The issue of central bank independence has two elements. First— governance, how is the central bank governed? Are its leadership appointments merit-based? Are its internal decisions insulated from day-to-day political interference? The prevailing wisdom around the world is that management systems for central banks must remain fairly independent from general government administration. The appointment of the governor, deputy governors, and senior economists must follow a clear, preferably legal or statutory, framework. The internal management of the bank and its regulation of commercial banks must be transparent and robust, and free from outside interference.

Second— functional independence, what does the central bank do? Does it have the autonomy to set monetary policy, control inflation, manage exchange rates and supervise the banking system without needing to seek political approval at every turn? The answers in Bangladesh are worrying. The central bank is expected not only to control inflation, but to support growth-friendly policies, stabilize the exchange rate, and support business-friendliness all under the influence of fiscal and, occasionally, political constraints.

The governance fault-line in our system is acute. On one side, we have state-owned commercial banks (SOBs) regulated by the Financial Institutions Division (FID) of the Ministry of Finance; on the other, private banks are regulated by the Bangladesh Bank. This division of regulatory responsibility is irrational. The two sets of banks operate in the same economy, share inter-linkages and systemic risk. Yet they answer to different authorities. This dichotomy invites regulatory arbitrage, weak accountability and political patronage. The result: state-owned banks carrying NPLs of more than 45 per cent, and the banking sector as a whole flirting with a 36 per cent NPL ratio. Clearly, this does not make much economic sense.

Therefore, having miserably failed its regulatory mission, the FID’s role in bank regulation must be eliminated by closing down this redundant Division of the Ministry of Finance, and the Bangladesh Bank must regulate all commercial banks, state?owned as well as private. Only then can the “one banking system” principle be enforced, with uniform supervision, consistent rules and real accountability (sans political interference). Without that structural reform, no amount of tinkering will restore public trust or financial stability in the banking system.

Turning to policy responsibility: in principle, the central bank must manage inflation, money supply, exchange rate and, in our context, support growth. But therein lies the rub. In a mature economy, one might suppress inflation via aggressive monetary tightening (the kind of action taken by Paul Volcker in the United States (early 1980s) where interest rates were whipped up to above 20 percent). That is not an option for Bangladesh. Our economic context is very different. We are a developing country, confronting both demand and supply constraints. Inflation here is not, as Nobel Laureate Milton Friedman argued, “always and everywhere a monetary phenomenon”. It is also rooted in supply-side shocks, arising from external price shocks, tariffs, energy price spikes and exchange-rate depreciation (as echoed by another Nobel Laureate economist, James Tobin).

Look at recent experience: the Bangladesh Bank intervened in the foreign exchange market to defend the taka at roughly 85-86 per US dollar until mid-2022. In the process about US$10 billion of reserves were depleted in about a year. Eventually, when BB let go, the taka still depreciated by some 30 per cent (about 40 per cent as of June 2025) and inflation picked up hard and fast. A recent World Bank study revealed that some 70 per cent of this inflation could be attributed to the energy price hike and exchange rate depreciation. That sequence shows that monetary policy alone cannot succeed when the underlying structural issues are ignored. Exchange rate shocks, imported inflation, tariff distortions all feed into price movements. Moreover, monetary transmission mechanism in Bangladesh has been found to be weak in view of the large informal sector and other market failures. Therefore, the efficacy of interest rate policy in curbing inflation in Bangladesh may have its limitations. What this tells us is that the central bank must possess the capacity to rigorously analyse and diagnose inflationary episodes to be able to thwart inflation in an effective manner. It must also have absolute authority and independence to fight inflation with all instruments at its disposal.

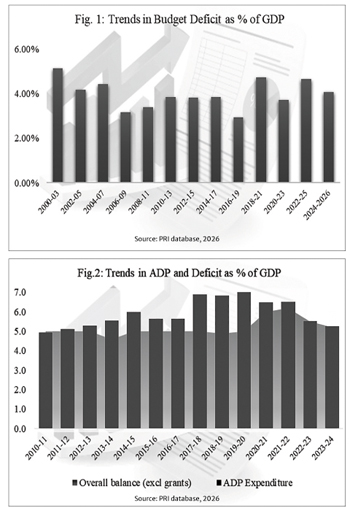

But there is a development dimension in the Bangladesh context that needs to be recognized. To propel growth, create jobs and reduce poverty, Bangladesh must invest heavily in development: building infrastructure, investing in health, education, and overall productivity enhancement. Yet, it cannot do all this with its own revenue resources. So, it must run budget deficits, financed by borrowing. The budget deficit has averaged about 4.5 per cent of GDP over the last two decades (Fig.1).

The more pertinent question concerns deficit financing, which reveals the underlying macroeconomic strain. Bangladesh finances approximately 60 per cent of its fiscal shortfall domestically. External sources provide the remaining 40 per cent or roughly 2 per cent of GDP, through multilateral and bilateral loans, while commercial banks, the central bank, and public borrowing contribute around 3 per cent. Each financing mechanism has distinct implications for inflation, private investment, and monetary management. Borrowing from the public through savings certificates and government bonds provides a predictable and politically palatable source of funds. Yet, it comes at a steep price. Interest rates on these instruments are often fixed above market levels, creating distortions across the financial system. When savings certificates yield more than bank deposits, households logically shift their savings toward the former, draining liquidity from the banking sector. The result is financial disintermediation. Banks face higher deposit costs, lending rates rise, and access to affordable credit for businesses tighten.

Borrowing from the banking system introduces another layer of complexity. When the government absorbs a significant share of available loanable funds, the private sector is effectively crowded out. Investment in private enterprise declines, undermining the very growth objectives that deficit spending seeks to achieve.

The most perilous option, however, is direct borrowing from the Bangladesh Bank, which is known as the lender of last resort, effectively monetising the deficit. This approach injects liquidity into the system fueling inflation and eroding purchasing power. It is, in essence, a short-term fiscal fix that carries long-term macroeconomic costs. The central bank is then forced into an impossible position: attempting to control inflation with monetary restraint while simultaneously accommodating the government’s financing pressures.

It is the push for development via an annual development programme (ADP) that results in the budget deficit (Fig.2) that then brings the financing pressures. Note that ADP size is typically slightly higher than the budget deficit. The fiscal space – a small surplus over current expenditures – has been narrowing as public operational expenditures swell and revenue mobilization falters. Consequently, much of the ADP financing must be done via budget deficits comprising domestic and foreign borrowing. As explained earlier, where domestic borrowing of the Government has to be from the central bank, in the Bangladesh context, there is little that the latter could do to avoid it. [Imagine Governor, BB, telling the Finance Minister…”sorry, we can’t lend you money to finance your deficit”]. There is a high-powered Coordination Council for fiscal-monetary coordination that ostensibly does the fiscal-monetary balancing act which essentially goes down to agreeing on how much of the deficit BB could finance.

Thus far it is the Finance Ministry that has always prevailed. To think otherwise is not to acknowledge the Bangladesh reality today, and as far as we can reckon in the future. To that extent, independence of BB is a justified pursuit in so far as its own governance and banking sector monitoring responsibilities are concerned. However, monetary policy independence will continue to be overly inhibited by the presumptive needs of deficit financing driven by fiscal deficits for investment in our development programme.

Dr Zaidi Sattar is Chairman and Hasan Al Banna is Senior Research Associate (SRA) at Policy Research Institute of Bangladesh (PRI). zaidisattar@gmail.com; h.albanna71@gmail.com

© 2026 - All Rights with The Financial Express