Md Rashel Hasan, Raju Ahmed, Md. Habibour Rahman and Mahmud Salahuddin Naser | March 17, 2022 00:00:00

The monetary conditions index (MCI) combines the effect of interest rates and exchange rates in a single indicator and can be used for assessing the overall monetary policy stance. This paper attempts to construct MCI for Bangladesh for the period 2004 to 2020 using monthly data. The weights of interest rate and exchange rate are derived from the aggregate demand framework using Johansen's cointegration techniques.

METHODOLOGY: MCI is defined as the weighted average sum of the changes in the interest rates and in the exchange rates in relation to the base period.

![]() where it is short-term interest rate and et is the exchange rate in period t respectively, and are interest rate and exchange rate, respectively, in a given base period, wr and we are weights of the interest rate and exchange rate express the impacts of those parameters on policy goal such as output growth or inflation. Both interest rate and the exchange rate could be either in nominal or real term, however, estimated MCIs derived from nominal or real terms would have similar movements in the short-run as relative prices and inflation rates are reasonably the same (Eika et al (1996)).

where it is short-term interest rate and et is the exchange rate in period t respectively, and are interest rate and exchange rate, respectively, in a given base period, wr and we are weights of the interest rate and exchange rate express the impacts of those parameters on policy goal such as output growth or inflation. Both interest rate and the exchange rate could be either in nominal or real term, however, estimated MCIs derived from nominal or real terms would have similar movements in the short-run as relative prices and inflation rates are reasonably the same (Eika et al (1996)).

The construction of MCI is involved in several steps. At first, we need to estimate the weights of the exchange rate and the interest rate as those are not directly observable. The literature addresses various methods to estimate those weights using econometric techniques. The most commonly used theoretical models are aggregate demand equation or price equation (IMF, OECD, Deutsche Bank estimated MCI using these approaches). Kannan and Bhoi (2006) also exploited the aggregate demand model to estimate weights of interest rate and exchange rate for the Indian economy. As a small open economy like Bangladesh, both interest rate and exchange rate can be considered as policy variables in the monetary transmission process. Moreover, changes in the interest rate and exchange rate can significantly influence both domestic demand and export earnings (external sector heavily dependent on export, more than 80 per cent of external income is coming from export). To quantify the relative importance of interest rate and exchange rate, we exploited the aggregate demand model. As the relationship among output, interest rate and exchange rate may be dynamic in nature and all the three variables exhibited having unit-roots, we applied Johansen's co-integration technique to reveal both short-term and long-term relationship among them. Aggregate demand equation can be expressed as below:

![]() where yt is aggregate demand, it is short-term interest rate, et is the exchange rate et is the error term.

where yt is aggregate demand, it is short-term interest rate, et is the exchange rate et is the error term.

DATA: Data of the selected variables namely lending rate, exchange rate and quantum index are observed on a monthly basis from July 2004 to August 2020. It may be noted that a market based floating exchange rate has been introduced in the mid of 2003. The study period has been incorporated since 2004 to capture the effect of market-based exchange on the economy. The lending rate was used as a proxy variable to track the interest rate channel of the monetary policy transmission mechanism. The bilateral nominal exchange rate has been employed to capture the exchange rate channel. Both weighted average lending rate and nominal exchange rate have been collected from Bangladesh Bank's various publications. Quantum index of manufacturing industries has been used as a proxy of gross domestic product (GDP) to quantify economic activities (GDP is available annual basis only). Data on the quantum index has been incorporated from the Bangladesh Bureau of Statistics.

MODEL SPECIFICATION: As discussed earlier, we need to have relative weights of interest rate and exchange rate to construct MCI. In order to estimate weights of interest rate and exchange rate, we rely on the output model which is shown in the following equation (3):

![]() Where logQt is the quantum index for manufacturing industries in logarithm form for time t, LR is the weighted average lending rate, log_exch refers to nominal exchange rate taka per USD in logarithm form, B’s are the parameters to be estimated and are error term.

Where logQt is the quantum index for manufacturing industries in logarithm form for time t, LR is the weighted average lending rate, log_exch refers to nominal exchange rate taka per USD in logarithm form, B’s are the parameters to be estimated and are error term.

TESTING STATIONARITY OF THE DATA: The property of data, whether it has unit root or not, is checked by the standard ADF method and Phillips-Perron unit root test. All data series except lending rate are in natural logarithm. The result reported in Table 3 indicate that all the series are not stationary evident by both the ADF test and PP test. However, the first difference of each of the data series shows stationary at 1 per cent significance level according to both ADF and PP test.

