Babul Barman

Shareholders of eight listed non-bank financial institutions (NBFIs) stand to lose around Tk 1.36 billion in current market value as the Bangladesh Bank prepares to declare them non-viable.

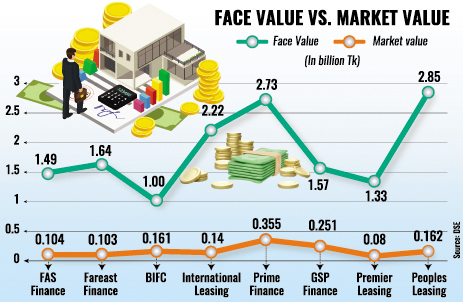

However, the actual loss is far greater. Together, the eight NBFIs have a combined paid-up capital of Tk 14.84 billion, representing the face value of shares at Tk 10 each.

The shares have long been trading far below their face value. Many investors may have bought the shares at prices even higher than the face value in the secondary market.

For instance, the stock of Bangladesh Industrial Finance Company (BIFC) traded above Tk 12 per share two years ago but fell to just Tk 1.50 by Tuesday. Similarly, FAS Finance's share closed at Tk 0.63 on Tuesday, down from Tk 6.20 two years ago.

Bangladesh Bank's decision to wind up nine NBFIs-eight of which are listed-marks the first large-scale liquidation in the country's financial sector. The move aims to protect depositors and restore financial stability.

The eight listed companies are FAS Finance, Bangladesh Industrial Finance Company, Premier Leasing, Fareast Finance, GSP Finance, Prime Finance, People's Leasing, and International Leasing.

Except for Prime Finance, all recorded negative net asset values (NAV), ranging from Tk 0.62 to Tk 219.03 per share. This indicates that their liabilities far exceeded assets, reflecting severe financial distress and poor asset quality.

Shareholders of the NBFIs slated for liquidation may ultimately lose everything.

Based on assessments of the institutions' assets, a decision will be taken on whether shareholders will receive anything, Bangladesh Bank Governor Ahsan H Mansur said at a press briefing on Monday.

The central bank is set to wind up nine NBFIs this week, as they have long struggled to repay depositors due to unsustainable financial conditions stemming from massive irregularities and loan fraud during the previous government.

These NBFIs account for 52 per cent of total defaulted loans in the sector, estimated at around Tk 251 billion at the end of 2024.

Among the troubled institutions, FAS Finance has the highest non-performing loans (NPLs) at 99.93 per cent, while GSP Finance has the lowest at 59 per cent.

"Given the current financial condition, general investors have little to hope for, as they would be at the bottom of the repayment hierarchy," said Akramul Alam, head of research at Royal Capital.

In other words, once assets are sold and liabilities settled, little-or nothing-may remain for ordinary shareholders.

Under liquidation rules, external creditors are

paid first, followed by depositors, debenture holders, and preferential shareholders.

"In such insolvency-driven liquidation, shareholders sit at the very bottom of the list of claimants," Alam said.

How much will be repaid to depositors

The central bank governor said individual depositors would recover their principal amounts before Ramadan in February this year. The government has verbally approved around Tk 50 billion for depositor repayments.

However, total deposits at the affected NBFIs stood at Tk 153.70 billion. Of this amount, Tk 35.25 billion belonged to individual depositors, while Tk 118.45 billion was held by banks and corporate clients, according to central bank data.

Who is responsible for the collapse

The collapse of the institutions reflects a collective failure of auditors, regulators-including Bangladesh Bank and the Bangladesh Securities and Exchange Commission (BSEC)-and company management.

Investors were misled by financial statements that concealed the true extent of defaulted loans.

"The financial distress is not sudden. The institutions have long been plagued by poor governance and unchecked irregularities," said Salim Afzal Shawon, head of research at BRAC EPL Stock Brokerage.

Auditors and credit rating agencies must be held accountable, and regulators cannot evade responsibility either, Shawon added.

Industry insiders also blame the central bank for approving flawed financial statements and, in many cases, determining the level of loan-loss provisions companies were required to maintain.

Bangladesh Bank spokesperson Arief Hossain Khan recently said the central bank was unable to ensure good governance due to political influence and regulatory limitations during the previous regime.

"Besides, many clients of the companies obtained court orders preventing them from being classified as defaulters," Khan said.

The institutions will be liquidated under the Bank Resolution Ordinance 2025, the country's first comprehensive framework for resolving failing banks and non-bank financial institutions.

babulfexpress@gmail.com

© 2026 - All Rights with The Financial Express