Claim settlement is like a mirror to insurance companies where the people see the real face of the industry. When an insurance company fails to settle claims, the policyholders feel frustrated and this discourages them to buy new policies.

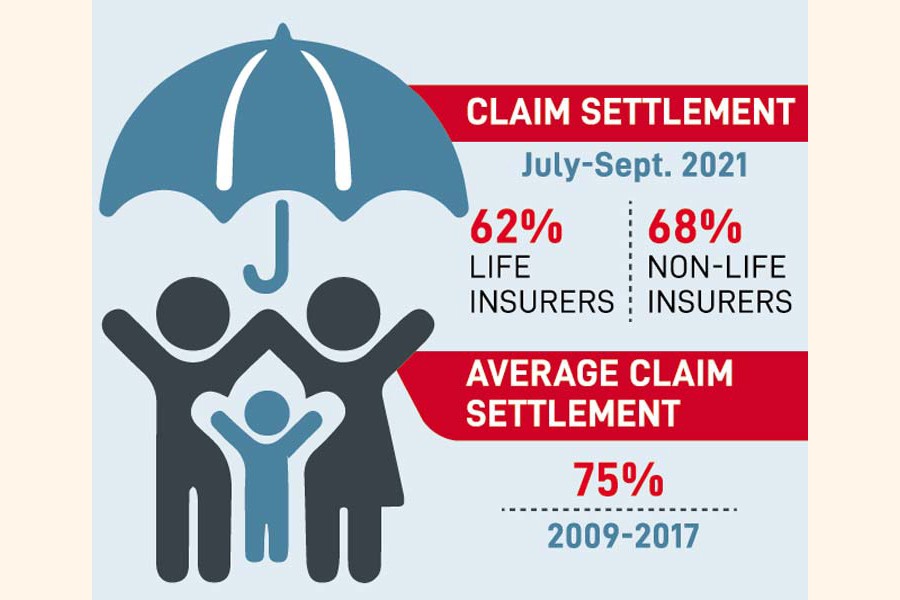

According to a claim settlement report of the Insurance Development and Regulatory Authority (IDRA), the claim settlement rate during the period of July- September 2021 was 62 per cent for life insurers and 68 per cent for non-life insurers. The average claim settlement rate was 75 per cent during 2009-2017. So, the claim settlement rate of the insurance sector is not satisfactory.

Claim settlement is one of the most important services that an insurance company can provide to its customers. Insurance companies have an obligation to settle claims promptly. There is a saying: 'Insurance companies solely depend on the customers but the customers do not depend on them'.

Therefore, maximum customer satisfaction needs to be ensured and claim settlement needs to be done as soon as possible.

Claim settlement is the key element of customer satisfaction which has long been ignored by insurers. According to the insurance act, the claim has to be paid within a maximum of 90 days. In many cases, the claim is not paid within 90 days. So, the reasons for this need to be analyzed and resolved.

The insurance companies have cited some reasons for which the settlement of a claim takes more than 90 days. The reasons are: submission of incomplete information by the insured, wrong nominee information in the insurance claim form, delay in receiving reports from concerned parties, wrong or partial information given by the insured and influence and non-cooperation by the insured during investigation.

Recommendations:

According to the information provided by different life insurance companies and analysis of the information, the following recommendations can be made for quick claim settlement:

1. The information and documents that can be taken at the time of the insurance contract, need to be taken for faster claim settlement. Besides, information that needs to be collected afterward i.e. after the claim is intimated needs to be collected as soon as possible or possibly online.

2. Claim settlement time could be lessened from 90 days & IDRA could take steps in this connection. Besides, for quick claim settlement, companies could form a separate special committee.

3. If any company loses its life fund growth, then it's difficult to settle the claim. Because of unplanned investment, the company loses income and a life fund cannot be created. As a result, companies cannot settle claims. Another reason for the fund crisis is false papers showing increased high values of assets whose resell values are less. Some financial institutions (leasing companies and banks) recently were unable to give the capital back wherein Insurance companies had funds that they could not get back. This is also creating a fund crisis. Therefore, insurance companies need to make investments carefully.

4. Lack of skilled professionals in life insurance companies i.e. lack of skilled managers in the actuarial department who have knowledge about technical matters like an investment of insurance products, surrender value, terms and facilities of life insurance products and investment facilities, and future value of maturity claims. Good knowledge about management costs and business profitability is also required. So, the recruitment of skilled manpower in insurance companies is needed.

5. Creation of awareness of the insured in submission of necessary documents and other matters to the insurers.

6. Making policyholders aware of their responsibilities and the duties by the insurance companies.

7. Proper collection and documentation of nominee information should be ensured by the insurance companies.

8. Digitization of the claim settlement process which can make the claim settlement speedy.

9. Concerned departments of insurance companies (claim department) should be sincere in submitting reports from various parties on time.

10. Developing door-to-door insurance services for claim settlement.

11. Taking steps to improve the ethics of all concerned.

12. Formation of an efficient claim management committee.

13. Prevention of fraud by the insured.

14. Implementation and development of a customer care service system.

The existing claim settlement system of the life insurance sector could be improved and quick claim settlement could be ensured by implementing the recommendations made above. Claim settlement should be given the highest priority in order to create a positive image of the insurance industry and ensure full customer satisfaction. The sooner the claims are settled, the better the image of the insurance industry will be.

The writer is Director (additional charge), Bangladesh Insurance Academy.

smibrahimacii@gmail.com

© 2026 - All Rights with The Financial Express