COINTEGRATION ANALYSIS: As data series can be made stationary after first differencing, there is a possibility that data series might have a co-integration relationship in the long-run. We can apply Johansen (1988, 1990) techniques to test the co-integration relationship among the variables (output, interest rate and exchange rate). Before applying co-integration technique, selection of appropriate lag length is very important. Optimal lag length can be determined with the help of the unrestricted VAR model. After running unrestricted VAR, optimal lags have been selected as 1 on the basis of Schwarz Criterion (SC). Johansen's cointegration technique that uses both maximum eigenvalue and trace statistics has determined the existence of one co-integrating vector. Table 2 displays test statistics values that can be obtained from both rank test and trace tests.

COINTEGRATION ANALYSIS: As data series can be made stationary after first differencing, there is a possibility that data series might have a co-integration relationship in the long-run. We can apply Johansen (1988, 1990) techniques to test the co-integration relationship among the variables (output, interest rate and exchange rate). Before applying co-integration technique, selection of appropriate lag length is very important. Optimal lag length can be determined with the help of the unrestricted VAR model. After running unrestricted VAR, optimal lags have been selected as 1 on the basis of Schwarz Criterion (SC). Johansen's cointegration technique that uses both maximum eigenvalue and trace statistics has determined the existence of one co-integrating vector. Table 2 displays test statistics values that can be obtained from both rank test and trace tests.

Based on the normalised value that we got from the first cointegrating analysis can be represented in the following equation:

![]() Both the coefficients exhibit expected signs and turned out to be statistically significant (values in the parentheses are standard error). That is an increase in lending rate lowers aggregate demand. On the other hand, an increase in nominal exchange rate measured as taka per USD (depreciation) has positive impact on aggregate demand. From this estimated model we can obtain weights of rate of interest and exchange rate. From equation (3), the weights for interest rate (wr) and exchange rate (we ) suggests to be 0.65 [(wr/(wr+we)] and 0.35 [(wr/(wr+we)], respectively. The estimated monetary condition ratio is about 1.86:1 (wr/we) which implies that a 1.0 percentage point rise (100

Both the coefficients exhibit expected signs and turned out to be statistically significant (values in the parentheses are standard error). That is an increase in lending rate lowers aggregate demand. On the other hand, an increase in nominal exchange rate measured as taka per USD (depreciation) has positive impact on aggregate demand. From this estimated model we can obtain weights of rate of interest and exchange rate. From equation (3), the weights for interest rate (wr) and exchange rate (we ) suggests to be 0.65 [(wr/(wr+we)] and 0.35 [(wr/(wr+we)], respectively. The estimated monetary condition ratio is about 1.86:1 (wr/we) which implies that a 1.0 percentage point rise (100  basis points) in the interest rate or a 1.86 percent increase (depreciation) in the exchange rate has about the same effects over time on aggregate demand. That implies interest rate channel is more powerful than exchange rate channel to influence aggregate demand in Bangladesh. Kannan (2006) who exploited output model for India and also found interest rate channel is superior to exchange rate (estimated ratio of interest rate and exchange rate was 1.36:1 for India). Moreover, Younus (2012) exploited inflation model to estimate relative weight of interest rate and exchange rate and found the ratio 4.88:1 for Bangladesh during January 2004 to March 2011.

basis points) in the interest rate or a 1.86 percent increase (depreciation) in the exchange rate has about the same effects over time on aggregate demand. That implies interest rate channel is more powerful than exchange rate channel to influence aggregate demand in Bangladesh. Kannan (2006) who exploited output model for India and also found interest rate channel is superior to exchange rate (estimated ratio of interest rate and exchange rate was 1.36:1 for India). Moreover, Younus (2012) exploited inflation model to estimate relative weight of interest rate and exchange rate and found the ratio 4.88:1 for Bangladesh during January 2004 to March 2011.

