Optimistically enough we are celebrating the 2nd National Insurance Day today. In order to reaffirm the purposes of insurance in our social and economic lifecycle, the government introduced such an energizing event, the first of its kind, back in 2020.

Optimistically enough we are celebrating the 2nd National Insurance Day today. In order to reaffirm the purposes of insurance in our social and economic lifecycle, the government introduced such an energizing event, the first of its kind, back in 2020.

To our credence and experience, the underlying premeditation of the observance of the day has literally been efficacious for the revival of our insurance sector despite the shock of Covid-19 pandemic, which claimed more than 205 million lives until February 27 last.

Throughout the pandemic period, insurance being one of the constituents of our financial market has recorded a negative growth, primarily resulting from slowdown of national economic activities and ongoing lockdown in different parts of the world. Nonetheless, Bangladesh scored well among the SAARC countries in the international Covid Resiliency Ranking.

The nation has great expectations from the insurance sector as a whole so that she can boldly face the challenges in our way to materialise the Bangladesh Vision 2041 - a brainchild of Her Excellency Prime Minister Sheikh Hasina for the socio-economic advancement of the country in the decades to come.

For such end in mind, those who are directly involved in insurance business have a lot to play, particularly the policy makers, regulatory body, board of directors and chief executive officers of the 79 market players.

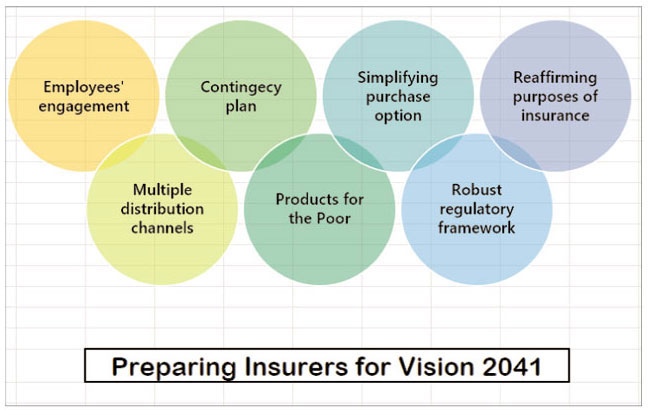

Let's delve deep into some dos and don'ts for finally figuring out something nourishing for all stakeholders of the Bangladesh insurance market.

Let's delve deep into some dos and don'ts for finally figuring out something nourishing for all stakeholders of the Bangladesh insurance market.

Reaffirming the purpose of insurance to the mass people: In our country the lack of insurance awareness is one of the hurdles in improving penetration rate. It is awareness that can act as a tool for stimulating people of all walks of life to purchase insurance products, thereby ensuing their participation in the nation building activities through investment and saving with the help of life insurance mechanism.

Non-life segment can play a vital role for the developmental economic activities. According to the US Centre for Excellence in Disaster Management and Humanitarian Assistance, Bangladesh has been affected by more than 200 natural disasters over the last three decades. The country's geographical location next to the Bay of Bengal, low-lying terrain, monsoons, and significant rivers make the country very vulnerable to natural disasters.

From 1970-2019, cyclonic storms have been the most frequent disaster to affect Bangladesh at 52%, followed by floods at 31%, with the remaining disasters being epidemics, earthquakes, droughts, and landslides.Under the above context, the IDRA and insurers should put their heads together, using mass media and social media such as Facebook, YouTube, etc., for educating the common people about the social & economic importance of insurance in the case of natural disasters.

Bringing uninsured community under insurance umbrella: According to Bangladesh Economic Handbook, one in every four persons has life insurance. Bangladesh stood the 55th in the world in terms of premiums as a percentage of GDP (Ref: Swiss Re Sigma 3/2019). The insurance regulator IDRA sources recently said that insurance density is USD 10.3 per person in 2019 which is an increase by USD 2.0 per person from the previous year while the insurance penetration remains almost the same i.e., 0.56 per cent (overall) of the GDP in 2019.

So, it is evident that the penetration rate is far away from keeping pace with the GDP growth rate in the country. This expressly indicates the affordability of the potential customers. For capturing the vast uncovered community, our product designs and promotions needs to be done as per the changing need of the potential buyers, who have long been untapped.

Simple products and simple purchase options: There should be an on-going process to introduce new products to have growth potentials by penetrating the new segment of the market with superior services. A cardinal principle of insurance is to diversify and achieve spread so that insurer is not reliant on limited classes of business. Developing new products means a combination of, or variation to, existing insurance products that results in a material change to the risk profile/nature of the existing products.

