Amidst this coronavirus outbreak, the Government of Bangladesh has announced a number of stimulus packages for different sectors and beneficiaries. There are so far at least seven major stimulus packages declared by the Government and are to be distributed by the banking sector under the guidance of Bangladesh Bank circulars to support the economy through these unprecedented challenging times.

In order to ease liquidity in the banking sector to support these stimulus schemes, the central bank has taken a number of swift steps by using the monetary policy tools. Cash Reserve Ratio (CRR) has been reduced by 1.5% .The repo rate has also been reduced by 75 basis points in two stages. Advance to Deposit Ratio (ADR) threshold has also been increased by Bangladesh Bank. In addition to these policy tools, the central bank is also refinancing a lion's share of these mammoth schemes.

Since the disbursements are being conducted through the banking sector whereby the commercial banks have to assume credit risk, the schemes pose additional risk management and administrative responsibilities on the banks. In the advent of economic shock, the borrowers who would primarily need additional support are probably the ones who are more susceptible to default.

Thus, it might just be a question of who gets access to the loans; the ones who need the most? Or the ones who have the credibility?

An explanation on the various financial stimulus packages might provide an insight into the impact on the banking sector in Bangladesh.

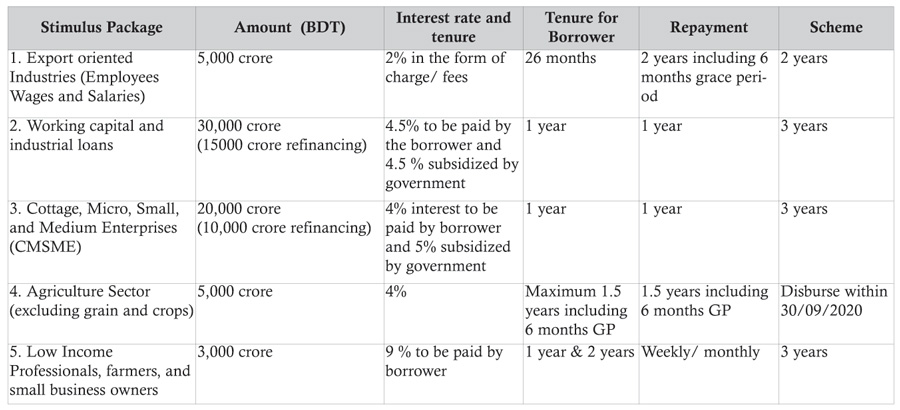

The table below summarizes the six major stimulus packages and key features:

Tk. 5,000 crore stimulus package for payment of wages and salaries by export-oriented industries has already been availed by majority of the companies. Under this scheme, the borrowers can avail loans for payment of wages and salaries of their workers for the months of April, May, and June. After a grace period of six months, the borrowers will repay the loan in 18 equal monthly installments from January, 2021 till June, 2022. The borrowers will not be charged with any interest/profit on this loan; rather, they will be charged a one-off 2% service charge on the loan amount. In order to provide the market with liquidity to support the scheme, Bangladesh Bank will provide the BDT 5,000 crore funds.

Tk. 5,000 crore stimulus package for payment of wages and salaries by export-oriented industries has already been availed by majority of the companies. Under this scheme, the borrowers can avail loans for payment of wages and salaries of their workers for the months of April, May, and June. After a grace period of six months, the borrowers will repay the loan in 18 equal monthly installments from January, 2021 till June, 2022. The borrowers will not be charged with any interest/profit on this loan; rather, they will be charged a one-off 2% service charge on the loan amount. In order to provide the market with liquidity to support the scheme, Bangladesh Bank will provide the BDT 5,000 crore funds.

While the banks will not face any liquidity issue, the return on capital is expected to be quite low considering the slim margin. However, most commercial banks already have an exposure to the RMG sector and they are providing this loan under this scheme to support the industry towards recovery as they have pre-existing credit exposure on the industry. The banking industry is in any case tormented by the swelling non-performing loans (NPLs). If the RMG industry and its backward linkage industries fail due to the contraction of the global economy, then it is only evitable that the NPLs will increase sharply.

The second package is for working capital loan to industrial and service sector. This will be in the form of medium term stimulus package as the scheme will operate for 3 years where the loan tenure for each borrower would be maximum 1 year. While the banks can lend at existing 9% interest rate, government will subsidize 4.5% while the borrower has to bear the remaining interest burden of 4.5%. Majority of affected businessesare expected to avail this loan due to impact of the disruption in the global and local supply chains on their liquidity. Bangladesh Bank has formed a Revolving Refinance Scheme of Tk 15,000 crore to support the banking sector with liquidity to refinance up to 50% of this scheme at 4% interest rate charged to the banks.