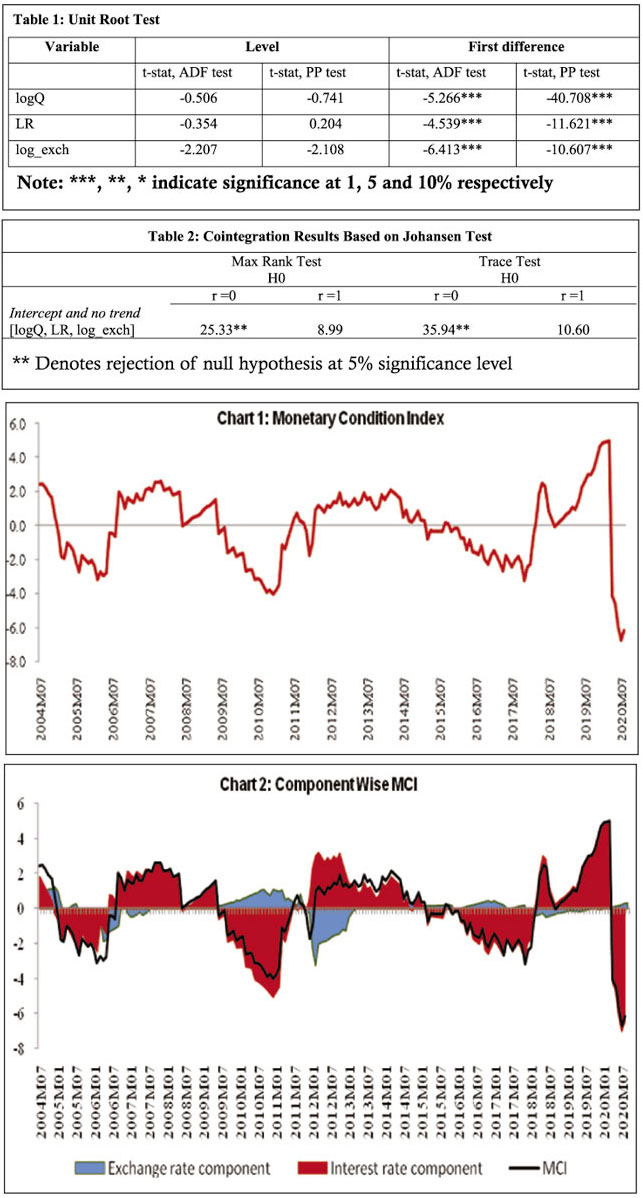

MOVEMENTS OF THE MCI, IMPLICATIONS AND INTERPRETATIONS: By using estimated weights that we obtained in the preceding section, a monetary condition index has been prepared. While calculating MCI, the common practice is to deduct the actual value of interest rate and exchange rate from that of a specified base period as shown in eq(1). However, few studies also use the deviation of interest rate and exchange rate from their equilibrium levels. This study tried to estimate the equilibrium level of interest rate and exchange rate by using Hodrick-Prescott (HP) filter as did by CNB bank. This would provide the possibilities to compare any situation with the equilibrium and to conclude whether or not the monetary conditions in the period have been too tight or too loose compared with the equilibrium period. By using the relative weight of interest rate and the exchange rate of 0.65 and 0.35 respectively, MCI values have been calculated using equation (1). Thus a rise in MCI values refer to an indication of tight monetary condition and a fall in MCI values indicates an easing of the monetary condition. [While calculating MCI using equation (1), nominal exchange rate has been used as dollar per taka. So an increase in the exchange rate indicates domestic currency appreciation and thus higher interest rate and currency appreciation will resultant higher MCI (that is, tight monetary condition). MCI values close to zero indicates a neutral monetary condition.]

Based on the values of MCI, chart 1 displays different phases of the monetary conditions in Bangladesh. The development of the MCI shows that there are seven distinct phases of monetary condition during July 2004 to August 2020 of which four phases indicate ease monetary conditions and three show tight monetary conditions.

Phase I. The downward movement of MCI since the beginning of 2005 until mid-2006 indicates an easy monetary policy stance. Bangladesh economy was adversely affected by the 2004 flood. Accordingly, the monetary policy stance in 2005 has been supportive of growth reflecting in part by increased lending to the agricultural sector for flood rehabilitation. But an accommodative stance generated pressures on the exchange market leading to a sharp fall in the nominal exchange rate (depreciation) exacerbated further by the aftershock of the introduction of the market-based floating exchange rate in May 2003. [Since the introduction of floating the exchange rate in 2003, the authorities have confined their interventions to counter disorderly market conditions. The foreign exchange market, however, had been truly tested in early 2005 when the economy was confronted by multiple external shocks i.e. global fuel oil and commodity price shocks. To ease the pressure, Bangladesh Bank sold foreign exchange reserves in January 2005 while allowing the taka to depreciate by 5 percent against the U.S. dollar.]

