In recent times loan default has emerged as a topic of frequent discussions both in academic circles and the media. The issue is of great importance in view of the dominant role of the banking system in financing investment in the real sector in Bangladesh. The capital market has not yet reached a level where it serves as a major source of long-term finance. In consequence, investment, economic growth, employment creation and poverty alleviation are inextricably connected with the financial soundness of the banking system. However, the banking system of Bangladesh is currently under tremendous stress because of unbridled increase of loan default.

By way of introduction it should be mentioned that there are certain structural features of the banking system in any country which make it prone to loan default. First, asymmetry of information is pervasive in banking systems. This means that the banks as lenders do not have full information that borrowers possess about financial viability of projects while submitting loan applications. Moral hazard also is a typical characteristic of the banking systems. The banks harbour the notion that they will be bailed out in the event of any imminent collapse. This encourages adverse selection in that banks lend money to risky borrowers at higher rates of interest at the cost of potential borrowers with sound project proposals but unwilling to pay very high rate of interest. These considerations dictate the need for prudential supervision and sound corporate governance of the banking system.

In light of the above, this paper seeks to quantify the extent of default problem in Bangladesh, indicate the probable causes and suggest actions to deal with the problem.

In light of the above, this paper seeks to quantify the extent of default problem in Bangladesh, indicate the probable causes and suggest actions to deal with the problem.

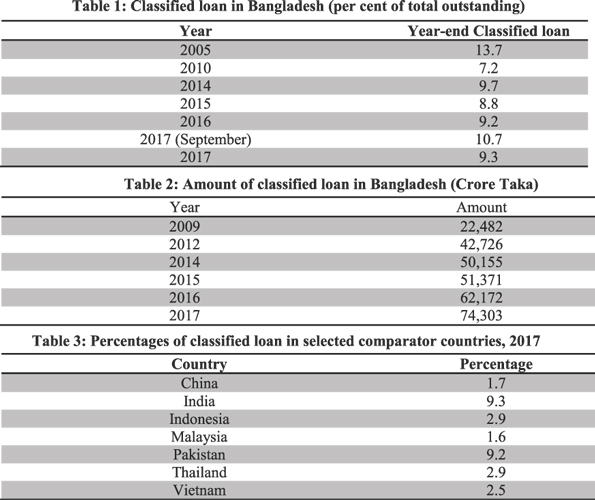

THE QUANTITATIVE DIMENSION: Non-performing loan as a proportion of outstanding loan which was 7.2 per cent in 2010, reached 10.7 per cent in September 2017. These numbers, however, understate the magnitude of the problem because these exclude the amounts rescheduled/ restructured or written off. As of September 2017, for example, an amount of TK 450 billion (45000 crores) was written off. In December 2017 non-performing loan ratio fell somewhat to 9.3 per cent (See table 1). Nevertheless, in absolute term the amount continued to grow. As of December 2017, the amount was TK 743.03 billion of 74303 crores (See table 2) of which 57 per cent was attributable to state-owned banks. Moreover, the non-performing loan ratio in Bangladesh is much higher than in our neighboring countries excepting India and Pakistan (See table 3).

THE UNDERLYING CAUSES: The following paragraphs indicate the causes underlying massive default. Two qualifications should be noted here. First, the discussion gives a general picture. All the causes are not necessarily relevant to all banks. Second, there is no pretention of assessing the relative importance of the various causes. More in-depth micro-level research is required in these respects.

(I) Incompetence of bank personnel: The incompetence of the bank personnel is reflected in several ways. The collaterals are improperly valued. The potential cash flows from the projects for which loans are given are not accurately assessed. Future revenue potentials of the borrowing companies in light of emerging domestic and external economic circumstances are not evaluated. There are sometimes mismatches between the loan maturity period and the time by which a project is expected to generate revenues. As a result, the borrowers who do not deserve loans are actually given loans and they fail to honor the terms of repayment. Appropriate follow-up with defaulters is often lacking.

(II) Poor governance: There are many indications of poor governance. Banks frequently engage in related lending. That means that loans are given to friends, relatives or politically connected people irrespective of the merit of their loan proposals. The choice of Board Members is not based on relevant qualifications. Audit Committees do not function independently. Risk Management Committees may be either nonexistent or do not function effectively. Board members are more concerned with approving specific loans or rescheduling/restructuring loans for favor people. There are also allegations of corruption against both Board Members and senior employees.

(III) Political influence: In many cases, loans are sanctioned in consequence of political influence. Rescheduling/restructuring decisions are also influenced by political considerations. The beneficiaries of such political influence frequently turn out to be perpetual defaulters. This problem is particularly acute for state-owned banks.

(IV) Ineffective judicial system: Thousands and thousands of cases are stuck up in the loan recovery courts. Many large defaulters manage to get stay orders from superior courts. As a result, recovery actions cannot be effectively implemented in a timely manner. This encourages borrowers to continue to default on new as well as rescheduled/restructured loans, fortified by a sense of impunity.

(V) Miscellaneous causes: Among the other factors cited by analysts are the ineffective enforcement of prudential norms by the central bank, its inability to initiate preventive actions, the existence of too many banks which detracts for the economies of scale and sometimes leads to unhealthy practices, and directed lending for some specific purposes at preferential interest rates.

SOME ADVERSE CONSEQUENCES OF LOAN DEFAULT: Persistence of large amounts of defaults gives rise to a number of adverse consequences. People's confidence in banking system may become shaky leading to slowdown of growth of deposit to the detriment of the intermediation function of the system. The recent slowdown in the deposit growth in Bangladesh may be partly due to continuing high levels of defaults. Bank's income generation is unfavourably affected by defaults. As a result, they tend to charge higher interest rates on new loans to compensate for the loss of income from defaulted loans. The high interest rates, in turn, can adversely affect the competitiveness of the borrowing enterprises and aggravate default. The banks have to maintain larger provisions affecting their lending capacity. In some cases, they may fail to meet capital adequacy requirements and may engage in aggressive lending to undeserving borrowers.

THE WAY FORWARD: The causes cited above intrinsically suggest remedial actions for the future. A few are mentioned below without any claim to being exhaustive.

* First, the analytical competence of the bank staff has to be improved. They have to more skilled in assessing viability of the projects for which loans are sought, valuation of the collaterals, monitoring utilization of funds and maintain dialogue with the borrowers.

* Second, sound corporate governance of banks has to be ensured. The functions of the Boards and the Management staff have to be clearly specified. The boards should refrain from interfering in the functions supposed to be performed by the staff. The practice of related lending should be totally avoided. The Audit Committees and Risk Management Committees should be allowed to function autonomously.

* Third, the disposal of cases stuck up in courts has to be expedited. The Central Bank, the Finance Ministry and Attorney General's office should jointly seek help from the Honourable Chief Justice to achieve this objective.

* Fourth, there has to be a strong commitment by the political authorities to deal with the problem. There should be no political intervention in approval of loans, rescheduling/ restructuring and initiation of timely legal actions.

* Fifth, the Central Bank should make honest self-assessment of the effectiveness of its role as the designated guardian of the banking system. Such assessment should look into the number, the qualifications and professional competence of its staff, examine the legal loopholes which might constraint the exercise of its due role and take initiatives for appropriate remedies.

Dr. Mirza Azizul Islam is a former Adviser (Cabinet Minister) to the Caretaker Government, Ministries of Finance and Planning and presently a Professor at BRAC University. This paper is based on a keynote presentation at Bangladesh University of Professionals (BUP).

maislam@bracu.ac.bd

© 2026 - All Rights with The Financial Express