The third package is to support the Cottage, Micro, Small, and Medium Enterprises (CMSME) which are the most affected due to this pandemic. The government has declared a Tk. 20,000 crore stimulus fund for this sector. The modus operandi is similar to working capital loans to industrial and service sector, with some minor tweaks. Bangladesh Bank has formed a Revolving Refinance Scheme of Tk. 10,000 crore to support the banking sector with liquidity to refinance up to 50% of this scheme at 4% interest rate charged to the banks. While, the government has declared Tk. 20,000 crore financial package to the SME sector at a subsidized rate, loans to SMEs are mostly given against tangible collateral (e.g. property) since there isn't a robust cash flow analysis available. But in times of crisis, like the one currently playing out, the SMEs are struggling to survive during this pandemic and with the slowdown of the business, it is even less likely for them to be able to repay the loans at the right time. Under this circumstance, the banks will be reluctant to provide unsecured loans unless provided with some kind of guarantees, even if that is partial.

Other countries like in India, the government is only required to provide a partial guarantee on bank loans based on an assessment by lending banks, guided by parameters set by RBI. Even in Malaysia, the government is providing US$453 million subsidized loans to SME with 80% credit guarantee.

While the credit guarantee has its own flaws in terms of default risks and moral hazards and have not been successful in many cases, some form of risk mitigation mechanism should be undertaken to protect the SMEs and encourage commercials banks to lend to SMEs. While asked about the impact on the banking sector, Mr. Mamun Rashid, managing partner, PWC, a banker and economic analyst mentioned,

"Banks will be under pressure in absence of credit guarantee scheme especially for SME facilitation. There is also capacity constraint to reach out to new clients distressed by Covid 19."

The fourth package of BDT 5,000 crore to support lending to agricultural sector excluding crops and grains (e.g. horticulture, fisheries, poultry, dairy and livestock) will be provided to avoid any adverse in this sector from the ongoing crisis. Under this scheme, Bangladesh Bank has set up a refinancing scheme of BDT 5,000 crore under which banks can disburse loans to affected parties in the industry. The loan tenure can be maximum 18 months including a grace period of 6 months. Interest/profit rate to be charged to the borrowers will be 4% and Bangladesh Bank will charge the banks at 1% interest/profit rate for this scheme.

Meanwhile, existing support to import-substitute crops through priority sector lending under Bangladesh Bank is expected to continue and can now include paddy, wheat and other grains, profitable crops, vegetables etc.This financial support will facilitate access to finance to run the supply chain , and help the generation of output for the farmers.

The fifth package of BDT 3,000 crore will be used to support low income professionals, farmers, and small business owners. Under this scheme, Bangladesh Bank will provide a revolving refinance scheme to the banks, under which banks can lend to Microfinance institutions (MFIs) certified by Microcredit Regulatory Authority (MRA). MFIs will be responsible for disbursement of loans by following the strict guidance of the circulars to affected parties eligible for this loan. Loan tenure will be maximum one year for micro-credit and maximum two years for micro-entrepreneurs including grace period. Under this scheme, MFIs can charge interest/profit rate of 9% to borrowers, banks can charge 3.5% to MFIs, and Bangladesh Bank will charge 1% to banks under revolving refinance schemes.

The sixth package is theadditional Tk 12,750 crore (USD 1.5 Billion) allocated under the Export Development Fund (EDF) of Bangladesh Bank to facilitate raw materials imports under back-to-back Letter of Credit. The interest rate was reduced to 2% on 07 April, 2020.

In addition to the distribution of the aforementioned packages, Bangladesh Bank has also announced a number of other supports such as a BDT 5,000 crore pre-shipment finance scheme for export-oriented industries, suspension on recognition of interest income for the months of April and May which are to be transferred to blocked accounts, suspension on adverse classification till 30 June 2020, disbursement of BDT 2,500 each to 5 million poor families through Mobile Financial Services (MFS), and waiver to penal interest on delayed credit card bill payment. Among these, suspension of accrued interest in suspense account will result in a hit in the profit and loss accounts of the banks in the month of April and May; however, the banks are yet to receive further guidance on the treatment of this suspended interest accrual.

Lastly, the government also announced additional Tk. 2000 crore to assist migrant workers, unemployed youth and rural population during the economic crisis caused by this pandemic. Besides, an additional Tk. 5000 crore will be distributed as loan to the vulnerable groups through 4 state owned PalliShanchay Bank, Probashi Kalyan Bank, Karmasangsthan Bank and PKSF. This takes the total stimulus package to Tk. 1 trillion, which is 3.6% of the total GDP.

The response of the government in meeting the needs of various sectors of the economy does deserve appreciation. The impact of the pandemic at this point in time can only be assumed and forecasted. Reaching the stimulus packages to the right kind of beneficiaries while maintaining transparency and accountability is essential.

Dr. Melita Mehjabeen is associate professor at the Institute of Business Administration (IBA), University of Dhaka.She can be reached at

melitamehjabeen@gmail.com

© 2026 - All Rights with The Financial Express