At the same time, Bangladesh economy faced with an upswing in global oil and commodity price that contributed to a surge in inflation. Subsequently, a tighter monetary policy stance was essential to ensure price stability and orderly exchange market conditions. Monetary tightening came in the form of an upward adjustment of repo interest rate and Cash Reserve Requirement (CRR).

Phase II & III. As depicted by the upward MCI, the monetary conditions were tight in most of the period in FY2006-FY2009 with GDP growth remained firmed spurred by strong growth of export and remittances. But inflation remained uncomfortably high due to multiple natural disasters and elevated international food and fuel prices. Government and private sector credit growth soared during the period due to the need to finance rice procurement from domestic markets and imports from international markets. With short-term government securities rates increased gradually, banks lending and deposits interest rates have seen a modest increase creating tight monetary conditions at that point. The real effective exchange rate appreciated somewhat in this period as a result of domestic inflation. Responding to the situation, Bangladesh Bank has kept the dollar exchange rate stable to guard against intensifying imported inflation pressures. The concerns of the global economic downturn since 2008 prompted Bangladesh Bank like many central banks to pursue an easy monetary policy that facilitated the process of the economic recovery that traced till the start of 2011. Monetary conditions were increasingly loosened as shown by a falling MCI during FY09-FY10. The improvement in the current account at that period put upward pressure on taka which Bangladesh Bank countered through unsterilized foreign exchange purchases. The injection of liquidity from unsterilised interventions caused the bank's excess reserves to rise sharply, pushing interest rates below.

Phase IV. The continued pursuance of easy monetary policy helped to recover growth. But the resulted growth pressures along with rising crude oil and other commodity price fuelled inflationary spirals warranting Bangladesh Bank to pursue preemptive monetary tightening since 2011. Lending rate caps for most of the types were lifted in March 2011, with a subsequent 200-300 basis points rise in their base rates. Bank-by-bank credit to deposit ratio (CDR) ceiling was imposed around the same time. The MCI started to pick-up strongly from early 2012 until reaching its pick at the beginning of 2014. The monetary tightening was a result of the rise in both the real interest rate and the exchange rate. Repo interest rate was raised by 100 basis points. Moreover, the rising of CRR by 50 basis points in June 2014 was also attributable to such tight episode.

Phase V & VI. Against global headwinds and episodes of domestic political turmoil and uncertainty, domestic demand and activity have weakened markedly in the second half of FY15. However, headline inflation eased in part by favourable agricultural production and falling global commodity prices. In the meantime, the current account balance turned into a deficit due to slower exports, higher imports and a decline in remittances. Repo interest rate was reduced a couple of times to boost credit growth. During FY18 private credit growth picked-up strongly. In response, Bangladesh Bank reduced the maximum advances-to-deposit ratio (ADR). The CRR was also increased by 50 basis points. With liquidity tightening, deposit and lending rates have begun to increase in 2018. The adverse impact of high issuance of higher interest-bearing National Savings Certificates (NSCs) and growing non-performing loans kept the upward pressure on interest rates. The high level of stressed assets narrowed banks' ability to engage in new lending and constrained access to credit thereby generating tight monetary conditions well traced by the upward movement of the MCI curve.

Phase VII. Domestic activities started to decline as the COVID-19 pandemic concentrated in the last quarter of FY20 and the first quarter of FY21.The government and Bangladesh Bank have announced a series of stimulus package with a total size of over Taka 1.21 trillion (about 4 percent of GDP). Bangladesh Bank moved rapidly to provide the necessary flow of credit to support the economy functioning. Bangladesh Bank has eased monetary policy by lowering the repo interest rate and the CRR, expanded provision of the repo facility, initiated the outright purchase of t-bills, raised Advance-Deposit Ratio (ADR) to facilitate credit to the private sector and improve liquidity in the banking system. Liquidity provision in the foreign exchange market was eased by selling USD by Bangladesh Bank. The easy monetary conditions are reflected by the sharp fall in the MCI since March 2020.

