The interbank foreign exchange spot market remains almost inactive despite recent changes in the exchange rate mechanism that included the introduction of a reference rate-driven system.

To make the forex spot market more vibrant, the central bank on December 31 last year introduced a reference-centric exchange rate mechanism to bring stability in the then volatile foreign exchange market, ending virtually an inefficacious crawling peg experiment.

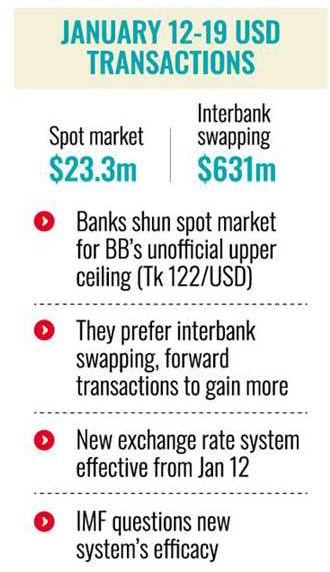

After observing the first six days of the spot market since the new system was applied on January 12 this year, it was found that the market where banks make outright transactions in US dollars remained almost inactive.

As there is an unofficial upper ceiling in forex buy-sell in the interbank market, many commercial banks try to avoid the highly-regulated spot market and largely trade their precious dollars through byways like interbank swapping and forward transactions to gain more.

Even the International Monetary Fund (IMF) representatives very recently in a virtual meeting with the banking regulator's high-ups raised questions over the new system's effective functioning.

According to the Bangladesh Bank (BB) data, banks made outright transactions in dollars of $23.3 million in the spot market from January 12 to 19 while $631 million was traded through interbank swapping, an arrangement where the taka-dollar exchange rate is not applicable.

Market players blamed the unofficial upper ceiling (Tk 122 a dollar) monitored by the central bank behind the commercial lenders' apathy to go for outright transactions in the American greenback.

Seeking anonymity, a central bank official said they launched a more flexible and reference-centric exchange rate mechanism a few days ago to stabilise the market. "Now the market is stable after the recent volatility."

When the official's attention was drawn to banks' lesser concentration on the spot market and over-reliance on swapping and forward deals, he said, "Give us some time as the Bangladesh Bank is working on the matter."

This correspondent talked to half a dozen bank executives, including managing directors and treasury officials, over the changing foreign currency management patterns. All of them agreed to share their thoughts on condition of not disclosing their identities.

The treasury head of a private commercial bank said the forex market would not be stabilised unless the spot market is vibrant. "Under the current context, the expected level of vibrancy will not come if the virtual cap on the exchange rate is not removed."

He said the interbank currency swap is an arrangement where a bank lends foreign currencies to another bank having dollar shortages for a short period with a provision of swapping back the same amount to the lending bank once the time is over.

"By doing so, banks are gaining more by keeping their dollars in hand," he said, adding forward transactions in dollars in the banking system went up significantly in recent days, which indicates that banks' concentration has switched from spot market trading.

A forward transaction is a binding agreement between two parties to exchange an asset at a predetermined price and date in the future within 90 days. Forward transactions are also known as forward contracts.

Another treasury head of a commercial bank said there are some banks that purchased more dollars during the volatile period and engaged in large forward deals. "By doing so, they fell short in forex requirements and bought more dollars from the spot market before going for fresh forward transactions."

"Through forward transactions, banks can gain higher prices of the greenback. I think the central bank should collect forward deal-related data regularly to better understand the situation," the official added.

jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express