"Extraordinary easy financing' conditions may pose 'upside risks' in the case of price stability in the upcoming quarters, the Bangladesh Bank (BB) report for the last quarter (Q4) of the immediate past financial year (FY), released on Tuesday, said.

The central bank in its quarterly publication noted that active vigilance and policy tuning are required for making a balance between growth recovery and price stability.

The quarterly said economic activities were shattered heavily, in the final quarter of the FY2019-20 due to an unprecedented lockdown clamped to contain the Covid-19 pandemic. The industry and service sectors were affected most, it said.

During this period (April-June 2020), industrial production dropped significantly, driven mostly by a precipitous fall in manufacturing output.

The service sector activities were stalled by the partial and often complete shutdown of transportation, trade, and hospitality industries, the quarterly noted.

But the agriculture sector maintained firm growth during this period, aided by the government's supportive initiatives, it added.

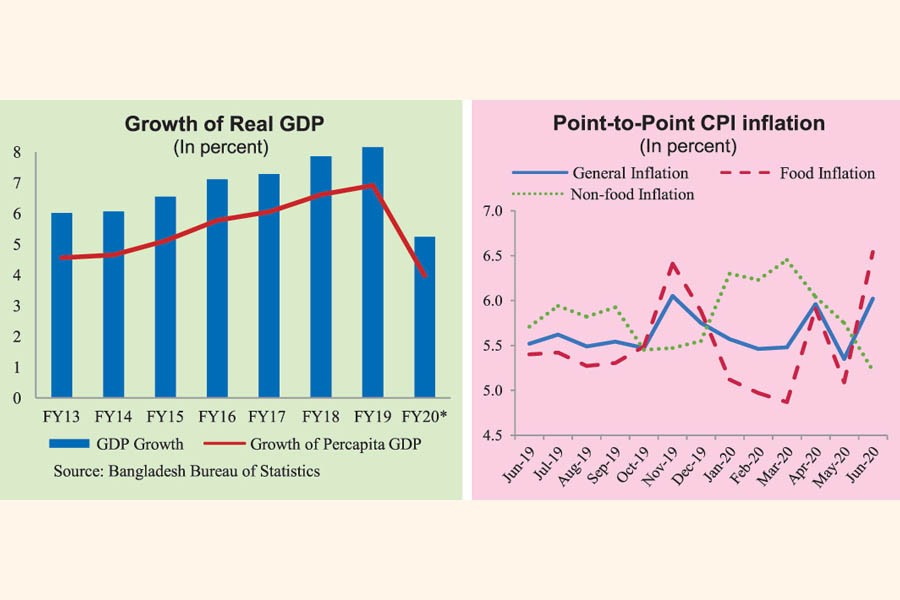

Nonetheless, the preliminary estimations by the Bangladesh Bureau of Statistics (BBS) suggested that real GDP growth dropped to 5.24 per cent in FY 20 from 8.15 per cent in FY 19.

The headline CPI inflation (point-to-point) increased to 6.02 per cent in Q4 of FY 20 from 5.48 per cent in Q3 amid some volatility, driven by a rise in food prices that emanated mostly from the pandemic-induced global and domestic supply chain disruptions.

The BB report said although food inflation witnessed a notable rise in Q4, non-food inflation remained moderate because of subdued demand of elastic items.

Accordingly, 12-month average inflation rose to 5.65 per cent in FY 20, whereas the target was 5.50 per cent.

In the quarter, the government's borrowings from the banking system increased following a slide in revenues, caused by economic fallout of the pandemic. It was accompanied by an uptick in net foreign asset that led to a broad money (M2) growth of 12.64 percent, close to the target for FY 20.

Credit growth to the private sector further moderated to 8.61 percent, which was far below the FY 20 target.

Interest rates in the inter-bank and retail markets witnessed a downward movement in the quarter because of reduction in both the repo rate and cash reserve ratio (CRR) by 50 basis points and 100 basis points, respectively.

The BB report mentioned that among other indicators related to the banking sector, the ratio of gross non-performing loans (NPLs) edged up to 9.16 percent in Q4 of FY 20 compared to the level of Q3.

Current account deficit (CAD) widened to an eight-quarter high of US$ 2.4 billion in Q4, resulted from a sharper fall of exports than imports, triggered by the pandemic.

Nevertheless, the overall balance of payment (BOP) witnessed a surplus of $3.3 billion in this period, bolstered by the record high quarterly financial inflows of $5.2 billion.

Nominal exchange rate of BDT against US dollar remained broadly stable owing to net purchase of dollars from the foreign exchange market by the BB.

On the fiscal side, budget deficit rose significantly in Q4 of FY 20, and about 70 per cent of the deficit financing was met from domestic sources (banks and non-bank).

Looking ahead, growth outlook is positive, as lockdown measures are being lifted in the domestic economy as well as in the advanced and emerging market economies, the BB report opined.

Moreover, a range of expansionary fiscal and monetary policies are likely to boost economic activities in full swing in near future.

jasimharoon@yahoo.com

© 2026 - All Rights with The Financial Express