. Although its chief economist feels current growth forecasts (3.2 per cent global GDP growth) offer a buffer against a potential global recession.

In South Asia, India and Bangladesh are projected to outperform the average Gross Domestic Product (GDP) growth of emerging and developing Asia in 2022 and 2023. Both the countries are, however, likely to experience higher inflation during the same period.

It is still a little early to predict whether the global economy will plunge into recession. The conservative view is that "bringing inflation under control without a recession and large increase in unemployment will be challenging."

WAY FORWARD: High inflation matters; it is often associated with lower growth, financial crises, and political unrest. In its latest world economic outlook IMF cautioned, "...as advanced economies lift policy rates, risks to financial stability and EMDEs' capital flows, currencies, and fiscal positions- especially with debt levels having increased significantly in the past two years- may emerge."

Policymakers in Bangladesh now face extraordinary challenges to tame inflation. The scope of policy response is constrained by two key reasons. First: the drivers of ongoing inflation -- the pandemic, the war, supply chain disruption, sanctions, geopolitical factors etc -- are to large extent beyond the control of the country. Second: there are adverse developments in key macro variables, notably large "twin deficits" in the past few months: the consolidated fiscal balance (% of GDP) registered a large deficit of 5.2 per cent in December 2021. The external sector of the country also faces significant challenges owing to big gaps in export earnings and import payments and the slowdown in inward remittances. Bangladesh's current account deficit is projected to be 3.1 per cent of its GDP in 2022.

That being said, to limit the adverse impacts of inflation, there is still some scope for policy manoeuvre through monetary and fiscal policies aimed at limiting the impact of current inflation as well as anchoring medium- and longer-term expectations at moderate levels. The latter determines the effectiveness of fiscal and monetary policy and shapes realised inflation.

Monetary policy response. Nobel laureate Milton Friedman famously observed that "inflation is always and everywhere a monetary phenomenon." As such, monetary policy transmission through interest rate and exchange rate could play a crucial role in limiting inflation shock. In this regard, the central bank's credibility holds the key. Studies suggest that "inflation expectations are shaped by, among others, the history of inflation and the degree of credibility of the central bank."

One of the constraints is that the interest rate is largely administered rather than market-determined in Bangladesh. As a result, there are marked anomalies between policy rate, deposit rate, and lending rate. Currently, depositors are punished for savings with a negative real interest rate (deposit rate is 4 per cent and official inflation rate is over 6 per cent). Clearly, with this interest rate policy, it is challenging to manage aggregate demand in line with BB's inflation target. Tightening monetary conditions including credit growth in less productive sectors is advisable. Nevertheless, of other key variables, broad money (M2) growth in recent months has declined to below 10 per cent.

Given the nature of the exchange rate regime that Bangladesh Bank pursues the central bank has to intervene in the foreign exchange market when the impact of inflation is persistent. Amid the steady depreciation of most currencies of EMDEs vis-à-vis the US dollar, maintaining an appropriate level of exchange rate of Bangladesh Taka is imperative limiting the impact of imported inflation as well as sustaining export competitiveness. In recent weeks, there has been marked misalignment between the official and kerb market Taka-Dollar exchange rate, leading to volatilities in exchange rate markets. Since the pandemic, Bangladesh's real effective exchange rate (REER) appreciated about 7 per cent while the nominal effective exchange rate (NEER) index remained the same, indicating inflation in Bangladesh is higher than its trading partners, indicating exports have been more expensive and imports cheaper.

In addition, a World Bank study shows that "there is a risk of policy missteps if the pass-through, the effect of exchange rate changes on domestic inflation, is not properly evaluated, notably in EMDEs, where large currency movements are more frequent". As such, a correct assessment of the exchange rate pass-through ratio (ERPTR) to inflation, the percentage increase in consumer prices associated with a 1.0 per cent depreciation of the effective exchange rate, is advisable.

Fiscal measures. The priority of fiscal authorities should be protecting those struggling with the double whammy of the commodity price hikes and the pandemic-induced economic crisis through targeted food subsidies and safety net measures. The upward adjustment of energy prices should be delayed to suppress inflation and inflation expectations, although this could further increase the fiscal deficit. The austerity measures that have been introduced should be maintained until inflation is eased to Bangladesh Bank's targeted level. The forthcoming national budget is also critical to reduce tariff rates for essentials and elevate luxury items to control imports.

The signal (supported by actions) that both monetary and fiscal authorities need to give to the market is that they are determined to ease inflationary pressure as much as they can, even if that cost some growth limiting current inflation and anchoring medium-term inflation expectations.

Dr M Shahidul Islam is a Senior Research Fellow at the Centre for Governance Studies (CGS) and a Distinguished Fellow at Yunnan Academy of Social Sciences (YASS), China.shahid.imon@live.com

© 2026 - All Rights with The Financial Express