Even during the 1980s, many relatives of Bangladeshi expatriates had to travel to Dhaka to withdraw remittances from Sonali Bank's foreign-exchange branch in Dilkusha. Imagine the toils involved: relatives navigating the bustling capital city to collect the hard-earned money sent by their loved ones abroad. The cost, time, and energy required for such trips added to their challenges. At that time, the median yearly remittance was merely around US$600 million, and private-sector banks were scarce. This, however, now goes down as a chapter of history.

Remittances grew significantly during the 1990s, driven by massive privatization of the financial system. Over the decade, annual remittances had increased from less than US$1.0 billion to nearly US$2.0 billion on average.

Thereafter came a remittance surge by the 2000s, with the figure reaching, on average, nearly US$11 billion per annum. During the 2010s, with the introduction of agent banking, remittances overshot the US$11-billion mark to nearly US$24 billion annually by now.

While a detailed quantitative analysis is necessary to fully understand the factors driving this growth, one thing is evident: accessing remittance funds has become significantly easier in recent decades, marking a remarkable evolution in Bangladesh's remittance history since 1975-76.

Agent banking: A rural game-changer: Agent banking has significantly simplified access to remittance funds, even in far-flung rural areas. During the July-September 2024 quarter, more than 9.0 per cent of inward remittances were channeled through agent banking, amounting to Tk 73,462.82 million (over Tk 73 billion).

This system is instrumental in revitalizing rural economies by addressing challenges such as travel costs, time loss, and logistical hurdles. It especially benefits women whose spouses are abroad and young dependents, providing convenient and timely access to financial resources.

This system not only ensures easier access to cash for rural relatives or dependents of expatriates but also reduces different types of costs. Previously, the recipients had to travel to Upazila headquarters to withdraw the money, incurring transportation costs, losing time, and facing numerous hassles-especially women whose husbands are abroad or young dependents.

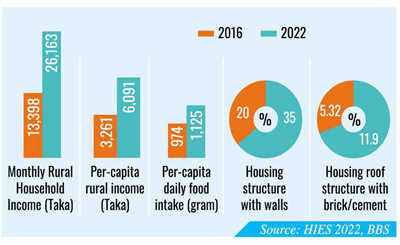

Positive impacts on rural development: The easy access to remittances has far-reaching implications for rural development of Bangladesh. For instance, household Income: monthly household income rose from Tk 13,398 in 2016 to Tk 26,163 in 2022, according to the Household Income and Expenditure Survey (HIES).

Per-capita rural income: Rural per-capita income doubled from Tk 3,261 in 2016 to Tk 6,091 in 2022, based on the HIES data.

Improved housing: Housing structures have seen a substantial facelift in once-backwater villages. In 2016, only 5.32 per cent of rural homes had roofs made of brick or cement, which increased to 11.9 per cent in 2022. Similarly, homes with wall materials other than mud or bamboo rose from 20 per cent in 2016 to 35 per cent in 2022.

Food consumption: Per-capita daily food intake increased from 974 grams in 2016 to 1,125 grams in 2022.

Digital and energy access: Internet penetration: As of the July-September 2024 quarter, 46 per cent of rural households had internet access. The proportion of households with smartphones was 66.7 per cent in rural areas and 77.8 per cent in urban areas, according to the ICT Access and Use Survey 2024-25 conducted by the Bangladesh Bureau of Statistics (BBS).

Mobile-phone penetration: Mobile-phone penetration in rural areas reached 98.6 per cent, nearly on par with urban areas at 98.9 per cent.

Electricity access: Rural households with electricity access stood at 97.8 percent, compared to 99.2 percent in urban areas.

Agent banking has given a fillip to rural economy. The rising living standards and modern facilities in rural areas cannot be attributed solely to agent banking, but its contributions are undeniable. By reducing transaction costs and ensuring timely access to funds, this innovation in banking has supported economic activities, non-economic expenditure and overall household welfare. This, in turn, has rejuvenated the rural economy and is expected to drive further growth in years ahead.

jasimharoon@yahoo.com

© 2026 - All Rights with The Financial Express