Advantage of new products includes:

• Diversifying product lines

• Catering to needs of the customers

• Boosting gross premium income

• Keeping pace with recent trends in insurance

Some trendy new products in Bangladesh may be personal ones (Flat, Household Contents, etc.), personal accident, Takaful, agriculture, cyber liability, and RMG-based insurance products.

Products for poor community: While 2nd largest portfolio in India is agriculture insurance, in Bangladesh this class is still under pilot project of Sadharan Bima Corporation. Local farmers can be protected by offering weather index-based crop insurance, livestock insurance and health insurance. Underwriting these classes essentially requires expertise of the underwriters.

In such social products, government may subsidise to the certain extent. The Covid-19 pandemic has made it clear to the concerned that there is an immediate requirement of the health-related insurance products in our country. Not a significant portion of our population are under the health coverage whereas almost 20% Indian has some sort of health insurance cover, of course, at a very optimum cost.

Broadening coverage of the existing products & distribution channels: Our insurers have been offering the traditional types of insurance products through the old-fashioned distribution channels like direct and agency methods. Contrary to the above, most of the South Asian markets have already introduced diverse channels like Bancassurance, Brokers and web Aggregators. Other than MNC clients, very few commercial insurance policies in Bangladesh covers business interruption in addition to material damage, let alone extended coverage of employer's liability, for example. The industrial all risks policy is locally popular, but it covers with a number of exceptions. Due to lack of skilled underwriters, coverages remain limited.

Nurturing culture of engagement among employees: There is no denying the fact that an employer can get the best performance only from the engaged employees. Employee engagement is the extent to which people are personally involved in the success of a business. Basically, engagement is closely linked to an employee's emotional connection to his or her company, and how that connection influences the to job performance. Insurers should actively take into consideration of the employee engagement issues for attainment of the desired level of customer services. Human resources policy of the insurance company must encompass the different measures in order for keeping their employees motivated and engaged. Above all; employee engagement is the constituent part of "The Service-Profit Chain" of an enterprise and also the working capital of any service-oriented company.

Simplifying the work process for the insurance employees: 81% of insurance employees consider that their work environment and business practices are either "complex" or "very complex". Company should take initiatives to streamline processes by investing in re-engineering of business process.

This will definitely help companies easily comply with the regulatory changes, and it can reduce the time employees are spending regularly on navigating complex and antiquated system, which would contribute to maintain the life balance among the employees.

Survey indicates that work life balance is a top career goal for insurance employees and for graduates who are the future job seeker and this trend has been continuing since 2008.

Another survey indicated that 20% of the organisation currently have attached priority to the simplification programme. When work simplification process will be handy, it will save time spent on gathering information by the actuaries, who will then be able to dedicate their time on analytical works for bringing better bottom line for the organisation.

Business friendly regulatory framework: The robust regulatory framework is the preconditions for thriving of a financial industry. The recent regulatory move to bring discipline in the market is evident and two new acts have already been enacted. Following the enactment of 'Insurance Act 2010', the regulator IDRA has been working for formulation of the various customer friendly rules and regulations. In the past couple of months, the IDRA has issued a few corrective circulars for the benefit of not only the policyholders but also the insurers. To our perview, such measures will positively lead the insurers to self-regulation in day-to-day operation of their companies, of course, fully consistent with the requirements of prudential regulation of IDRA.

Business contingency plan to be in place: As Dr. Jerome Haegeli, group chief economist of Swiss Re, put it rightly: "COVID-19 is causing the worst recession of our lifetime. Yet in the face of adversity, insurance markets are holding up well as premiums see a V-shaped recovery, which is the recovery movement involving a sharp rise back to a previous peak after a sharp decline in these metrics.

For recovering at the faster speed, all concerned need to adopt a collaborative approach in which the government must be the forerunner. This is necessary to facilitate a faster recovery of the economy. The individual companies must embed the business continuity plan in their corporate strategy and also put in the culture. This plan also needs to be updated in line with the changing circumstances, by continuously managing three key phases of the crisis-respond, recover, and thrive.

To sum up, it is known to the market practitioners that there exists a pressure from pre-existing obstacles, recent slowdown of economic activities due to Covid-19, and above all, the hardening of International reinsurance market.

I myself being a core support of optimism cherish the opinion that if we all put our heads together to do our level best for the advancement of the sector, we will indelibly be capable of meeting the nation's expectations, to a greater extent, which would in the long run be contributing to reshape our countryin the light of Bangladesh Vision 2041.

Md. Khaled Mamun FCII (UK) is the Chief Executive Officer of Reliance Insurance Limited, and an associate of Bangladesh Insurance Academy, and also a fellow member of the Chartered Insurance Institute of the United Kingdom.

© 2026 - All Rights with The Financial Express