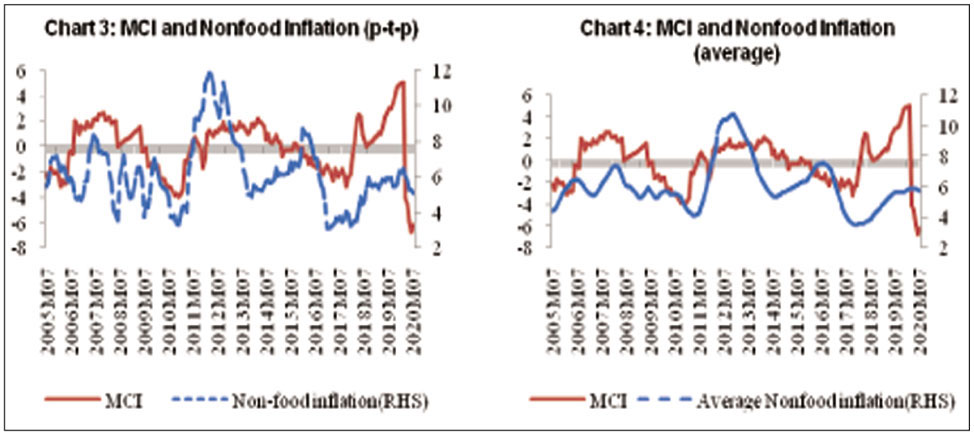

Relative strength of exchange rate and interest rate on the MCI is shown in Chart 2. It shows that the index movement is mostly subject to the movement in interest rate and for some period exchange rate was moving in the opposites direction, off-setting the affect of the interest rate.

Finally, Charts 3 and 4 represent the movement of MCI and nonfood inflation. The Charts show that, in most of the cases, higher MCI values is associated with falling nonfood inflation.

CONCLUSION: The study focuses on the contribution of MCI for Bangladesh and its application to the Bangladesh economy. The MCI derived in this study appears to indicate the actual monetary policy stance. The different phases of monetary tightening or easing in the context of Bangladesh can be better captured by the MCI compared to the trends in the interest rate or the exchange rate alone. Although Younus (2012) estimated the monetary condition index for Bangladesh over the period January 2004 to March 2011, our paper differs and adds values to the existing literature in several ways. Firstly, Younus (2012) exploited the inflation model to estimate relative weights of interest rates and exchange rate though, the effect of interest rate and the exchange rate is viewed as equally important influencing output in small open economies (Kannan 2006, Hyder 2006). In this paper, we introduced an aggregate demand model to estimate the relative weights of interest rate and exchange rate from July 2004 to August 2020. Our results suggest that the weight of the interest rate and the exchange rate is 0.65 and 0.35 respectively. And the estimated monetary condition ratio is 1.86:1, implying that a 1.0 percentage point rise (100 basis points) in the interest rate or a 1.86 percent increase (depreciation) in the exchange rate has about the same effects over time on aggregate demand. That implies that the interest rate channel is stronger than the exchange rate channel in influencing monetary conditions in Bangladesh. Younus (2012) found the monetary condition ratio as 4.88:1 indicating interest rate channel even stronger during 2004-2011 based on the inflation model. Secondly, calculating MCI is generally based on deducting the actual value of the interest rate and exchange rate from that of a specified base period. In such a case, the movement in MCI (up or down) needs to be compared to that base period. However, few papers also do the deviation of interest rate and exchange rate from their equilibrium levels (for instance, the Czech National Bank (CNB) in their inflation report published in the second quarter of 2015 utilised that technique). MCI that uses the deviation of interest rate and exchange rate from their equilibrium level makes it possible to compare the movement of MCI of a specific time point relative to the same time point. This paper tried to estimate the equilibrium level of interest rate and exchange rate by using Hodrick-Prescott (HP) filter as did by CNB bank and finally obtained MCI values.

Obtained estimates of MCI using the weights of interest rate and exchange rate suggest that in the observed period monetary policy in Bangladesh was mostly expansionary, as reflected by easing monetary condition. The paper also identifies four tight and three soft episodes of monetary policy stance from July 2004 to August 2020. Furthermore, our findings show that the movements between MCI and inflation are broadly opposite, suggesting that cautionary monetary policy might able to tame inflation to some extent.

Thus MCI can be used as an indicator of monetary policy decision-making as a technical instrument alongside other indicators. Bangladesh Bank can use the MCI as an indicator in monetary policy analysis. In this capacity, Bangladesh Bank would not use monetary policy tools to adjust the level of the index to the desired path, but rather it would help to inform policymakers of the current stance of monetary conditions, and whether they are tighter or easier relative to other periods.

The authors are from the Chief Economist's Unit and the Governor Secretariat of Bangladesh Bank. rashel.hasan@bb.org.bd

© 2026 - All Rights with The Financial Express